Can Skin Booster Injections Enhance Skin Texture?

Health |

2026-06-02 07:44:28

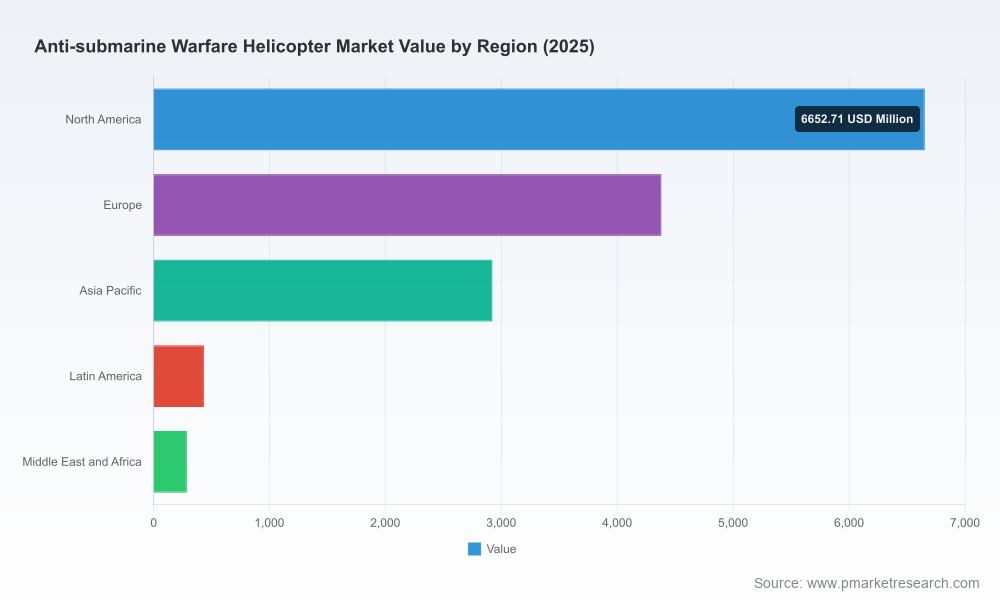

Report base year: 2025; forecast period: 2026–2032. Our model shows a steady market expansion from a 2025 baseline to a materially larger market by 2032, reflecting a compound annual growth rate (CAGR) of 4.12% over the forecast window.

Anti Submarine Warfare Helicopter Market

Why this matters now: accelerating naval modernization programs, renewed alliance spending commitments, and an active export cycle for premier ASW platforms are collectively reshaping procurement horizons and supplier strategies in 2026.

Anti Submarine Warfare Helicopter Market

Market concentration: the sector is moderately concentrated — the top-three firms account for a majority share and the top-five firms capture well over half of industry revenues — creating both barriers and predictable supplier pathways for fleet planners and OEMs.

Anti Submarine Warfare Helicopter Market

Report focus: actionable guidance for procurement officers, program managers, OEM strategy teams, and investors seeking to translate macro momentum into resilient 2026 decisions without exposing confidential program-level detail.

Translate macro momentum into procurement timing. The market trajectory and sector dynamics in our forecast help organizations choose whether to accelerate replacement cycles, extend sustainment, or pursue interim capability buys.

Align capability investments with alliance interoperability. Contemporary ASW requirements increasingly prioritize sensors, data fusion, and allied operating standards — our analysis maps those operational expectations onto practical procurement trade-offs.

Balance manned platforms and unmanned augmentation. The naval aviation mix is evolving; decision-makers need robust ROI and risk frameworks to decide when to procure additional manned helicopters versus investing in unmanned or mission-kit solutions.

Mitigate supply chain and sustainment risk. The report exposes critical supply-chain chokepoints, spare-part lead-times, and obsolescence windows to support realistic availability forecasts and contingency sourcing in 2026.

Concise market sizing and trend synthesis anchored to 2025 baseline metrics and our 2026–2032 forecast, with scenario sensitivity to procurement pacing and geopolitical shocks.

Operational playbooks: procurement timing matrices, fleet transition roadmaps, and integration checklists that convert strategic intent into executable program milestones.

Supplier resilience tools: scorecards and stress-test templates to quantify vendor delivery risk, sustainment cost drivers, and domestic-manufacturing exposure.

Investment decision aids: capital-allocation models and comparative TCO templates for manned vs. unmanned options, upgrade vs. replacement decisions, and export-opportunity assessment tools.

