Tubular Cable Lugs Market — Strategic Imperatives for 2026

Executive summary

PW Consulting’s newly released Tubular Cable Lugs Market report (base year 2025, forecast period 2026–2032) equips executives with the market intelligence and operational playbooks needed to navigate a changing cost, regulatory and demand environment. The global market — measured in USD Million — has expanded steadily from a post‑2020 recovery into a larger industrial segment. In 2025 the market reached USD 432.5 Million and PW Consulting’s near‑term outlook anticipates the market moving to approximately USD 482.1 Million in 2026, before progressing to a projected USD 706.0 Million by 2032 under a central scenario that implies a compound annual growth rate (CAGR) of 7.25% across the forecast horizon.

Tubular Cable Lugs Market

This research is purpose-built for decision-makers preparing budgets, sourcing strategies, product investments and M&A activity in 2026. It balances rigorous quantitative market sizing and scenario analysis with practical, executable recommendations — a “trailer” of insights designed to demonstrate depth while reserving full granular split tables and country-level figures for report subscribers.

Tubular Cable Lugs Market

Why this matters for 2026 decisions

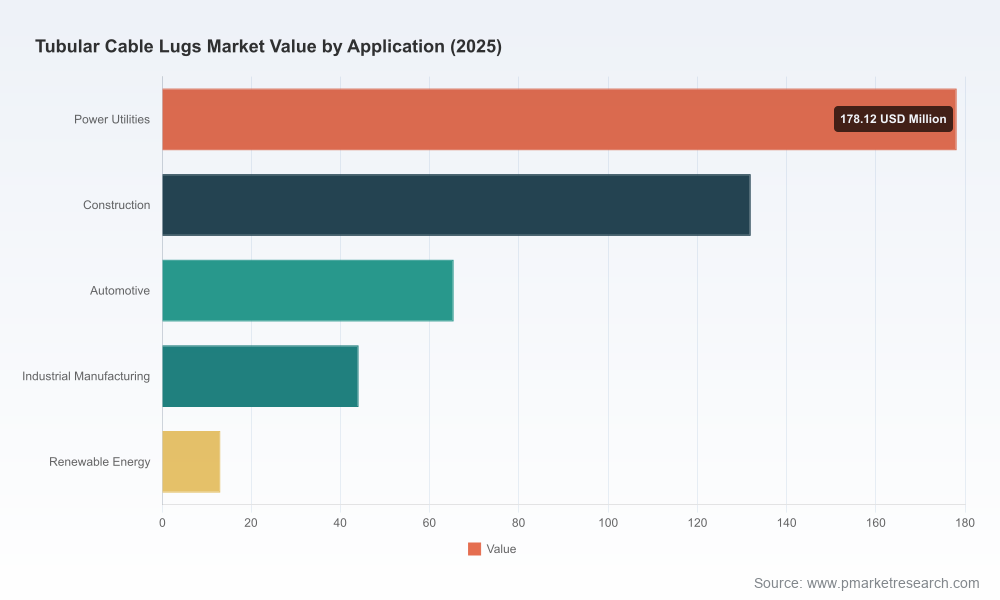

Market momentum and structural forces are creating a window of strategic choices this year. Demand drivers such as grid reinforcement, industrial modernization, electrification of vehicles, and renewable-project rollouts are supporting steady volume growth for tubular cable lugs, while raw material dynamics and tighter technical standards are increasing the importance of supply‑chain resilience, certification and product engineering. The 7.25% CAGR we project for 2026–2032 is not uniform across the market — growth pockets exist, and they will determine who captures margin and scale.

Tubular Cable Lugs Market

Key market dynamics and near‑term risks

- Raw material volatility: Copper and aluminum price swings remain the single largest margin determinant for manufacturers. Notably, copper reached highs of roughly USD 12,000–14,500 per tonne in early 2026, directly pressuring production costs and forcing frequent pricing re‑negotiations across supply chains (Industry Market Data, March 2026).

- Regulatory and technical conformity: Compression and tubular lug products are subject to established dimensional and marking standards (for example, DIN 46235 for copper conductors). Certification and traceability requirements are increasingly enforced by OEMs and utilities, elevating the commercial value of compliance.

- Competitive concentration: The market exhibits moderate consolidation—our concentration analysis shows the top three firms account for a substantial share, and the top five an even larger portion—indicating incumbents hold scale advantages but regional and product specialists can still exploit niche opportunities (CR3 = 38.5%, CR5 = 52.8%).

- Substitution and product mix: Cost pressures and performance needs are fueling selective substitution (e.g., aluminum and bimetallic constructions), affecting product portfolio strategies and inventory mixes.

- Supply chain & logistics risk: Lead times for raw materials and finished components, together with shifting freight dynamics post‑pandemic, require more dynamic inventory and procurement policies.

What’s inside the PW Consulting report (practical highlights)

- Comprehensive market sizing and yearly trajectories (2020–2025 historical, 2026–2032 forecast) presented in USD Million, including central and alternative scenarios and sensitivity testing by price and demand shocks.

- Cost pass‑through and margins model illustrating the commercial impact of copper and aluminum price scenarios on product pricing and profitability.

