Increasing Vegan Adoption Fuels Frozen Pizza Market Growth Worldwide

Food |

2026-04-22 17:27:55

As fertility care climbs higher on national health agendas and alternative patient access models reshape treatment economics, senior executives, corporate strategists, and investors must recalibrate decisions for 2026 and beyond. PW Consulting’s latest market study — built on a five‑year historical base (2020–2025) and a 2026–2032 forecast horizon — delivers precisely the forward-looking, actionable intelligence needed to navigate this evolving landscape.

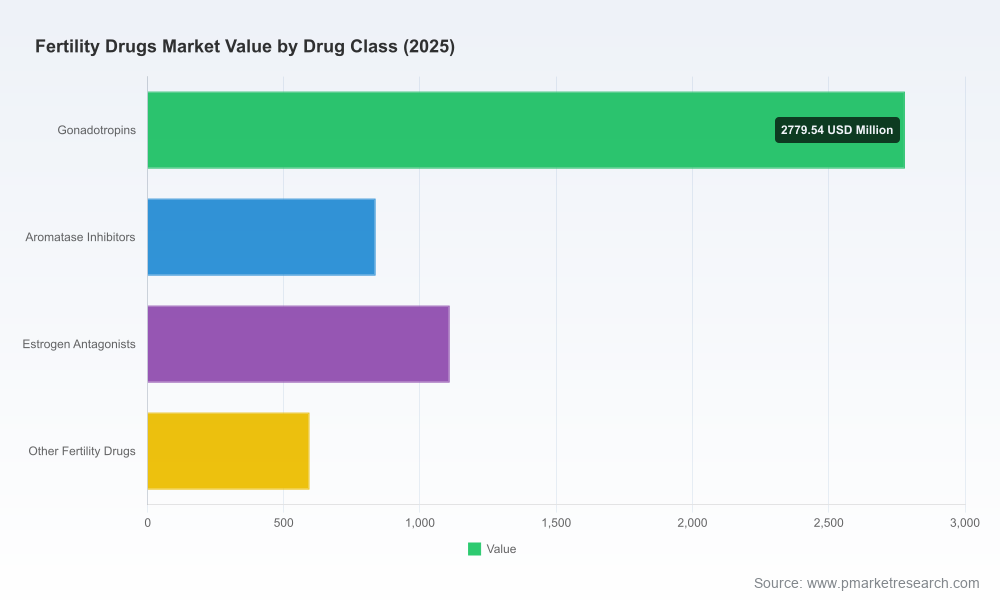

Fertility Drugs Market

Validated market trajectory: Our market model shows a clear multi‑year growth path from the 2025 base through 2032, underpinned by a 6.1% compound annual growth rate in the forecast period. That trajectory encapsulates demand growth, pricing dynamics and product mix shifts that will affect capital allocation and portfolio prioritization throughout 2026.

Fertility Drugs Market

Strategic inflection points: The report identifies the commercial, regulatory and supply‑chain inflection points that will decide winners and laggards — from biosimilar launches and generic expansion to policy interventions and episodic product shortages.

Fertility Drugs Market

Decision‑ready outputs: We translate data into decision frameworks — investment prioritization, M&A screening, manufacturing resilience plans, and go‑to‑market playbooks — so leaders can move from insight to execution within months, not quarters.

PW Consulting’s topline model traces the fertility drugs market from its documented historical position in 2020 through a 2025 base year and projects forward to 2032. The market expanded steadily across the historical window and, under our central scenario, continues to expand at a steady mid‑single‑digit CAGR of 6.1% through the forecast period — a profile that supports both continued organic investment in established franchises and selective inorganic moves to secure scale and access.

Critically, the forecast is scenario‑based: we model downside risks from regulatory contraction and supply disruption, and upside from accelerated private‑pay D2C models and biosimilar adoption. Each scenario is mapped to actionable financial and operational sensitivities so executives can stress‑test choices before committing capital.

The competitiveness of the fertility drugs market reflects a blend of large multispecialty pharmaceutical groups, specialized reproductive medicine companies, established generics players and an emerging biosimilar cohort. Market concentration is meaningful: a compact set of multinational and specialist firms exert strong influence over clinical protocols, pricing norms and distribution channels. In this environment, strategic plays must be tailored to your role—incumbent, challenger or new entrant.

Multinationals with full portfolios: Leading global firms maintain broad fertility portfolios spanning recombinant gonadotropins, antagonist protocols and support hormones. Their advantages include integrated R&D, validated cold‑chain manufacturing, and established clinical relationships with IVF clinics and key opinion leaders.

Specialist reproductive players: Companies focused on reproductive medicine hold depth in protocol design and physician engagement; they act as innovation incubators and commercial partners for scale players seeking credibility in the fertility clinic channel.

