Why CPA Bookkeeping Services Are a Critical Year-End Advantage for U.S. SMEs in the BFSI Industry

Other |

2026-07-08 08:09:47

As PW Consulting publishes its 22 Dimethylbutyric Acid Market report (base year 2025; historical coverage 2020–2025; forecast horizon 2026–2032), this brief highlights the strategic value of the study for executive teams planning allocations, M&A, supply‑chain adjustments and product development strategies in 2026. The analysis synthesizes macro sizing, concentration dynamics, supply‑side realities and regulatory inflection points — enough to inform boardroom debate while reserving the granular segment tables and proprietary scenarios for the full report.

22 Dimethylbutyric Acid Market

Steady, predictable growth: Our market model (revenues reported in USD Million) shows a consistent expansion from the historical period into the forecast window, with an underlying compound annual growth rate (CAGR) of 4.82% across 2026–2032. That pace creates a planning horizon conducive to medium‑term capacity investments, multi‑year supplier contracts and targeted product development roadmaps rather than speculative short‑term plays.

22 Dimethylbutyric Acid Market

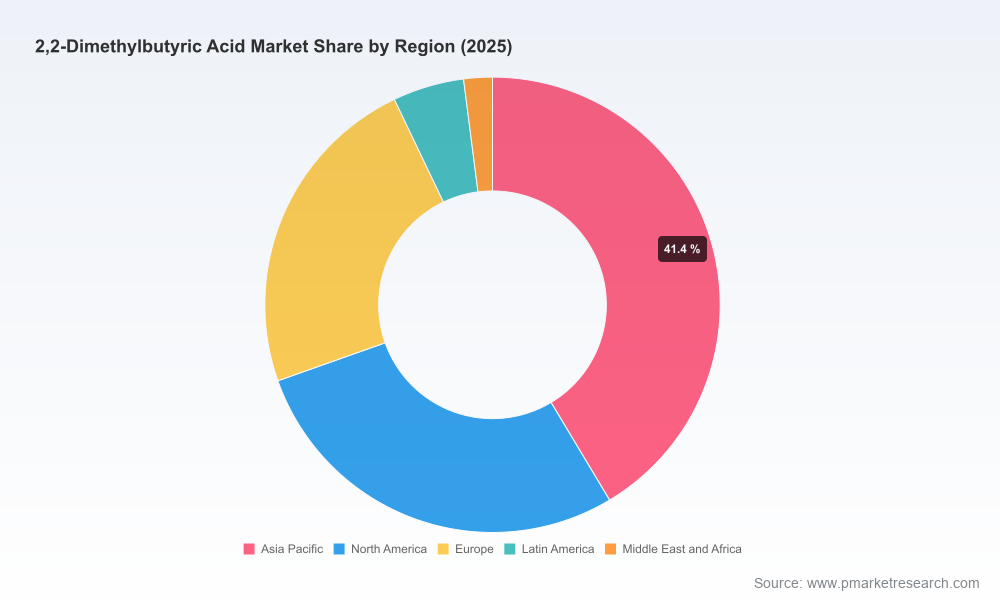

Consolidation opportunities: The market exhibits a measurable degree of concentration (CR3 ~56% and CR5 ~72%), indicating that top suppliers command a material share of demand. For potential entrants and smaller producers, this structure implies both competitive barriers and carve‑out opportunities through niche specialization or backward integration.

22 Dimethylbutyric Acid Market

Cross‑sector exposure: Demand is tied to pharmaceutical intermediates, agrochemicals and specialty applications. This cross‑sector positioning reduces correlation with any single end‑market cycle but increases sensitivity to regulation, raw‑material availability and quality specifications that differ by end use.

Trajectory snapshot: The market expanded from an estimated USD 30.45 Million in 2020 to USD 38.5 Million in 2025 (base year). Our projection anticipates steady growth into the late 2020s and early 2030s, reaching approximately USD 53.5 Million by 2032 under the central scenario. This shows a clear, non‑volatile growth path suitable for capital projects with multi‑year payback profiles.

Implication for capital allocation: At a sub‑5% CAGR, firms should prioritize high‑return, low‑execution‑risk investments — for example, process optimization to raise yields or modular capacity expansions — rather than large greenfield plants that require long lead times to monetize.

Production routes and process economics: Recent patent literature identifies multiple scalable synthesis pathways (e.g., carbonylation routes from isoamyl alcohol with formic acid under acid catalysis; Grignard‑type additions to CO2; nitrile‑hydrolysis routes from chlorinated precursors). These alternatives differ in feedstock intensity, unit‑operation complexity and achievable purity. For producers and CPOs, process choice will drive raw‑material exposure, environmental compliance costs and product cost curves.

Regulatory and trade factors: The compound’s trade classification and associated duties can materially affect landed cost in import‑dependent supply chains. Recent customs entries show specific tariff regimes and supervision requirements that buyers and exporters must incorporate into total landed cost models and sourcing decisions.

Quality and specification segmentation: End‑users, especially in pharma and fine chemicals, demand high‑purity grades and consistent batch documentation (e.g., certificates of analysis, SDS compliance). Suppliers that can reliably deliver regulatory documentation and traceability will command premium access to higher‑margin channels.

