Global Diphenhydramine Market Trends and Forecast 2031: Strategic Insights Driving Steady Growth

Health |

2026-02-24 06:45:17

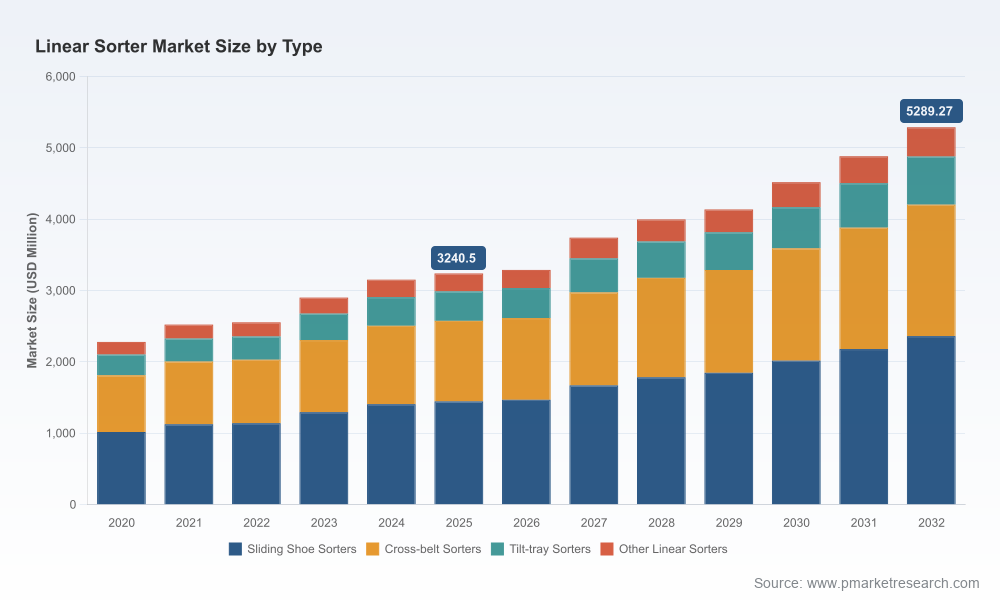

PW Consulting’s latest Linear Sorter Market report positions procurement teams, operations leaders, integrators and investors to make high‑conviction decisions in 2026. The global market continues its multi‑year recovery and expansion—from roughly USD 2.28 billion in 2020 to USD 3.24 billion in our 2025 base year—and is forecast to grow to more than USD 5.28 billion by 2032. Our modelling for the 2026–2032 forecast period yields a compound annual growth rate of 7.25%, driven by persistent e‑commerce volume growth, warehouse automation strategies, and the need to substitute labor with high‑throughput mechanized sortation.

Linear Sorter Market

Timing of capital deployment: With measurable momentum from 2023–2025, 2026 is a window in which late adopters can still secure advantageous pricing and integration slots before a second wave of large rollouts in the back half of the decade.

Linear Sorter Market

Technology choice will lock operating models: Decisions between sliding‑shoe, cross‑belt, narrow‑belt and other linear architectures now determine throughput ceilings, maintenance profiles, and expansion pathways for the next 8–12 years.

Linear Sorter Market

Supply chain and raw material volatility: Structural reliance on steel and complex electromechanical components makes procurement strategies sensitive to metal markets and long‑lead electronic components.

The market’s rebound since 2020 reflects two overlapping dynamics: secular growth in parcel volumes and an accelerated corporate push to automate at scale. Between 2020 and 2025 the sector expanded materially, and our base‑case projects continued expansion through 2032 with accelerating absolute dollars as facility modernization and retrofit investments compound. The 7.25% CAGR we forecast for 2026‑2032 is a function of both greenfield distribution center construction in high growth regions and large‑scale retrofit programmes in mature markets.

Key macro drivers informing our scenarios:

E‑commerce density and parcel mix: demand for modular, high‑speed sortation capable of handling heterogeneous package sizes is the principal demand lever.

Labor and regulatory dynamics: rising labor costs, workforce scarcity and, in specific cases, craft determinations (notably recent national craft assignment activity in mail induction operations) are accelerating the substitution of manual operations with mechanized induction and sortation.

Input cost and supply chain noise: exposure to steel and specialty component markets creates near‑term margin and procurement risk for OEMs and integrators; buyers need procurement hedges and vendor risk assessments.

Market sizing and conservative/optimistic scenario models with sensitivity to parcel growth, steel costs and service network constraints.

Vendor scorecards and procurement checklists: technical capability, footprint, spare‑parts lead times, integrated controls maturity and field service coverage.

Technology decision matrix to match sortation architecture to throughput, footprint and package mix objectives.

TCO templates and ROI calculators with realistic depreciation, maintenance curves and upgrade paths used by leading operators.

Implementation playbook: pilot design, commissioning checkpoints, KPI targets and common integration pitfalls.

Case studies and failure mode analyses from recent deployments across e‑commerce, parcel, food & beverage and pharmaceutical environments.