Scenario planning modules: three defensible pathways (base, accelerated modernization, and constrained-budget) that illuminate trade-offs in capability, cost, and timeline to 2032.

Lockheed Martin (Sikorsky) remains a global reference platform provider with a mature ASW helicopter portfolio and recent delivery milestones that reinforce fleet sustainment narratives. Such delivery rhythms materially influence allied interoperability planning and aftermarket service expectations.

NHIndustries (the Airbus/Leonardo/Fokker JV) continues to position its NH90 Sea Tiger/variant family as the backbone of several European and partner navies’ ASW roadmaps; recent handovers underscore the program’s role in regional modernization cycles.

Leonardo leverages the AW family in export and nation-level programs, complementing JV activities and providing alternative industrial partnerships in multi-vendor procurement strategies.

Harbin Aircraft Industry Group (AVIC) is scaling indigenous shipborne platforms in response to local naval programs, highlighting a parallel market trajectory driven by domestic replenishment and blue-water ambitions.

Kamov (Russian Helicopters) sustains a presence in legacy fleets and select export markets through modernization programs and platform refresh cycles.

Airbus Helicopters is actively integrating unmanned systems into maritime architectures, signalling a future operating model that blends manned helicopters with UAS mission kits for expanded, distributed ASW coverage.

Implication: a mix of entrenched OEM incumbency and targeted innovation creates both predictable supply channels and windows for niche suppliers to capture capability adjacencies (sensors, mission systems, sustainment).

Fleet sustainment vs. capability uplift: aging helicopter fleets push navies into a dual-track decision — sustain existing airframes longer or accelerate procurement of next-generation maritime platforms. Each path has distinct cost and readiness outcomes that we quantify in the report.

Sensor and weapons integration as force multipliers: investments in dipping sonars, sonobuoy networks, torpedo integration, and onboard processing are increasingly decisive for operational effectiveness. Our analysis ranks integration levers by cost-effectiveness and lead time.

Alliance-driven procurement: NATO and allied signaling around defence spending and interoperability are reshaping procurement timetables — collaborations, joint buys, and shared sustainment contracts are becoming preferred risk-mitigation strategies.

Unmanned systems and modular mission kits: VSR-class and missionized UAS present a credible augmentation path, affecting fleet sizing and sortie-generation calculations in our scenarios.

Supply-chain sovereignty and industrial policy: nations are weighing onshore production and licensed manufacture against total-cost and schedule efficiencies; our supplier playbook helps quantify the trade-offs.

Procurement Timing Matrix — a decision-support grid that aligns capability requirements, budget cycles, and industrial lead times to recommend optimal procurement start dates and contract structures.

Supplier Resilience Scorecard — a repeatable diagnostic measuring production capacity, single-source exposure, repair-cycle readiness, and geopolitical risk.

TCO and ROI Models — customizable templates that capture acquisition, sustainment, and upgrade lifecycles for manned helicopters versus unmanned alternatives, enabling apples-to-apples capital planning.

Capability Gap Heatmaps — operationally focused visualizations that highlight theatre-level ASW shortfalls and recommended mitigations across near-, mid-, and long-term horizons.

Run a short-form TCO using our template to stress-test fleet sustainment budgets and identify immediate cost-avoidance opportunities.

Map supplier single points of failure for mission-critical subsystems and begin contractual dialogue on redundancy or license-right contingencies.

Commission a focused interoperability trial (sensors, datalinks) with a prioritized partner to validate cross-platform ASW workflows and reduce integration risk ahead of full procurement.

Use our scenario modules to rehearse budget-constrained options and identify which capabilities to defer without fatally degrading operational reach.

The Anti-Submarine Warfare helicopter market entering 2026 is a market of disciplined growth and strategic inflection. Navies and suppliers face a clear set of trade-offs: accelerate replacement to embed new sensors and fuel interoperability, or extend sustainment and invest in modular unmanned augmentation. Both paths are defensible; the right choice is program-specific and time-sensitive. Our report converts the market’s macro trajectory and the competitive moves of leading OEMs into a practical playbook for 2026 decisions — from procurement timing to supplier hedging to capability prioritization.

For senior leaders making near-term budget and program choices, the full PW Consulting market study delivers the confidential segmentation tables, country-level forecasts, vendor scorecards, and downloadable decision tools necessary to execute with confidence. Visit the PW Consulting report page to access the complete dataset and schedule a briefing with our senior analysts.

For detailed analysis of this topic, please visit the official page:Anti Submarine Warfare Helicopter Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com