Logistics and packaging economics: Given the product’s common handling in drums and intermediate volumes for R&D and pilot production, flexibility in pack sizes and logistics partners remains a differentiator. Smaller suppliers can defend margins via service‑led differentiation where volume plays are limited.

The full report provides an operationally focused segmentation by product type (purity tiers), application (end‑use verticals) and geography, with demand forecasts and directional pricing differentials. In this brief we intentionally summarize rather than disclose segment‑level shares to preserve the report’s role as a subscription asset.

Practical takeaway: Decision makers should treat purity and regulatory documentation as primary drivers of customer access and margin differentiation, while geography and logistics determine cost competitiveness and time‑to‑market.

TNJ Chemical (China) — URL: https://www.tnjchem.com. TNJ positions itself as a producer‑supplier for synthesis intermediates with established commercial pack sizes and third‑party certification. Strategic implication: buyers seeking consistent production scale and cost competitiveness should evaluate TNJ’s qualification credentials and supplier redundancy plans.

OTTO KEMI (India) — URL: https://www.ottokemi.com. An India‑based manufacturer and exporter that emphasizes research‑grade product availability for global shipping. Strategic implication: OTTO KEMI is well suited for customers needing flexible, research‑scale supply and rapid access to specialty grades.

Central Drug House (CDH) Fine Chemicals (New Delhi, India) — URL: https://www.cdhfinechemical.com. ISO‑certified supplier focused on analytical and reagent‑grade packings for laboratory and small‑scale production. Strategic implication: CDH can be a preferred partner for formulators and R&D organizations prioritizing documentation and small‑lot logistics.

Tokyo Chemical Industry Co., Ltd. (TCI) (Japan) — URL: https://www.tcichemicals.com. TCI supplies laboratory‑grade building blocks with detailed specifications and safety documentation. Strategic implication: TCI’s global distribution and brand trust make it attractive for regulated R&D and early‑stage development work where traceability is paramount.

Shijiazhuang Dowell Chemical Co., Ltd. (China). A fine‑chemical manufacturer with stated annual capacity for related dimethylbutyric acids and derivatives (including acyl chlorides), and existing export relationships across Europe, the USA, India and Korea. Strategic implication: Dowell’s capacity focus positions it for larger volume contracts and potential vertical integration plays for pesticide and pharmaceutical intermediates.

Market structure note: The concentration metrics noted earlier suggest a market where a few suppliers have scale advantages, but specialized niches and high‑purity segments remain accessible to smaller or regionally focused providers. Competitive moves in 2026 should therefore balance scale with specialization.

Buyers: institute dual‑sourcing contracts that differentiate between purity tiers and regulatory documentation needs. Use the forecasted, modest CAGR to prioritize contractual flexibility (e.g., volume bands, roll‑over options) over rigid long‑term minimums.

Producers: target margin expansion through yield improvement, impurity control and certified documentation. Consider modular capacity expansions or tolling partnerships rather than large greenfield investments unless long‑term offtake can be secured.

Investors/M&A: evaluate bolt‑on acquisitions that add either high‑purity capabilities or downstream conversion (e.g., acyl chloride derivatives) to capture more value per unit of feedstock. CR3/CR5 metrics indicate M&A can meaningfully shift market shares if integration is executed quickly.

R&D and product development: prioritize formulations that tolerate lower‑grade feedstock where feasible, reducing exposure to premium high‑purity raw material costs; conversely, develop proprietary processes where purity commands sustainable pricing premiums.

Supply‑chain managers: incorporate tariff and supervision costs into landed‑cost models and review logistics pathways for import‑intensive flows, including inspection timelines that can affect lead times and safety stock requirements.

Detailed market model (USD Million, historical 2020–2025, forecast 2026–2032) with scenario runs and sensitivity to feedstock price, duty changes and capacity additions.

Actionable supplier due‑diligence templates, procurement scorecards and a validated list of global producers with capability matrices and contact points.

Segment‑specific playbooks (purity tiers × end‑use) that map margin pools, qualification requirements and go‑to‑market strategies for 2026‑2028.

Regulatory and trade annex covering HS classification implications, common country tariff treatments, and recommended customs‑compliant document flows for import/export operations.

Process economics primer summarizing alternative synthesis routes, their feedstock sensitivities, CAPEX ranges and likely environmental & permitting considerations.

Our estimates combine bottom‑up supplier capacity/build‑out analysis, demand mapping by end use, and price/distributor margin triangulation. Data sources include primary supplier disclosures, patent filings, customs and trade databases, and PW Consulting’s proprietary survey of procurement leads in the pharmaceutical and agrochemical sectors.

Base year and forecasting conventions: base year 2025; historical window 2020–2025; forecast period 2026–2032. Revenue figures are reported in USD Million and scenarios are stress‑tested for ±20% raw material cost shocks and tariff adjustments.

For firms making 2026 capital and sourcing decisions, the 2,2‑Dimethylbutyric Acid market presents a low‑volatility growth environment where well‑timed operational improvements, supplier qualification rigor and selective collaboration (tolling, off‑take or acquisition) can yield durable advantage. The full PW Consulting report provides the operational templates, supplier maps and scenario models to move from strategic intent to executable plans. For access to the complete datasets, segment tables and supplier scorecards, visit PW Consulting’s market report page to request the full study and supporting appendices.

For detailed analysis of this topic, please visit the official page:22 Dimethylbutyric Acid Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com