Coal Tar Pitch for Graphite Electrodes: Strategic Insight Briefing — PW Consulting

Executive preview

As electric arc furnace (EAF) steelmaking and specialty carbon applications continue to recalibrate global metal and materials supply chains, coal tar pitch — the feedstock and binder for graphite electrodes — is once again in the strategic spotlight. PW Consulting’s new market study on Coal Tar Pitch for Graphite Electrodes provides C-suite and procurement leaders with an actionable intelligence package tailored to 2026 decision cycles: a rigorous market sizing, scenario-driven forecasts, competitive benchmarking, cost-and-compliance playbooks, and deal-ready acquisition and outsourcing scenarios.

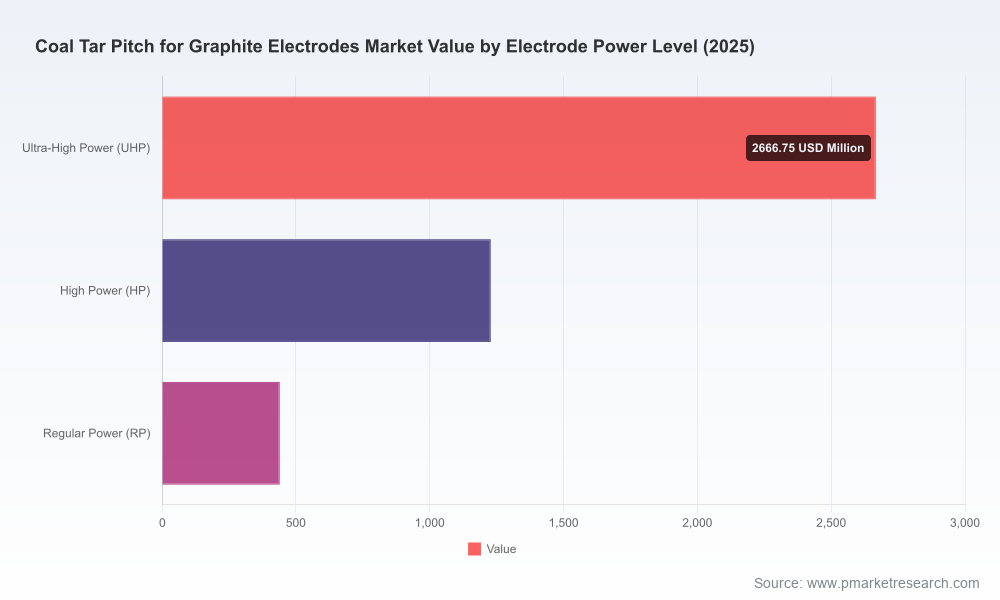

Coal Tar Pitch For Graphite Electrodes Market

Market snapshot (why the timing matters)

Our analysis consolidates observed dynamics from 2020–2025 and projects the market through 2032. The market showed steady expansion in the 2020–2025 base period and, under our base forecast, is expected to grow at a compound annual growth rate (CAGR) of 5.61% during 2026–2032. The market reached a multi-billion-dollar scale by the 2025 base year and is forecast to be materially larger by 2032, reflecting a mix of capacity additions, rising graphite electrode consumption tied to EAF penetration, and product upgrades for higher-power electrode grades.

Coal Tar Pitch For Graphite Electrodes Market

This trajectory is not linear: short-term pulses from raw material cost swings, regulatory compliance investments for emissions and PAH control, and geopolitically driven trade measures create windows of margin compression and selective margin expansion. For companies planning capital allocation in 2026, reading the directional market scale and growth profile is necessary but not sufficient — firms must pair scale outlooks with supplier concentration, cost curve placement, and regulatory exposure to make resilient choices.

Coal Tar Pitch For Graphite Electrodes Market

What the report contains — practical value for 2026 decisions

- Integrated market model with base-year reconciliation (2025) and scenario runs to 2032 — enabling stress-testing of capacity investments, pricing assumptions and feedstock shocks.

- Supplier and feedstock cost mapping — cost stack models that isolate feedstock, processing, and compliance cost drivers so you can evaluate insourcing, long-term sourcing, or tolling arrangements.

- Competitive benchmarking and capability matrix — technology and grade mappings (binder, impregnation, UHP-grade compatibility), capacity footprints, and approval/qualification status versus major electrode manufacturers.

- Regulatory and compliance roadmap — emissions and PAH control capital estimates, compliance timelines by major regulatory regimes, and recommended technology levers to reduce regulatory risk exposure.

- Commercial playbook — contracting strategies (term vs spot, indexed contracts), pricing pass-through mechanisms, and procurement triggers tied to market and raw material inflection points.

- M&A, JV and greenfield prioritization framework — where to place capital in 2026 to capture higher-margin segments or de-risk supply chains through backward integration.