Generics and biosimilar entrants: A growing set of generic manufacturers and biosimilar developers are compressing price points for core agents used in ovulation induction and IVF cycles. These entrants change margin dynamics and expand access, especially in cost‑sensitive markets.

Regional champions: Firms with deep local manufacturing and distribution capabilities can rapidly capture volume shifts where payers or clinics rationalize suppliers.

PW Consulting’s full report contains independent profiles and strategic-positioning maps for each major competitor, including recommended partnership and response strategies — reserved for subscribers and clients.

Generic expansions: Late‑stage and recent launches of generic equivalents for core agents have already started to alter pricing dynamics and treatment choices in multiple markets. Expect accelerated tendering activity and greater bargaining power for purchasers.

Product shortages: Episodic supply constraints in key biologics have surfaced, with regulators flagging intermittent shortages for some established gonadotropin products. These events crystallize the need for inventory strategy and alternate sourcing plans.

Policy shifts: Recent government‑backed initiatives targeting IVF drug pricing and distribution models introduce new commercial routes to patients, including direct‑to‑consumer and federally supported programs. These initiatives increase pricing transparency but also add policy execution risk for manufacturers.

Each of these drivers is modeled in our scenario suite, with quantified impacts on revenue, margin and clinic uptake under alternate timelines.

Methodology and data transparency: Detailed modeling assumptions, primary‑research interview summaries, and a reproducible forecasting engine so clients can re‑run scenarios with their proprietary inputs.

Market sizing and trend decomposition: A granular decomposition of the overall market growth drivers — demographic demand, treatment intensity, protocol evolution and price dynamics — with sensitivity analyses for each.

Regulatory and reimbursement matrix: Country‑level policy mapping, reimbursement levers, and payer behavior archetypes to support market access strategies.

Supply‑chain risk register: Sourcing maps for biological APIs, cold‑chain vulnerability scoring, and recommended mitigation investments for near‑term resilience.

Commercial playbooks: Segmented GTM options for branded, biosimilar and generic launches, including clinic engagement frameworks, digital patient acquisition models, and pricing tactics under competitive and policy pressure.

M&A and partnership scorecards: A prioritized list of strategic targets and partner archetypes aligned to inorganic growth, capability fills and market entry objectives — with valuation stress tests under multiple regulatory outcomes.

Operational KPIs and implementation roadmaps: Short‑term (0–18 months) and medium‑term (18–36 months) action plans with deliverables, resource needs and success metrics tailored for manufacturer, investor and clinic stakeholders.

Portfolio rationalization: Use our scenario outputs to decide which molecules merit continued investment, which should be out‑licensed, and where biosimilar entry risks necessitate accelerated lifecycle actions.

Manufacturing and supply decisions: Rebalance production footprints to reduce single‑source exposure for biologics, and evaluate contract development/manufacturing partnerships to enable rapid scale‑up when shortages or tender wins occur.

Commercial strategy: Adopt differentiated patient access models (e.g., hybrid clinic+D2C), refine clinic incentive structures, and prepare value dossiers demonstrating cost per live birth improvements under evolving reimbursement regimes.

M&A and investment screening: Prioritize targets that provide either capacity for biosimilar/biologics production, clinic channel access, or proprietary assets that can extend protocol franchises beyond price‑sensitive categories.

Public affairs and policy engagement: Build anticipatory strategies for new pricing and distribution interventions, including stakeholder coalitions with clinic networks and patient groups to shape implementation detail.

Our risk register highlights several watch items for 2026 decision cycles: rapid biosimilar approvals in key markets, new federal procurement models that shift margin pools, intermittent biologic supply disruptions, and clinic consolidation changing purchasing behavior. For each risk we provide early warning indicators — market signals, regulatory filings, and procurement tender patterns — so clients can act before downside outcomes crystallize.

This preview is designed to surface the strategic value of PW Consulting’s full Fertility Drugs Market report for leaders making 2026 decisions. The complete report contains the full datasets, methodology, company scorecards, and executable playbooks that we only summarize here to protect source depth and competitive sensitivity.

Clients who commission the full report receive: ongoing update briefings as the 2026 landscape evolves, a working model with scenario toggles for bespoke inputs, and a tailored executive workshop to translate insights into a 90‑day action plan.

Fertility therapeutics in 2026 sits at the intersection of robust demand growth and accelerating disruption from generics, biosimilars and policy reform. That combination creates both opportunity and execution risk. PW Consulting’s analysis converts macro momentum into granular strategy: where to invest, where to partner, where to defend — and when to step back. For executives seeking to lead rather than react, the levers are clear; the timing is now.

To access the full report, data tables, and company playbooks, visit our report page or contact PW Consulting directly for a briefing and model license.

For detailed analysis of this topic, please visit the official page:Fertility Drugs Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com