The Real Reason Students Turn to Essay Writing Services in 2026

Other |

2026-07-01 05:40:45

PW Consulting today publishes an executive-level strategic briefing that previews our full Oxindole Market report (base year 2025, forecast 2026–2032). Designed as a decision-ready roadmap for corporate leaders, procurement heads, and investors planning activity in 2026, this briefing synthesizes the market’s macro trajectory, competitive dynamics, and actionable responses firms should prioritize to preserve margin, secure supply, and capture product-extension opportunities.

Oxindole Market

Market scale and growth: Oxindole has expanded from an estimated USD 67.8 million in 2020 to USD 85.5 million in 2025, reflecting recovery and demand reallocation across pharmaceutical intermediates and fine-chemicals uses. Our forecast projects the market to grow to approximately USD 118.7 million by 2032 at a compound annual growth rate (CAGR) of 4.81% over 2026–2032.

Oxindole Market

Competitive posture: Market concentration is moderate — the top three suppliers account for roughly 42% of market volumes, and the top five about 58% — indicating meaningful scale advantages for incumbent manufacturers while still leaving room for specialist suppliers and regional players to win niche demand.

Oxindole Market

Supply-demand balance: The near-term outlook (2026) points to steady, manageable growth rather than a structural supply crunch. However, cyclical raw-material pressures, regulatory tightening for pharmaceutical intermediates, and logistics bottlenecks can create episodic price and availability volatility that require proactive mitigation.

Protect margin under modest-but-steady growth. With a mid-single-digit CAGR, companies will not be able to rely on volume growth alone to protect profitability. Tactical moves — supplier consolidation for cost-to-serve savings, differential pricing for higher-purity grades, and value-added services for pharma customers — will be central to improving operating leverage.

De-risk procurement. The current structure — a mix of global catalog suppliers, regional manufacturers, and custom producers — creates both choice and complexity. Firms with limited supplier intelligence risk supply interruptions or paying a premium for last-minute purchases.

Position for product adjacencies. Demand from pharmaceutical intermediates remains the single largest end-use driver. Forward-looking chemical firms should evaluate formulation adjacencies and custom synthesis offerings that increase share of wallet with drug-discovery and API customers.

End-market mix resilience: Pharmaceutical synthesis continues as the principal demand engine. Markets such as dyes, research chemicals and agrochemical synthesis provide complementary demand that smooths cyclicality but differ in commercial expectations (lead times, purity requirements, regulatory documentation).

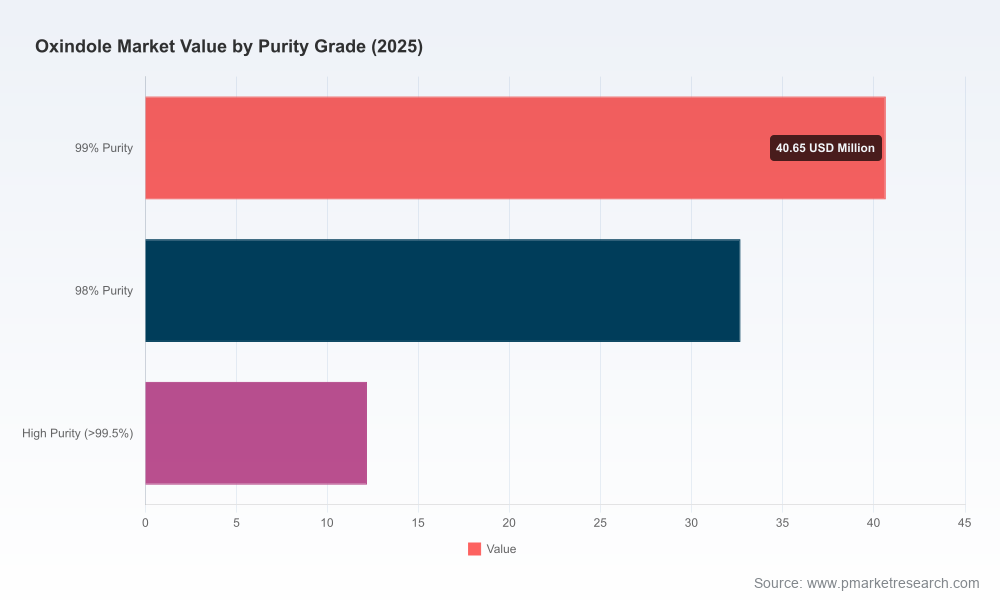

Purity segmentation compresses margins but expands service opportunities. Customers requiring high-purity (>99.5%) material are willing to pay for certified processes, analytical traceability and tighter supply windows, opening up premium pricing segments for suppliers who can demonstrate robust quality systems.

Geographic sourcing & logistics: Supply chains remain regionally structured with Asia-based production often serving as the low-cost backbone. However, regulatory and customer nearshoring trends are prompting select regional capacity investments and qualification cycles in 2026.

Regulatory and compliance drift: Pharmaceutical supply-chain scrutiny continues to rise. Producers capable of GMP-compliant manufacturing and audit-readiness are increasingly preferred partners for higher-margin pharmaceutical applications.

