Brake Hoses Market 2026: Strategic Imperatives for Supply-Chain Resilience and Competitive Advantage

As PW Consulting’s lead industry analyst, I present a concise strategic primer drawn from our forthcoming Brake Hoses Market research release. This briefing distils the high-confidence, decision-relevant findings that corporate leaders must factor into 2026 planning cycles — from procurement and product development to M&A screening and regulatory compliance. The goal is to demonstrate the report’s depth and operational value while leaving detailed segment-level outputs reserved for the full study.

Brake Hoses Market

Executive snapshot

The global brake hoses market — measured on a USD revenue basis with 2025 as the base year — has shown steady expansion through the 2020–2025 historical window and continues to project growth across the 2026–2032 forecast horizon at a compounded annual growth rate (CAGR) of approximately 4.12%. Our bottom‑up market model places the 2025 market size in the low‑tens of thousands (USD Million), with a near‑term uplift forecast for 2026 consistent with ongoing vehicle production increases, stricter safety standards, and the rising complexity of braking systems in both passenger and commercial vehicles.

Brake Hoses Market

Why this matters for 2026 planning

- Procurement and cost management: Moderate, consistent market growth at ~4% CAGR means buyers should lock in medium‑term contracts for key inputs (synthetic rubber, PTFE, stainless steel) while keeping flexibility for higher‑performance variants demanded by premium and electric vehicle platforms.

- Regulatory and compliance risk: Mandatory certifications (notably FMVSS 106 and SAE J1401 in major markets) are non‑negotiable for both OEM and aftermarket players. Compliance investments and accredited testing infrastructure must be prioritized in 2026 CapEx plans to avoid market access risk.

- Competitive positioning: The market displays moderate concentration (CR3 ≈ 34.2%; CR5 ≈ 46.85%), indicating room for both scale players and specialized niche suppliers. Strategy work should evaluate whether to compete on scale, service/quality, or technology-led differentiation.

- Aftermarket vs OEM strategies: Aftermarket channels remain structurally important; however, securing Tier‑1 or OEM design wins yields higher revenue visibility and long‑lifecycle contracts. Firms must align product portfolios and certification readiness with targeted channel strategies in 2026.

Report contents: practical, transaction‑ready intelligence

The full PW Consulting report is structured for immediate board‑level and operational use. Key deliverables include:

Brake Hoses Market

- Proprietary market sizing and forecast model (historical 2020–2025, forecast 2026–2032) with scenario analysis for demand shocks and regulatory tightening.

- Supply‑chain heat maps identifying single‑source risks, raw‑material exposure (synthetic rubber, stainless alloys, PTFE) and logistics choke points.

- Compliance playbook covering FMVSS 106, SAE J1401 and major regional homologation requirements, with an implementation checklist for manufacturers and assemblers.

- Commercial due diligence templates for M&A and JV evaluation: CAPEX needs, margin drivers, warranty / liability exposure, and integration risk matrices.

- Product and manufacturing benchmarking: material choices, testing protocols, automation pathways, and quality management KPIs tied to cost and reliability outcomes.

- Go‑to‑market playbooks: OEM tendering strategies, aftermarket distribution architectures, pricing levers, and service‑based differentiation (e.g., lifecycle maintenance, predictive diagnostics).

- Technology watch: material innovations, PTFE and stainless steel adoption patterns in high‑performance segments, and testing regimes that exceed baseline standards.

Competitive landscape: implications and tactics

Our competitive analysis covers global OEM suppliers, specialist niche manufacturers and vertically integrated players. While the market is neither monopolistic nor fully fragmented, leaders combine certification strength, geographic footprint, and deep OEM relationships. Representative strategic profiles and associated implications:

- Large diversified suppliers (examples: global fluid‑power players): Benefit from scale, cross‑portfolio customer relationships, and broad aftermarket distribution. Recommendation: leverage cross‑selling into adjacent hydraulic lines, invest in global testing capabilities, and optimize pricing via procurement economies.

- Specialist hose manufacturers (examples: regionally dominant independents): Offer high technical know‑how and customization for OEMs, with premium pricing in high‑performance niches. Recommendation: defend differentiation through certification leadership, targeted R&D, and selective capacity expansion near key OEM sites.

- Emerging vertically integrated and low‑cost producers: Can secure aftermarket share rapidly but face certification and reputational hurdles. Recommendation: incumbents should accelerate quality and certification investments to create meaningful entry barriers.

The report profiles leading firms across these archetypes, evaluating manufacturing footprints, certification records, product portfolios, and go‑to‑market models. We map where strategic consolidation, partnerships, or selective greenfield investment will produce outsized returns.

Regulation and testing: a gating factor

Compliance with FMVSS 106 and SAE J1401 remains central to market access in several major regions. Our analysis emphasizes three practical implications for 2026:

- Certification is both an entry requirement and a competitive moat — firms without documented testing and DOT registration face immediate exclusion from significant aftermarket channels.

- Testing protocols (expansion, burst, environmental aging) are increasingly conservative relative to past practice; leading suppliers now incorporate accelerated life testing and chemical/thermal resistance validation as standard R&D elements.

