Nickel Boride Alloy Market — Strategic Outlook and Action Playbook for 2026

PW Consulting’s latest market study on Nickel Boride alloys delivers a pragmatic, decision-focused synthesis intended to guide corporate strategies through 2026 and beyond. Built on a comprehensive historical review (2020–2025) and a forward-looking forecast (2026–2032), the report combines quantitative scenario modelling with operational playbooks. This briefing highlights the report’s strategic value for executives and investors while preserving the full granular datasets and segment-level figures for readers who access the complete report.

Nickel Boride Alloy Market

Market snapshot: trajectory you need to plan for

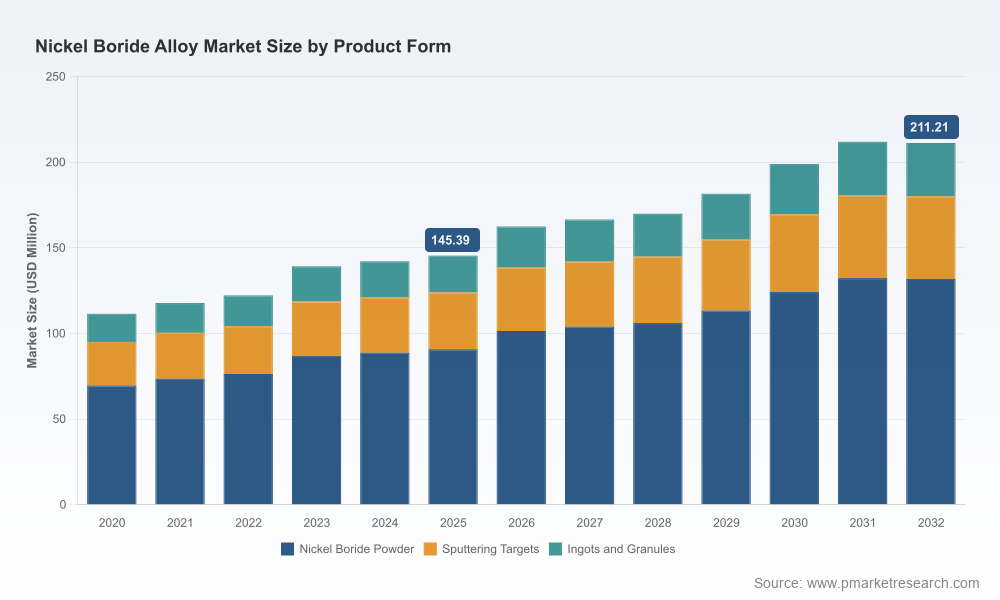

The Nickel Boride market has moved from a niche technical material toward broader industrial relevance, reflecting growing demand across advanced coatings, catalyst technologies and certain semiconductor processes. Our consolidated market model places the industry at USD 145.39 Million in 2025 (base year), with a projected expansion at a compound annual growth rate (CAGR) of 5.48% through the 2026–2032 forecast horizon. The first forecast year (2026) shows a clear step-up to USD 162.43 Million, and the market continues to grow toward the low hundreds of millions by the early 2030s under our central scenario.

Nickel Boride Alloy Market

These headline metrics are not an abstract exercise: they quantify the commercial runway available to suppliers, specialty manufacturers, downstream users, and private capital assessing market entry, capacity expansions, or consolidation plays in 2026.

Nickel Boride Alloy Market

Why 2026 is an inflection point

- Raw-material pressure and volatility: Nickel prices remain a dominant input risk for Ni-containing materials. As of April 30, 2026, nickel was trading near USD 19,457 per tonne, up roughly 28% year-over-year — a fluctuation that materially affects cost of goods sold, margin management and inventory strategies for Nickel Boride producers.

- Policy and trade dynamics: Export controls and resource-nationalization policies (notably Indonesia’s long-standing ore restrictions and select export controls on alloy technologies from some jurisdictions) continue to reshape where value is captured along the nickel value chain. These policy levers alter capital allocation choices — from siting of processing assets to long-term offtake agreements.

- Demand composition shift: While traditional uses (hard-facing, brazing) remain important, higher-value applications—such as catalytic chemistries and specialized sputtering targets—are increasing the premium on quality, consistency and supply security. That composition shift creates differentiated margin pools and strategic asymmetries between suppliers.

What’s in the report — practical, executable content

The report purposefully blends market intelligence with operational guidance. Key deliverables include:

- Top-line market sizing (historical and forecast) with transparent modelling assumptions and sensitivity ranges to test alternate macro scenarios.

- Scenario-driven pricing and margin models that translate nickel price stress into unit-cost impacts and pass-through thresholds for both powder and value-added formats.

- Supplier and capability heatmaps that identify where high-purity NiB, master-alloy production, thermal-spray powders and sputtering target capacity are concentrated — and where gaps open strategic windows.