Our full Oxindole Market report is designed as a playbook for executive teams. Key deliverables include:

A transparent market model with historical series (2020–2025) and granular forecasts by purity-grade, application, and region for 2026–2032 — enabling bottom-up scenario planning.

Supply-chain risk matrices mapping feedstock exposure, single-source nodes, logistics sensitivity and regulatory risk — prioritized by probability and business impact.

Supplier profiling and scorecards that evaluate capacity footprint, quality systems, price positioning, and strategic fit for targeted customer segments.

Commercial playbooks for procurement and sales — including recommended contract structures, hedging approaches for spot purchases, specification negotiation levers, and value-based pricing tactics for premium grades.

Scenario analyses and sensitivity testing for raw-material price shocks, regional capacity additions, and demand shocks from the pharmaceutical and agrochemical sectors.

M&A and investment checklist: diligence templates, integration risk mapping, and target-screening criteria for bolt-on producers and specialty intermediates suppliers.

Note: This briefing intentionally previews the analytical framework and strategic recommendations. Detailed segment-level tables and supplier-by-region metrics are available exclusively in the full report.

MilliporeSigma (Sigma-Aldrich) — A global catalog leader with deep distribution networks and recognized quality credentials. Their strength lies in serving research and development workflows and small-scale pharma synthesis across developed markets. Strategic implication: incumbent advantage in early-stage drug discovery; less exposure to large-volume industrial synthesis unless complemented by manufacturing partnerships.

TCI Chemicals (Tokyo Chemical Industry) — A Japan-headquartered specialist supplying high-purity grades for laboratory and material-science customers. TCI’s reputation for tight specifications and consistent analytical data makes it a preferred vendor for discovery chemistry and advanced-materials labs. Strategic implication: premium positioning, opportunity to expand into custom synthesis and Asian pharma suppliers.

Thermo Fisher Scientific (Alfa Aesar) — A broad-based supplier combining catalog convenience with global service. Alfa Aesar’s reach and brand give it access to institutional customers in academia and industry. Strategic implication: strong at R&D scales and cross-selling adjacent products; may face margin pressure on commodity-grade Oxindole.

Combi-Blocks — Focuses on gram-to-kilogram scale supply for medicinal chemistry and custom-route work. Strengths include flexibility and willingness to do small-batch custom work. Strategic implication: attractive partner for biotech firms and CROs seeking tailored quantities and rapid-turnaround synthesis.

Apollo Scientific — UK-based distributor of high-purity heterocycles, well positioned for European research markets. Strategic implication: maintains relevance through fast logistics and targeted technical support to discovery teams.

Oakwood Chemical — A U.S. manufacturer with capacity to supply both industrial and academic users. Strategic implication: competitive in regional supply and custom production; potential acquisition target for firms seeking Western manufacturing footprint.

Hairui Fine Chemicals & Capot Chemical — China-based producers with GMP capabilities and bulk-manufacturing orientation. Strategic implication: cost-competitive providers of intermediates for the pharma and agrochemical value chains; attractive for buyers seeking volume discounts but requiring careful qualification for regulated end-uses.

Supplier segmentation and dual-sourcing: Classify supply partners by purity-grade capability, regulatory readiness and lead-time performance; dual-source critical grades to avoid single-point failure.

Value capture via productization: Invest in certification and analytics to monetize high-purity grades and traceable supply for pharma customers; consider co-development arrangements with API manufacturers for long-term offtake.

Selective vertical integration: For firms heavily exposed to raw-material price swings, targeted upstream moves (tolling or captive synthesis) can stabilize costs — evaluate against capital intensity and margin lift thresholds.

Commercial differentiation: Use logistical reliability, documentation (e.g., GMP, COA granularity), and technical support as competitive differentiators versus competing on price alone.

M&A and partnership scouting: Seek bolt-on assets with complementary purity capabilities or regional footprints to lift share in strategic end-markets.

Procurement leaders: Use the supplier scorecards and risk matrices to restructure contracts and implement a three-tier sourcing strategy (strategic, preferred, tactical).

Business development and sales teams: Leverage end-use demand maps and purity-segmentation playbooks to prioritize accounts and tailor technical dossiers.

Corporate development: Apply the M&A checklist and valuation sensitivity outputs to screen acquisition targets and model integration upside.

R&D and technical operations: Adopt the manufacturing-route benchmarking and specification harmonization guidance to reduce qualification cycles when onboarding new suppliers.

Oxindole’s market is entering 2026 with steady growth, moderate concentration and a clear hierarchy of commercial demands. Success in this environment will be determined by the ability of firms to pair near-term procurement discipline with selective investment in higher-purity capabilities and regulatory readiness. PW Consulting’s full Oxindole Market report provides the quantitative backbone — including historical time series, segmented forecasts, supplier-by-capability assessments and executable checklists — that decision-makers need to convert market insight into resilient, profitable action.

To access the complete dataset, supplier scorecards, and the full suite of strategic tools referenced in this briefing, visit our report page or contact Pw Consulting’s Oxindole practice for a customized executive briefing and data package.

For detailed analysis of this topic, please visit the official page:Oxindole Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com