Handcrafted Silver Jewellery

Other |

2026-06-02 10:27:28

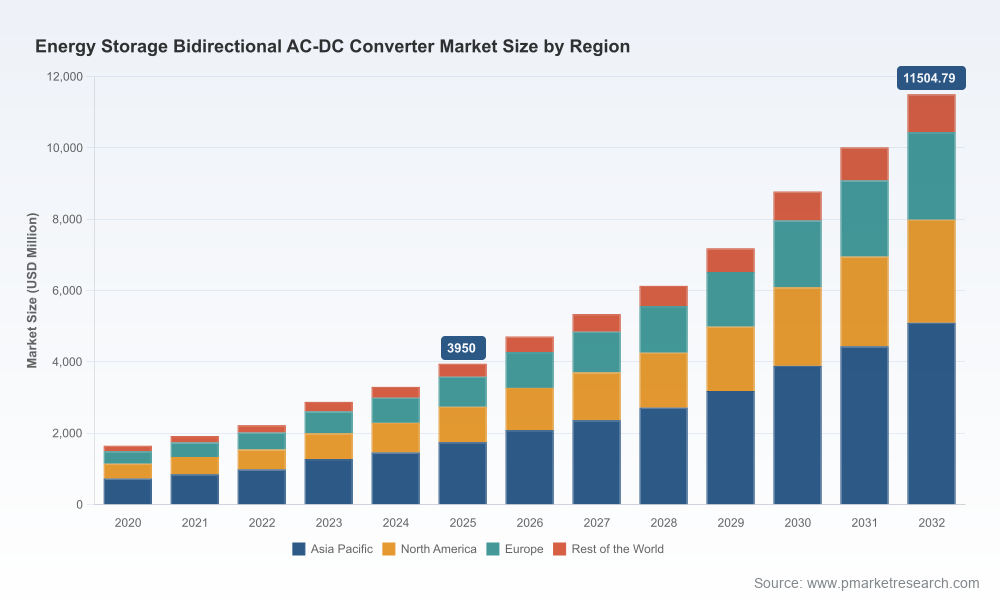

As electrification accelerates and power systems evolve from unidirectional supply chains to interactive, distributed networks, the market for bidirectional AC–DC converters in energy storage is entering a decisive growth phase. PW Consulting’s new market study — covering historical performance through a 2025 base year and projecting across a 2026–2032 forecast horizon — shows a market expanding at a sustained compound annual growth rate (CAGR) of 16.52%. This preview outlines the report’s strategic value for corporate decision-makers in 2026 while deliberately holding back granular segment tables and regional allocations to encourage direct engagement with the full report.

Energy Storage Bidirectional Ac Dc Converter Market

Strong macro growth: The global market crosses a notable milestone in the report’s 2025 base year and is projected to more than double by the end of the forecast window, reflecting accelerating adoption of bidirectional power conversion across utility, C&I and residential contexts.

Energy Storage Bidirectional Ac Dc Converter Market

Industry consolidation and differentiation: Market concentration indicators show a moderately concentrated vendor landscape — sufficient scale among leaders to move market levers, but with meaningful opportunity for specialized challengers and regional players.

Energy Storage Bidirectional Ac Dc Converter Market

Strategic inflection points for buyers and vendors alike: Regulatory updates, raw-material price trajectories, and technology modularity are creating short windows in 2026 for securing supply, locking-in design architectures, and forming project-first partnerships.

Actionable market sizing and growth pathways: A year-by-year topline model (historical 2020–2025 and forecast 2026–2032) expressed in USD (revenue unit: Million), enabling scenario planning for CAPEX and product roadmaps.

Segment-level intelligence (kept behind the paywall): granular coverage by region, power-rating band and end application with demand drivers, adoption curves, and supply-side capacity maps — intentionally summarized here at a thematic level to preserve strategic exclusivity.

Vendor scorecards and go-to-market playbooks: comparative analysis of technology architectures, efficiency benchmarks, scalability, and commercial models; procurement checklists and supplier negotiation levers tailored to different buyer archetypes.

Project pipeline and deployment risk matrix: a prioritized list of near-term project opportunities, policy-driven demand pockets, and failure-mode analyses relevant to EPCs, integrators and asset owners.

Cost and margin trees: detailed build-up of typical BOM and system-level cost drivers, plus sensitivity testing across raw-material pricing scenarios and CAPEX declines projected by independent sources.

Procurement and contract timing: By mapping supplier capacity, certification lead times and recent product introductions, we identify optimal windows to secure MW-scale converter supply without premium time-risk exposure.

Product strategy and differentiation: Technical profiles and efficiency benchmarks allow R&D and product leaders to prioritize investments in modular three-level topologies, liquid cooling, and integrated V2G interfaces that unlock premium segments.