- Supplier risk heatmap and sourcing playbook: supplier concentration analysis, near‑sourcing vs. low‑cost sourcing tradeoffs, and an action checklist to reduce single‑supply exposure within 90–180 days.

- Product and certification roadmap: requirements matrix against major standards, suggested investment priorities (e.g., DIN/UL/ISO pathways) and a time‑phased certification plan for 12–24 months.

- Commercial playbooks for tendering, channel strategy and aftermarket conversions — templated negotiation levers and pricing guardrails tailored to utilities, OEMs and construction contractors.

- Manufacturing footprint optimization and short‑cycle CAPEX guidance to balance automation, labor and proximity to key cable manufacturers.

- M&A and partnership screen: targets by strategic rationale, synergy estimates, and a phased diligence checklist.

- Primary interviews and supplier intelligence: curated insights from manufacturers, distributors and end users to validate commercial assumptions.

- Downloadable Excel models and executive dashboards to stress‑test strategic scenarios and incorporate internal business data.

Competitive landscape — what incumbents are doing

The market features a mix of established Western engineering specialists and scale-oriented manufacturers from South Asia and China. Across this competitive set, strategies diverge between premium product differentiation, compliance leadership, broad product breadth, and cost-focused scale playbooks.

- Klauke (Germany): Renowned for high‑quality tubular cable lugs crafted from electrolytic copper, often tin‑plated and designed to meet stringent European standards for fine and superfine stranded conductors. Recent product updates (July 2025) to two‑hole lug designs improve compatibility with fine‑stranded cables — an example of feature differentiation that helps sustain pricing power in demanding OEM channels (Klauke Data Sheet, July 2025).

- Pioneer Power International (India): Focuses on a wide product portfolio including copper and aluminum lugs plus heavy‑duty XLPE types; their breadth positions them well for domestic electrification projects and export markets needing higher throughput and competitive pricing.

- MG Electrica (India): An ISO‑certified manufacturer with active catalog and pricing refreshes that signal ongoing production and market engagement. The May 2025 catalog release reaffirms demand continuity and competitive re‑pricing cycles in South Asian markets (MG Electrica Official Price List, May 2025).

- Axis Electricals (India): A UL‑listed supplier offering high‑conductivity ETP copper compression and tubular lugs; certification credentials make Axis an attractive partner for regulated markets and OEMs with strict procurement standards.

- Yueqing Lilian Electric Co., Ltd. (China): A major exporter producing a wide array of lug types; their global distribution footprint makes them a key low‑cost alternative for buyers prioritizing price and lead time flexibility.

- Apple International (India): Specializes in battery cable ends and terminal connectors; their presence underscores the importance of adjacent product diversification for revenue resilience.

Collectively, these firms exemplify the strategic choices open to market players: invest in engineering and certification to command premiums, scale operations to capture volume contracts, or differentiate through regional service and distribution excellence.

Strategic playbook for executives in 2026 (priority actions)

- Hedge and flex raw material exposure: Implement a layered hedging approach (short‑term purchase collars plus medium‑term supplier contracts with escalation clauses) and maintain a rolling 3–6 month safety stock for critical SKUs.

- Targeted certification investments: Prioritize DIN/UL/ISO certifications where they unlock access to high‑margin OEM channels; accelerate certification timelines for products aimed at utilities and renewables.

- Product rationalization and modularization: Reduce SKU complexity by consolidating redundant part numbers and introducing modular platform designs to lower inventory and tooling costs.

- Commercial segmentation and pricing governance: Apply differentiated margin targets and contract terms across customer cohorts (utility tenders, industrial contractors, OEMs) and deploy tactical win‑price thresholds for competitive bids.

- Sourcing diversification and nearshoring assessment: Evaluate nearshore suppliers and regional distribution hubs to shorten lead times and reduce freight volatility; include on‑shore capacity options in disaster recovery planning.

- M&A and partnerships: Use targeted bolt‑ons to gain certification, product breadth or regional access quickly; prioritize targets with validated customer contracts and margin improvement levers.

How PW Consulting helps

For leadership teams making allocation decisions in 2026, PW Consulting’s Tubular Cable Lugs Market report functions as both a strategic compass and an implementation toolkit. We combine market‑level forecasts (USD Million), concentration metrics (CR3 and CR5), cost impact models, supplier risk frameworks and templated commercial playbooks that executives can plug directly into planning cycles. The report deliberately showcases analytical depth while keeping detailed SKU‑ and country‑level tables behind the subscriber portal — ensuring readers see the strategic picture and are invited to access the full dataset and downloadable models.

To access the complete set of segmented tables, country breakdowns, supplier‑level analysis and the downloadable Excel models that power our scenarios, please visit the PW Consulting report page and request the full Tubular Cable Lugs Market package.

PW Consulting — turning market intelligence into 90‑day actions and 3‑year positions. For tailored briefings or to commission a custom variant of this study focused on your product lines, supply base or M&A targets, our industry team is available for direct engagements.

For detailed analysis of this topic, please visit the official page:Tubular Cable Lugs Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com