The linear sorter vendor ecosystem is a blend of global integrators, specialized OEMs and regionally strong manufacturers. Market concentration is meaningful: the largest three suppliers account for roughly two‑fifths of the market’s revenue, while the top five account for just over half. That structure creates a tiered procurement landscape—global incumbents offer integrated systems and service networks; regional suppliers compete on price, modularity and space‑constrained innovations.

Fives Intralogistics (France) — Strengths: high‑speed parcel shoe sorters and established product families suited to parcel hubs. Strategic positioning: focuses on throughput and accuracy for high‑velocity parcel sortation; visible at industry events with new entries in 2025 product lines.

BEUMER Group (Germany) — Strengths: integrated loop and linear solutions tailored to distribution network topologies. Strategic positioning: competes where integrators need seamless conveyor ecosystems and long service contracts.

Dematic (KION Group) (Germany/USA) — Strengths: modular FlexSort architectures for high‑volume package and carton sortation. Strategic positioning: favored by large omnichannel retailers and 3PLs undertaking cross‑dock and high‑density sortation projects.

Wayzim (China) — Strengths: compact vertical circulating layouts optimized for constrained footprints. Strategic positioning: attractive option for operators retrofitting inner‑city or brownfield sites where space is the primary constraint.

ConfirmWare (China) — Strengths: narrow belt solutions with strong compatibility across mixed package sizes. Strategic positioning: differentiates on package handling flexibility; demonstrated new narrow‑belt offerings at LogiMAT show focus on mixed small/large SKU environments.

Honeywell Intelligrated / Transnorm (USA/Germany) — Strengths: SmartSort shoe sorters with very high hourly throughput and modular platform design. Strategic positioning: used where maximized throughput and phased scaling are needed.

Vanderlande (Netherlands) — Strengths: comprehensive, high‑speed sorting systems in integrated automated portfolios. Strategic positioning: often chosen for critical parcel and airport sortation projects where uptime and systems integration matter most.

Okura Yusoki (Japan), Intralox (USA), Gosunm (China) — Strengths: specialist offerings from cross‑belt to container‑direct sortation and induction systems. Strategic positioning: these players are selected where specific package types or industrial use cases require niche engineering.

Fives showcased expanded sorting solutions at major parcel industry events in late 2025, signaling renewed go‑to‑market activity on parcel automation programs.

ConfirmWare’s narrow belt demonstrations at a leading trade show underscored the market appetite for solutions that increase compatibility across mixed package fleets.

Intralox won a contract to deliver modifications to a Parallel Induction Linear Sorter variant, highlighting continuing investment in induction technologies for specialized package handling.

Adopt a modular procurement stance: specify upgrade paths and bolt‑on controls rather than monolithic, irrevocable builds to preserve optionality as volumes and parcel mixes shift.

Prioritize spare‑parts logistics and regional service footprints in vendor selection—installation uptime and mean time to repair will often drive value more than headline throughput specs.

Run a two‑track RFP: one for brownfield retrofits focusing on footprint‑efficient architectures; another for greenfield high‑throughput solutions emphasizing throughput and automation density.

Stress‑test procurement against raw material and electronics price shocks; secure caps or hedges where capital budgets are exposed to long supplier lead times.

Factor regulatory and labor dynamics explicitly into ROI models—workforce classifications and craft determinations can materially alter operating cost forecasts and rollout timing.

Plan pilot‑to‑scale roadmaps with clear KPI gates: measure throughput, first‑time sort accuracy, rejects and maintenance man‑hours per thousand items as gating metrics before full system expansion.

Input cost inflation: steel and component cost swings can compress OEM margins or force lead time extensions; buyers should model multiple procurement timing scenarios.

Service network concentration: reliance on a small number of field engineers increases downtime risk—consider hybrid contracts that combine OEM support with certified local partners.

Technology lock‑in: mismatched architectures may require expensive rip‑and‑replace upgrades as throughput needs evolve.

Regulatory shifts affecting who can perform induction and sortation tasks (craft assignments) may create near‑term operational constraints in postal and mail spaces.

Operational leaders should use the report’s ROI templates and vendor scorecards during vendor selection and budget prioritization cycles. Strategic teams will find the scenario models and concentration mapping useful for M&A and partnership diligence. Implementation teams should follow the pilot‑to‑scale playbook to reduce install risk and to shorten time‑to‑value.

We intentionally present high‑level market sizing and vendor positioning in this release to guide initial decision pathways. For full access to segmented demand tables, regional and application breakdowns, detailed vendor scorecards, supplier pricing benchmarks and our downloadable ROI calculators, please refer to the PW Consulting report hub—these granular datasets and procurement tools are included in the full report and subscription portal.

For enterprises setting 2026 capex envelopes or re‑architecting sortation strategies, the choices made this year will define operating cost structures and service capabilities for the rest of the decade. PW Consulting’s Linear Sorter Market report gives decision‑makers the actionable intelligence—analytical frameworks, vendor playbooks, and scenario models—they need to translate forecasted market momentum into defensible investment and execution plans.

For detailed analysis of this topic, please visit the official page:Linear Sorter Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com