Used Golf Cart Market 2026: Strategic Preview — What Boards and Business Units Must Know Now

PW Consulting’s latest market intelligence on the global used golf cart market delivers a concise, decision-focused briefing for executives preparing capital, product, and channel strategies in 2026. This preview highlights the macro trajectory, competitive dynamics, regulatory and supply-chain inflection points, and the practical operating levers that will determine winners in the secondary market. It deliberately surfaces the strategic implications while reserving detailed segment-level tables and model-level valuations for the full report available on our site.

Used Golf Cart Market

Executive snapshot: steady growth, accelerating electrification

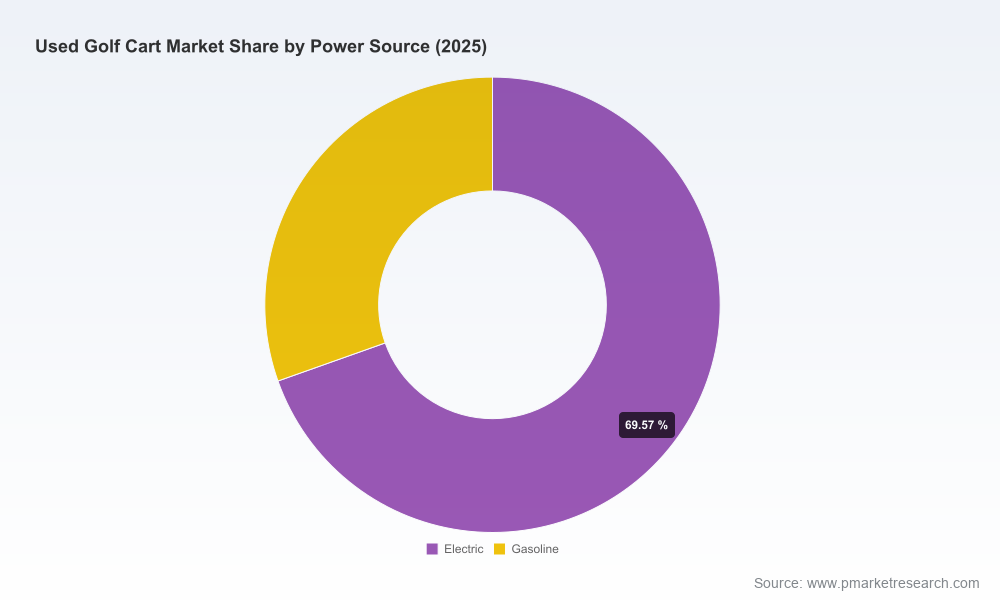

The used golf cart market has expanded meaningfully over the past half-decade, rising from a base below USD 1.4 billion in 2021 to an estimated USD 1.75 billion in 2025 (base year). Our forecast projects continuity of that momentum into 2026 — with a near-term market value in the neighborhood of USD 1.86 billion and a compounded annual growth rate (CAGR) of roughly 6.25% through the 2026–2032 forecast window. This growth is sustained by three interacting forces: lifecycle refreshes from robust new-unit sales, accelerating adoption of lithium powertrains in replacement and refurb programs, and expanding non-golf end uses that are monetizing used-unit affordability.

Used Golf Cart Market

Why this matters for 2026 corporate decisions

- Capital allocation: OEMs and fleets must decide how much to invest in certified pre-owned (CPO) refurbishment capacity versus new-unit production. With predictable volume growth and rising resale value for electrified units, targeted investment in standardized reman lines yields outsized ROI compared with low-margin ad hoc refurbishment.

- Product strategy: Electrification is no longer optional for the secondary market. Lithium upgrades and BMS-enabled batteries are becoming the feature that preserves realized value and reduces total cost of ownership for buyers.

- Channel & partnerships: Dealer networks, independent refurbishers, and logistics partners are the lifeblood of secondary-market velocity. Firms that move from transactional exchanges to subscription-style certified programs capture higher lifetime value.

- Compliance & risk: Regulatory changes affecting batteries and transport materially influence logistics cost and time-to-market for refurbished inventory. Compliance planning must be embedded in 2026 operations.

What the full report contains — practical outputs for execution

PW Consulting’s report is structured to convert insight into action. Key pragmatic deliverables include:

Used Golf Cart Market

- Operational playbooks for CPO programs: refurbishment workflows, quality gates, and parts sourcing matrices that reduce rework and warranty claims.

- Fleet disposition frameworks: decision tools to determine holding periods, refurbishment thresholds, and resale channel selection to maximize net realized proceeds.

- Battery upgrade and warranty models: sensitivity analyses that compare lead-acid-to-lithium conversion economics under multiple TCO scenarios and lifecycle assumptions.

- Compliance checklist and logistics playbook: a step-by-step guide to battery certification requirements, air/ground transport constraints, and documentation to avoid shipment delays and fines.

- Commercial templates: margin-by-channel pricing guidelines, trade-in program terms, and dealer incentive structures proven in pilot implementations.

- Executive scorecards and scenario dashboards: a modular set of metrics and forecasts to stress-test capital allocation decisions under varying electrification and price scenarios.