- Procurement contracts should explicitly allocate compliance‑related liabilities and warranty obligations; due diligence must include lab audit results and re‑testing commitments in seller representations.

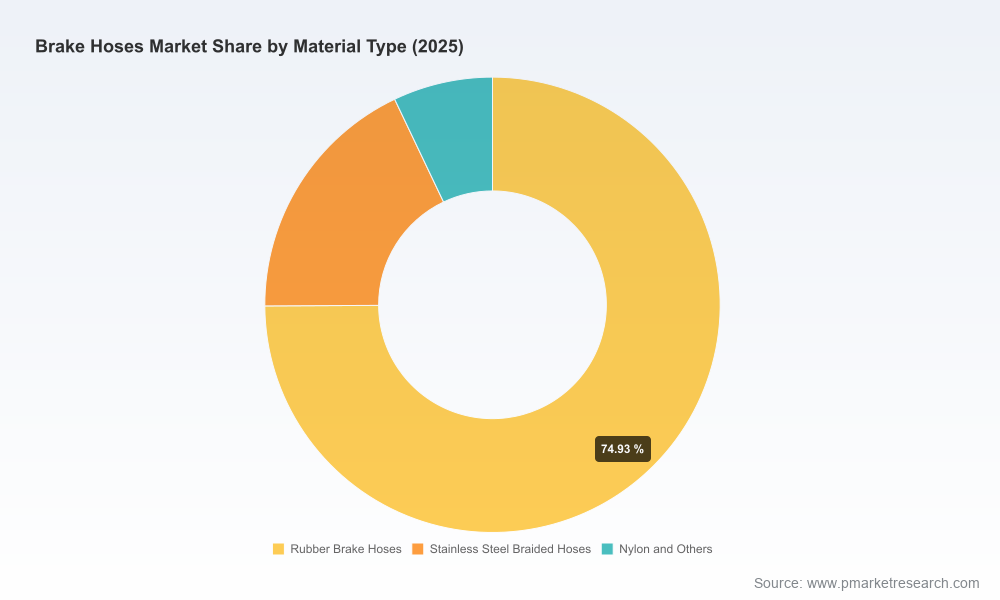

Materials and technology trends — strategic bets for 2026

Synthetic rubber continues as the base material for the majority of applications due to cost and flexibility. Simultaneously, stainless steel braided assemblies and PTFE‑lined hoses are gaining traction in performance segments and in environments demanding corrosion resistance. For strategy teams this translates into two clear actions:

- Maintain cost‑effective synthetic rubber supply agreements for volume platforms while selectively expanding capabilities in stainless/PTFE for premium and electric vehicle platforms.

- Invest in testing and quality control capacity aimed at higher‑value product lines where margins justify capital and certification spend.

Recent market movements to watch

- Trade show and technology forums continue to shape OEM and supplier roadmaps — industry exhibitions in late‑2025 highlighted braking technology innovation and aftermarket services.

- Product introductions in late‑2025 expanded supplier ranges with pressure‑tested coil and unbent hoses targeting rapid-fit aftermarket demand.

- Certification lists updated in early 2026 underscore the near‑term regulatory housekeeping that aftermarket suppliers must complete to retain DOT‑compliant status.

Actionable recommendations for 2026 corporate planning

Based on our market model and scenario runs, executives should treat 2026 as a pivot year to tighten compliance, shore up supply chains, and selectively invest in product and manufacturing capabilities. Key, prioritized moves:

- Implement a two‑track procurement approach: secure long‑term supply for base materials and maintain optionality (spot or supplier flex clauses) for higher‑performance alloys and PTFE.

- Prioritize certification readiness and third‑party lab audits as a gating item for any go‑to‑market or M&A activity in 2026.

- Target OEM partnerships for new electrified platforms where brake system behavior is evolving; early design wins confer long revenue tails.

- Quantify and mitigate single‑source and logistic bottlenecks using a supplier concentration scorecard built from our report’s supply‑chain heat maps.

- Screen M&A targets using an integration score that weights certification, manufacturing automation, and customer contracts more heavily than short‑term revenue multiples.

- Elevate aftermarket warranties and service propositions (e.g., bundled replacement programs, predictive diagnostics) to differentiate from low‑cost competitors.

Conclusion — the strategic payoff

Our analysis shows a market with reliable, mid‑single‑digit growth and meaningful strategic inflection points driven by regulation, material substitution, and OEM platform evolution. The decisions you take in 2026 — on procurement, certification, and selective capability investment — will materially affect your competitive positioning across the decade. PW Consulting’s full Brake Hoses Market report delivers the granular segment intelligence, supplier evaluations, and playbooks required to convert that insight into actionable decisions.

Next steps

For executive teams preparing 2026 budgets and M&A pipelines, the full report contains the granular segmentation, regional scenarios, and supplier scorecards that we intentionally omit here to preserve the “trailer” focus of this briefing. Contact our research desk to access the complete dataset, model files, and practitioner checklists that will enable immediate implementation.

For detailed analysis of this topic, please visit the official page:Brake Hoses Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com