Partnerships and M&A screening: The study’s vendor scorecards and concentration metrics enable acquirers to triage targets by technology complement, addressable market overlap, and integration risk.

Regulatory and compliance roadmaps: Our scenario analysis links emerging regulations — including recent building-code updates and executive orders — to procurement standards and product certification priorities for 2026 deployments.

The vendor ecosystem spans global conglomerates to nimble power-electronics specialists. Leading multinational suppliers bring high-power portfolios and grid-experienced control stacks suited to utility-scale deployments, while a cohort of focused vendors competes on power-density, modularity and application-specific integration (e.g., EV-to-grid, residential hybrid packs).

Long-established power-electronics leaders: These players offer high-power PCS and integrated BESS solutions with strong grid-compliance credentials. Their scale and service footprints are decisive for multi-MW, utility-facing projects and for customers requiring lifecycle O&M propositions.

China-based and regional innovators: Several manufacturers have optimized high-efficiency, compact bidirectional AC–DC and DC–DC modules for C&I, residential and V2G use cases. Their rapid product refresh cycles and competitive cost structures make them important partners for volume-driven deployments.

Specialist converter manufacturers: Firms focusing on DC–DC architecture, energy recovery and hybridization (e.g., for supercapacitor or hybrid battery systems) position themselves as technology enablers for niche applications such as fast frequency response and microgrids.

PW Consulting’s report provides vendor profiles that distill each supplier’s technical differentiation, typical application fit, recent announcements, and likely positioning across the 2026 opportunity set. For example, the landscape includes companies offering high-efficiency three-level topologies and modular cabinets that scale to the multi-MW range, suppliers focused on V2G-enabled residential and EV-integration modules, and specialists targeting power-dense DC–DC solutions for energy recovery.

Product push from regional manufacturers: Early-2026 product launches underscore the market’s rapid iteration. New mid-power bidirectional converters sized for on-grid/off-grid ESS expand options for integrators and lower technical barriers for smaller projects.

Project activity: Commissioning events for MW-class systems and awarded contracts for large storage projects demonstrate commercial traction and provide reference cases for procurement due diligence.

Policy drivers: New building codes and executive directives in major markets are raising baseline requirements for storage integration and grid reliability assessment. These policy shifts tighten technical specs for converters and can accelerate demand for certified, grid-compliant products.

Raw-material and system-cost trends: Independent cost projections for utility-scale batteries and observed price points for stationary LFP cells are compressing total BESS CAPEX. This shifts the commercial emphasis toward higher-value system integration, lifecycle services and converter-level efficiency gains.

Supply-chain concentration: Components and subassemblies remain exposed to geographic concentration. Mitigation options include multi-sourcing, forward-buy contracts, and commodity hedging tied to clearly modeled sensitivity cases.

Regulatory headwinds: Emerging standards and carbon-pricing mechanisms can alter procurement economics; proactive certification strategies and participation in standards working groups reduce market-entry friction.

Technology obsolescence: Rapid improvements in converter topologies and cooling can change product lifecycles. Adopt modular architectures and procurement clauses for upgradeability to protect asset value.

Board-level briefing: Use the topline market trajectory and concentration metrics to set investment thresholds, M&A screening criteria, and target ROIs for storage-linked opportunities.

Procurement RFP design: Leverage the vendor scorecards and BOM sensitivity models to craft RFPs that align product specs, service SLAs and commercial terms with the buyer’s risk appetite.

Technology roadmap alignment: Product and systems teams should map their development timelines to the expected cadence of converter efficiency and power-density gains identified in the study.

Strategic partnerships: The report identifies likely partnership archetypes — from turnkey integrators to component specialists — and offers negotiation playbooks for JV and licensing structures.

Our estimates are based on a bottom-up market construction rooted in historical deployments (2020–2025), primary supplier interviews, project-level commissioning data and cross-validated cost models. External sources on battery cost trajectories and regional regulatory changes were incorporated to stress-test scenarios. The 2026–2032 forecast reflects a central-case CAGR of 16.52% and includes upside and downside pathways driven by policy, raw-material price variance and technology adoption curves.

This preview highlights the decision-making value embedded in PW Consulting’s full Energy Storage Bidirectional AC–DC Converter Market report: granular, actionable intelligence designed to inform procurement, product strategy, M&A and regulatory engagement in 2026. To access the complete dataset (regional and application breakouts, supplier scorecards with quantitative rankings, detailed cost tables and downloadable models) visit our official report page or contact PW Consulting’s advisory team for a tailored briefing.

For executives planning capital allocation, technology selection or partnership strategies this year, timing matters: early access to segment-level demand forecasts and supplier capacity maps materially improves negotiation leverage and reduces execution risk. PW Consulting’s full report gives you that edge.

For detailed analysis of this topic, please visit the official page:Energy Storage Bidirectional Ac Dc Converter Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com