The full dataset and model workbook remain behind the report’s access portal to protect commercial sensitivity and to support client-tailored exports — this preview intentionally omits granular regional and end-use breakouts to encourage direct engagement with our analysts.

Competitive landscape — what incumbents and challengers are doing

The competitive map in 2026 is a mix of traditional OEMs leaning into certified pre-owned offers, specialty electric OEMs feeding abundant pre-owned inventory, and independent refurbishers consolidating value chains. Market concentration remains moderate: the leading three players account for just over thirty percent of the market, and the top five for under half. This structure creates room for scale advantages through branded CPO programs, while also allowing nimble players to win on speed and cost.

- Club Car, LLC — Club Car has leaned heavily into multi-tiered refurbishment and branded CPO offerings, pushing lithium options and enhanced customization packages. Their strategy focuses on warranty-backed, dealer-distributed pre-owned units that preserve brand value while accelerating turnover.

- E‑Z‑GO (Textron Specialized Vehicles) — E‑Z‑GO’s approach centers on factory-inspected refurbishment with systematic parts replacement and battery refresh programs. Emphasis on integrating newer MY25/MY26 technology into CPO inventory helps maintain resale premiums.

- Yamaha Golf‑Car Company — Yamaha leverages dealer networks and reputation for durability to sustain higher resale values for select models, making them a consistent source of desirable secondary inventory.

- ICON EV, Evolution Electric Vehicles, STAR EV, Tomberlin — These electric-native and neighborhood-LSV manufacturers contribute high-volume, feature-rich pre-owned inventory. Their market presence accelerates the normalization of lithium and street-legal configurations in the used segment.

- Cushman (Textron) & Garia (integrated via acquisition) — Utility-focused and premium-luxury playbooks respectively demonstrate how segment positioning translates into differentiated secondary price curves and buyer cohorts.

Strategically, OEMs that align their new-unit roadmaps with certified refurbishment standards (standardized removable battery packs, modular body components, documented service records) reduce refurbishment cost and increase resale velocity. Independent refurbishers that secure repeatable parts flows and battery supply contracts can undercut OEM CPO pricing while maintaining acceptable margins.

Regulatory and supply-chain dynamics shaping 2026 choices

- Battery cost and technology: Lithium system costs continue to decline at an estimated annual rate of 5–10% driven by manufacturing scale. Practically, this makes lithium upgrades the preferred economics for many refurbishments; lithium packs deliver thousands of cycles versus low hundreds for legacy lead-acid systems, materially improving total cost of ownership for buyers.

- Safety & certification: UL 2271 is the de facto safety benchmark for lithium battery systems in light electric vehicles; CPO programs that do not require UL-compliant packs expose sellers to heightened warranty and liability risk.

- Regulatory timing: European battery rules requiring harmonized safety and BMS provisions (and the CE mark for batteries) come into force across many jurisdictions, forcing inventory screening and remediation prior to cross-border sales.

- Logistics constraints: Air transport regulations effective from January 1, 2026, require state-of-charge limitations for batteries intended for air shipment. This impacts the speed and cost of international resale and remarketing programs; firms that pre-certify and stage inventory geographically maintain higher conversion rates.

- Component pricing: Bench-level price points for a full 48V lithium set are now visible in supply channels; while ranges vary by chemistry and supplier, procurement teams must bake realistic battery replacement costs into residual-value models.

Risk checklist for boards and operating teams

- Underestimating certification costs and logistics friction for cross-border battery shipments.

- Failing to standardize refurbishment specifications across dealer networks, leading to inconsistent product quality and brand dilution.

- Overexposure to a single battery supplier or chemistry without contingency for price spikes or supply disruptions.

- Pricing CPO units purely on vehicle age or hours without accounting for battery health metrics and BMS data — a leading cause of post-sale claims.

Actionable recommendations for 2026

- Establish a center of excellence for certified pre-owned operations to codify inspection standards, battery acceptance criteria, and warranty playbooks.

- Negotiate multi-year battery supply agreements with indexed pricing and capacity guarantees, and require UL-compliance and traceable BMS telemetry as part of contracts.

- Invest in quick-turn staging hubs near key dealer clusters to avoid air shipment constraints and to shorten remarketing cycles.

- Pilot subscription or guaranteed buyback programs for high-turnover fleets — these improve resale predictability and customer retention.

- Deploy data capture at point of maintenance (battery cycles, charge profiles, component replacements) to enable model-level residual forecasting and dynamic pricing engines.

Conclusion — what to do next

2026 is a year for pragmatic moves rather than speculative leaps. The macro picture supports continued expansion of the used golf cart market at a mid-single-digit CAGR; companies that convert that growth into predictable cash flow will be those who standardize refurbishment, secure battery supply and certification, and build faster distribution channels. PW Consulting’s full report provides the detailed scenario models, regional and end‑use breakouts, OEM and model-level valuations, and implementation toolkits to operationalize these recommendations.

For clients and executives ready to translate these strategic signals into 2026 budgets and operating plans, our analysts are scheduling advisory sessions to walk through the full data set, custom model exports, and tactical roadmaps. Access the detailed report and request a briefing via the PW Consulting reports portal.

For detailed analysis of this topic, please visit the official page:Used Golf Cart Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com