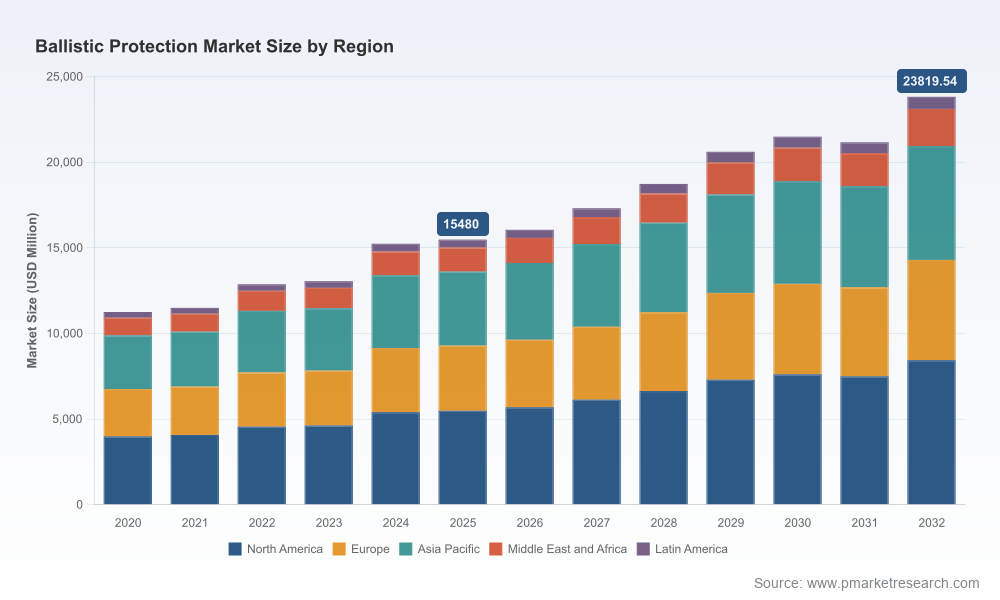

PW Consulting: Ballistic Protection Market Poised for 6.35% CAGR, Surging Through 2032

Other |

2026-07-02 10:53:36

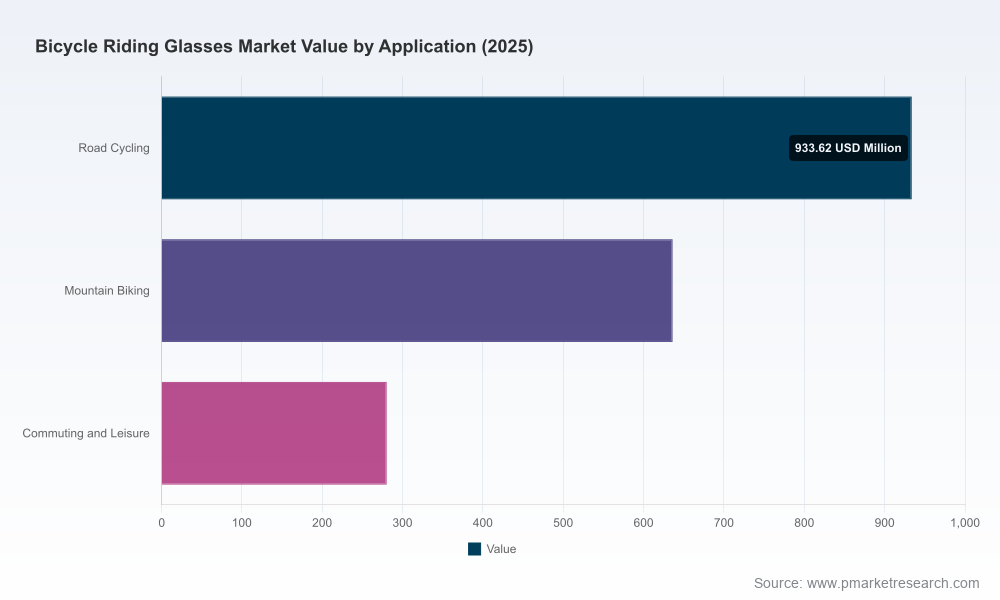

PW Consulting’s latest Bicycle Riding Glasses Market study is designed as a decision-grade briefing for executives who must set product, channel, and portfolio priorities in 2026. The market has demonstrated steady expansion from the start of the decade, growing from roughly USD 1.36 billion in 2020 to about USD 1.85 billion in 2025, and PW’s forecast models—anchored to our base year of 2025—project continued expansion through 2032 at a compound annual growth rate (CAGR) of 6.25%, with the market approaching the low‑to‑mid USD 2.8 billion range by the end of the forecast horizon. This briefing outlines the practical strategic implications we believe should shape boardroom agendas in 2026 while intentionally reserving detailed segment-level tables and exact regional/application splits for subscribers to the full report.

Bicycle Riding Glasses Market

Reliable topline trajectory: With a multi-year historical series and a clear CAGR, the report provides a stable platform for revenue planning, capital allocation, and product roadmap timing for the next three to five years.

Bicycle Riding Glasses Market

Consolidation and competitive leverage: The market shows a modestly concentrated structure (the top three and top five players together represent a defined but not impenetrable share of demand), creating both acquisition opportunities for mid-sized brands and defensive plays for incumbents. (Our executive summary includes concentration metrics to help prioritize targets.)

Bicycle Riding Glasses Market

Regulatory and materials constraints: Mandatory compliance with sport-specific eye-protection standards and the prevailing use of polycarbonate lenses underpin product design, supplier selection, and sourcing risk—factors that materially affect cost curves and time-to-market.