- A regulatory risk matrix covering export controls, resource nationalism and dual-use policy triggers that can affect cross-border trade and customer qualification timelines.

- Commercial playbooks: customer segmentation frameworks, go-to-market approaches for premium applications (e.g., semiconductor-grade targets, catalysts), and service-product bundles that reduce churn.

- M&A and partnership evaluation rubrics emphasizing capability fit (purity, particle-size control, target fabrication), regional logistics advantage, and integration risk.

- Procurement and hedging templates tailored to NiB producers and major consumers — from short-term rolling hedges to strategic inventory and toll-processing options.

Each module contains worked examples and templates so teams can adapt the tools directly into 2026 planning cycles without reinventing the analytical groundwork.

Competitive landscape — who matters and why

The sector shows a mixed structure: moderate concentration at the top with opportunities for specialized challengers. Our concentration metrics highlight that the top three suppliers account for roughly 44.15% of the market, while the top five reach about 62.8% — a structure that favors both scale players and nimble specialists.

- North American specialists (e.g., American Elements, Stanford Advanced Materials, ESPI Metals): These firms are positioned around high-purity powders and niche product grades required by research, advanced catalysis and semiconductor end-markets. Their differentiation is built on material specification control, traceability and customer qualification expertise.

- European master-alloy players (e.g., KBM Affilips, Westbrook Resources): European suppliers focus on engineered master-alloys and deoxidizer materials tailored to superalloy and hard-facing supply chains. Their strengths are metallurgical know-how and deep OEM relationships.

- Scale and cost-competitive manufacturers (Chinese producers such as Luoyang Golden Egret, Huarui Metal, Xinglu Chemical, and PTG Advanced Catalysts): These companies provide capacity for thermal-spray powders, standard NiB powders and catalyst-grade materials at scale—a critical part of global supply balancing and an important source of competitive pressure on pricing.

Strategic implication: buyers of Nickel Boride can extract value through qualification of dual or multi-source supply strategies—pairing high-purity, higher-cost domestic suppliers for premium segments with cost-effective overseas producers for larger-volume applications—while mindful of lead times, regulatory constraints and quality harmonization.

Strategic imperatives for 2026 decision-makers

For executives preparing 2026 budgets, procurement cycles, or M&A pipelines, this market’s dynamics lead to clear imperatives:

- De-risk feedstock exposure: Implement a tiered procurement strategy combining short-dated hedges, strategic inventory cushions and contractual relationships with refiners/processors in politically diversified jurisdictions.

- Localize or qualify alternate supply where policy risk is highest: For critical customers (semiconductor, defence-adjacent catalysts), local qualification and on-shore buffer capacity reduce the probability of disruptive supply shocks tied to export controls.

- Invest selectively in higher-value product forms: Premiumization — whether through tighter composition control for sputtering targets or engineered morphology for catalytic powders — is a direct path to margin protection against raw-material inflation.

- Use M&A to accelerate capability gaps: Target acquisitions that add either upstream security (tolling/processing) or downstream differentiation (target fabrication, catalyst formulation). Our scorecards identify the capability vectors that best improve enterprise value under multiple market scenarios.

- Adopt continuous scenario planning: Maintain a rolling 18–36 month set of scenarios that stress-test capacity utilization, nickel price shocks, and policy moves, with pre-defined trigger actions for each scenario.

- Operationalize sustainability and circularity: Recycling of Ni-rich scrap and alloy reprocessing can reduce exposure to nickel volatility while meeting rising customer ESG demands.

How to deploy the report in your 2026 planning cycle

Boards, strategy teams and procurement leaders can use the report in multiple, practical ways:

- As the analytical backbone of 2026 capital-allocation debates — quantifying near-term returns from capacity expansion versus long-term strategic M&A.

- For procurement to build supplier scorecards and execute qualification roadmaps that reduce single-source risk for high-priority accounts.

- To inform R&D prioritization — focusing resources on material properties and production techniques that create defensible differentiation in high-margin end-uses.

- By investment committees assessing the risk-adjusted upside of platform plays vs bolt-ons in the Nickel Boride value chain.

Closing: the value of the full dataset

This briefing surfaces the strategic contours and operational levers leaders must weigh in 2026. The full PW Consulting report contains the detailed segment and regional breakdowns, supplier maps, model inputs, and downloadable scenario models required to operationalize these recommendations. We intentionally restrain segment-level dollar disclosures in this synopsis to preserve the depth of the primary publication and encourage teams to consult the complete dataset when making capital and commercial commitments.

To obtain the complete report, with full segmentation datasets, supplier heatmaps and the interactive modelling toolkit, please visit the PW Consulting report page. The comprehensive materials are structured to plug directly into corporate planning workflows and support immediate execution in 2026.

For detailed analysis of this topic, please visit the official page:Nickel Boride Alloy Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com