- Case studies and tactical templates — negotiation checklists, due-diligence scorecards, and a phased implementation plan for capacity or product-line changes.

Competitive landscape — strategic takeaways

The market exhibits moderate concentration: the top three players account for roughly the high‑thirties percent of supply, while the top five together control just over half the market. This structure creates a balance between scale-driven pricing power and opportunities for nimble regional or technical specialists to capture premium niches.

- Rain Carbon Inc. — a U.S.-headquartered producer with graphite-electrode-focused binder grades. Recent capacity expansion initiatives in South Asia demonstrate a strategic push to serve growing regional demand and secure lower-cost feedstock access. For buyers, Rain’s scale and global footprint make it a candidate for strategic supply agreements and long-term offtakes.

- Himadri Speciality Chemical Ltd. — India’s dominant domestic producer with deep qualification relationships across major electrode manufacturers. Its export milestone into the Middle East highlights an evolution from domestic leadership to export-oriented strategy. Buyers seeking tight technical fit and approvals may find Himadri an attractive partner, particularly for liquid grades and customized chemistries.

- Koppers Inc., JFE Chemical, Mitsubishi Chemical — established global players whose portfolios span pitches for graphite electrodes and adjacent carbon products. Their strength lies in brand, quality consistency, and integrated carbon chemicals capabilities, making them preferred partners for manufacturers requiring rigorous specification compliance and backward-traceable supply chains.

- Regional specialists (Lone Star Specialties, Konark Tar Products, Shanghai Baosteel Chemical, Jining Carbon Group, DEZA, Dubai Tar Pitch Company, Shree Shyam Chemicals) — these firms frequently compete on localized logistics advantages, tailored grade development and service flexibility. For short‑cycle supply or niche grades, these players can undercut larger suppliers on total landed cost and qualification agility.

Industry dynamics that will shape 2026 decisions

- Raw-material and input cost pressure — coal tar availability and pricing have firmed as aluminum and graphite-electrode demand recover. Procurement strategies in 2026 must include indexed contracts and optionality (alternate feedstocks, tolling) to mitigate price-driven margin erosion.

- Regulatory and compliance cost uplift — tightening control on PAHs and emissions, including obligations under regional industrial emissions rules and national air-quality legislation, requires capital investment in control technologies and changes to process design. Firms that proactively budget and stage compliance investments will reduce operational disruption risk and preserve customer approvals.

- Trade and geopolitics — export licensing and product controls implemented in key producing countries have introduced new frictions in graphite-related supply chains. Buyers should factor in permit-driven lead-time variability and consider multi-sourcing or localized buffer inventories.

- Product quality evolution — growing demand for ultra-high-power (UHP) and impregnation-grade pitches is changing the value capture map. Producers able to demonstrate improved impurity profiles and reproducible rheology command premium pricing and longer-term supply contracts.

Strategic recommendations for 2026 planning

- Align capital allocation with scenario-driven ROI thresholds — prioritize projects that pay back under base and downside scenarios (feedstock shock, slower EAF adoption).

- Secure technical approvals as strategic barriers — investment in R&D and co-development with electrode manufacturers expedites qualification cycles and converts quality into commercial stickiness.

- De-risk feedstock via diversified sourcing — combine long-term supply contracts, tolling agreements, and contingency from regional specialists to limit single-country exposure.

- Quantify and phase compliance investments — map regulatory timelines to capex windows and exploit early-mover technology adoption to achieve lower lifetime compliance costs.

- Reassess commercial models — consider blended pricing mechanisms and inventory finance options that align supplier economics with your margin objectives.

- Use M&A selectively to close capability gaps — bolt-on acquisitions in impregnation-grade or high-purity processing can shorten time-to-market for higher-margin segments.

Why PW Consulting’s report is uniquely actionable for 2026

Beyond headline forecasts, our study translates market dynamics into decision-support artifacts: a live model you can adapt to company-specific assumptions, supplier scorecards keyed to approval status and technical fit, and a stepwise implementation roadmap for procurement, operations and regulatory compliance teams. The analysis highlights where scale matters and where technical differentiation or localization unlocks premium margins.

Next steps

This briefing intentionally omits granular segment-level splits and certain proprietary data points to preserve the consultative value of the full report and to encourage direct engagement for tailored modeling. For procurement leaders, strategic planners and corporate development teams preparing 2026 budgets, our full report provides the complete dataset, model access, and a consultation slot to tailor outputs to your balance sheet and operational realities.

PW Consulting is prepared to support scenario workshops, supplier negotiation playbooks, and due-diligence on potential targets or partnership targets in the coal tar pitch value chain. Contact our industry team to schedule a briefing and obtain the full report and dataset.

For detailed analysis of this topic, please visit the official page:Coal Tar Pitch For Graphite Electrodes Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com