Bottom-up market sizing and scenario forecasts: Detailed annualized models from 2020 through 2032 (base year 2025) with sensitivity cases tied to macroeconomic and participation-rate variables.

Commercial playbooks: Go‑to‑market frameworks for premium, value, and mass segments; channel mixes (direct-to-consumer, specialty cycling retail, mass sports retail, and OEM partnerships) and margin mechanics by route-to-market.

Product and technology benchmarking: Comparative matrices on lens technologies (photochromic, polarized, standard), frame materials, ventilation and anti-fog performance, and integration with helmets and wearables—ranked by performance, cost, and manufacturability.

Supplier & supply‑chain risk maps: Concentration of key lens and frame inputs, lead-time scenarios, and contingency playbooks for polycarbonate sourcing and alternative materials.

Commercial diligence assets: Ready-to-use Excel models, price-elasticity tests, SKU rationalization tools, distribution scorecards, and M&A screening snapshots designed to accelerate decision-making.

Regulatory compliance checklist and test-lab partners: Practical operational requirements to ensure products meet sport safety standards and market access timelines.

The market is structured by lens type, use-case, and geography, and the choices companies make across these vectors materially change unit economics and competitive dynamics. The report qualitatively analyzes demand drivers for photochromic, polarized, and standard lenses and for road, mountain, and urban/commuting use. To preserve the strategic value of our full deliverable—and to provide readers a compelling reason to engage with PW Consulting—we are not publishing the granular regional, application, and type splits in this public summary. Subscribers receive the full tranche of segment tables, growth profiles, SKU-level margins, and retail price ladders.

The competitive field combines global performance brands, technical specialists, and value players. Key observed behaviors and tactical implications include:

Incumbent performance brands (example profiles: Oakley, Smith, Julbo): These firms compete on proprietary lens tech, brand credibility, and premium distribution. Their strengths are product innovation and visibility in specialist retail and athlete endorsements. Strategic implication: new entrants targeting premium niches must demonstrate meaningful differentiation in optics or fit to displace established loyalty.

Technical specialists (example profiles: Rudy Project, Shimano): Companies with engineering DNA leverage interchangeability and aerodynamic fit to win road and elite segments. Strategic implication: partnerships with cycling teams and integration with component ecosystems can accelerate credibility.

Value-focused challengers (example profile: Tifosi): These players win on price-performance and broad distribution. Strategic implication: brands seeking volume should optimize SKU complexity, logistics, and modular designs (interchangeable lenses) to maintain margins at scale.

Cross-category and lifestyle entrants (example profiles: Nike Vision, 100% Eyewear): These firms bring marketing reach and category cross‑sell advantages. Strategic implication: incumbents should assess whether to compete on brand or defense by doubling down on technical IP and athlete validation.

Recent product and market developments underscore these dynamics: in late 2025 and early 2026, independent testing and trade guides called out new-model performance for both premium and value brands—confirming that product quality remains a differentiator across price points. Our competitive chapters provide a granular benchmarking grid, including product positioning maps, channel footprints, and likely M&A targets by valuation band.

Two structural constraints shape near-term opportunities. First, cycling eyewear must satisfy sport protection standards (notably ANSI and ISO sport/eye-protection norms), which affects testing timelines and product claims. Second, polycarbonate continues to dominate as the lens substrate because of a favorable impact-resistance and weight profile versus alternatives. This concentration creates a supply-bottleneck risk and a cost lever for firms that secure long-term contracts or invest in alternative lens-process capabilities. Our report includes an actionable supplier mitigation plan and cost-to-serve scenarios tied to material price shocks.

Prioritize lens R&D that solves for variable light conditions and anti-fog performance—photochromic and hybrid coatings should be evaluated for ROI across product tiers.

Adopt a channel-led SKU strategy: streamline SKUs for online DTC, while offering technical packs for specialty dealers to reduce inventory friction and improve turn rates.

Secure supply continuity through strategic supplier contracts for polycarbonate and explore co-investment into downstream lens finishing to shorten lead times.

Pursue tuck-in deals to acquire distribution footprints or complementary tech rather than headline M&A—our valuation matrix highlights targets likely to move the needle on share with limited capital.

Use third-party testing and athlete endorsements selectively to convert product performance into credible marketing claims that justify premium pricing.

Subscribers to the full report receive the full quantitative backbone needed to operationalize the above moves: detailed regional and application splits, SKU-level margin models, competitor market shares, and acquisition target synopses. The package also includes scenario-ready Excel tools (best/likely/worst cases tied to participation and macro assumptions) and a 12-month GTM playbook tailored to either premium or volume strategies. These are the elements that turn insight into executable plans and measurable KPIs for 2026.

This release is deliberately a strategic preview: it surfaces the most consequential topline, competitive, and operational findings that should influence board-level decisions in 2026 while withholding the granular segment tables and proprietary models that allow for bespoke planning. If your 2026 planning cycle includes product roadmap sign-offs, channel reallocation, supplier negotiations, or M&A screening, the full PW Consulting Bicycle Riding Glasses Market report will provide the calibrated numbers and toolkits you need to act with confidence.

Contact PW Consulting for subscription details and access to the full dataset, scenario models, and the operational playbooks that convert the market’s 6.25% CAGR trajectory into concrete, near-term value creation opportunities.

For detailed analysis of this topic, please visit the official page:Bicycle Riding Glasses Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com