Don’t Paint Your Walls Before Reading This!

Other |

2026-05-06 07:52:25

PW Consulting’s Preeclampsia Therapeutic Market report (base year 2025; historical review 2020–2025; forecast 2026–2032) delivers a focused, strategy‑ready view of a market transitioning from supportive care to targeted disease‑modifying approaches. Our top‑level sizing shows a resilient market growing at a compound annual growth rate (CAGR) of 4.88% through the forecast window. The market is forecast to expand from its 2025 baseline into a materially larger opportunity by 2032, driven by late‑stage clinical programs, diagnostic adoption, and evolving reimbursement dynamics.

Preeclampsia Therapeutic Market

Timing and prioritization: Several first‑in‑class and novel modality candidates (recombinant proteins, siRNA, AI‑discovered small molecules, targeted apheresis) are advancing through clinical development. For biopharma and investors, 2026 is a pivotal year to commit resources to programs that can move from proof‑of‑concept into registrational paths.

Preeclampsia Therapeutic Market

Regulatory clarity and catalyst sequencing: Regulatory interactions and regional trial authorizations in late 2025–2026 alter development timelines and go‑to‑market sequencing. Companies that align non‑clinical packages and early regulator engagement will shorten commercial lead times.

Preeclampsia Therapeutic Market

Commercial planning: Even with modest baseline growth, the combination of improved diagnostics, new therapeutics, and concentrated clinical uptake implies asymmetric returns for first movers who secure payer pathways and provider adoption before competitors scale manufacturing.

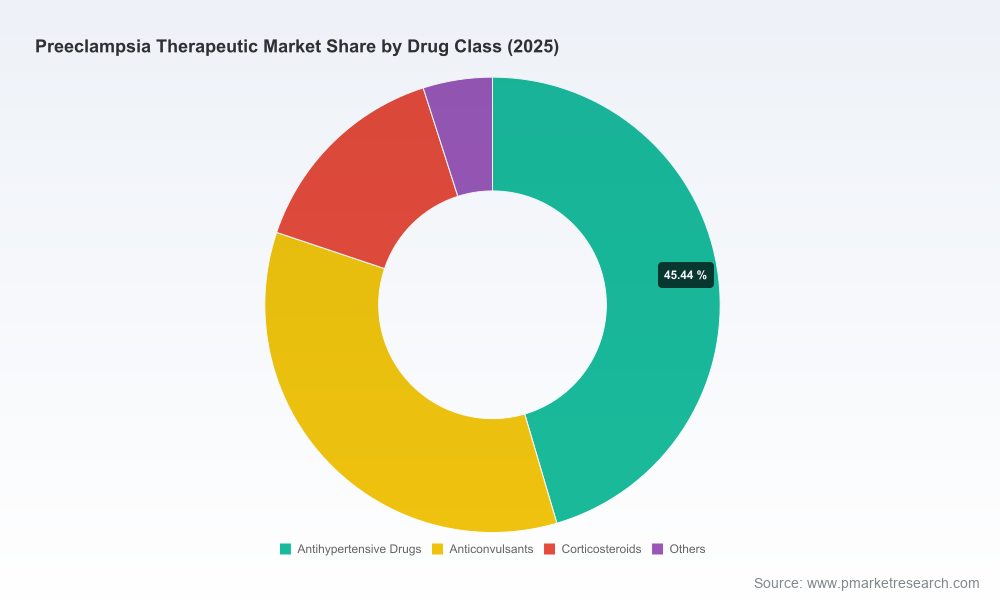

Transitioning standard of care: Current management remains anchored in repurposed antihypertensives (e.g., labetalol, nifedipine, hydralazine), magnesium sulfate for seizure prophylaxis, and preventative low‑dose aspirin for high‑risk patients. No FDA‑approved disease‑modifying therapeutic existed as of early 2026, making the regulatory and clinical landscape particularly consequential.

Diagnostics as accelerants: Expanded availability of validated sFlt‑1/PlGF ratio testing and other risk stratification tools is reducing clinical uncertainty, enabling earlier therapeutic intervention and potentially improving trial recruitment and endpoint definition.

Supply‑side fragility: Persistent supply chain weaknesses in low‑ and middle‑income settings create both humanitarian challenges and commercial opportunities—particularly for companies able to demonstrate robust, cost‑effective manufacturing and distribution models.

Addressable market trajectory: From our 2025 baseline to 2032, the market expands meaningfully under a baseline scenario (CAGR ~4.88%). Scenario modeling included conservative, central, and accelerated uptake pathways tied to clinical readouts and reimbursement decisions.

Product modality differentiation matters: Therapeutic mechanisms that directly target sFlt‑1 biology, restore placental angiogenic balance, or modulate maternal vascular function stand to command premium positioning. Delivery format, safety in pregnancy, and ease of integration into existing obstetric care pathways will determine adoption velocity.

Concentration and partnership dynamics: The competitive environment is neither atomized nor monopolistic. There is space for innovative mid‑cap companies to scale through partnerships with established players that offer distribution, regulatory, or manufacturing muscle.

Access and equity tradeoffs: Commercial strategies that ignore supply, pricing, and local regulatory contexts—especially in emerging markets—risk low uptake and reputational downside. Conversely, tiered pricing and novel delivery partnerships can unlock high‑volume segments and CSR value.

DiaMedica Therapeutics (Minneapolis, MN; https://www.diamedica.com) — Advancing DM199 (rinvecalinase alfa), a recombinant tissue kallikrein‑1 candidate for early‑onset preeclampsia. Notable regulatory progress includes productive pre‑IND FDA interactions in late 2025 and Health Canada Phase 2 clearance in early 2026. These interactions position DiaMedica as a near‑term clinical catalyst and a potential partner or acquisition target for larger players seeking a biologic candidate in pregnancy‑safe modalities.

Comanche Biopharma — Developing CBP‑4888, an siRNA‑based approach targeting sFLT1 isoforms. RNAi modalities present differentiation on mechanism and manufacturing complexity; partnerships with established oligonucleotide CDMOs and focused safety packages will be critical.

Gmax Biopharm (China/USA) — Progressing GMA‑312 or related candidates in the pipeline. Dual‑jurisdiction operations imply both rapid recruitment potential and regional regulatory complexity.

Vicore Pharma (Sweden) — Pursuing mechanism‑focused therapies aimed at underlying pathophysiology. European regulatory engagement and smaller‑scale biomarker‑driven trials can yield rapid proof points.

Kyowa Kirin (Tokyo; https://www.kyowakirin.com) — Leveraging established R&D and commercialization infrastructure to explore candidates (e.g., KW‑3357) with potential global reach—especially if safety and maternal‑fetal outcomes are favorable.

Evergreen Therapeutics — AI‑enabled small‑molecule discovery (EG‑101) offers a faster and potentially lower‑cost path to oral therapeutics, but will require robust teratogenicity and reproductive safety data.

MirZyme Therapeutics (UK) — Focused on MZe786 for prevention strategies. Preventive assets alter payer calculus and population health implications compared with acute therapeutics.

Advanced Prenatal Therapeutics (USA; https://www.advancedprenatal.com) — Developing targeted apheresis technology designed to remove pathogenic factors in preeclampsia. Device‑based interventions change commercialization models and hospital adoption dynamics.

Aggamin LLC — Developing recombinant human PlGF protein candidates targeting sFlt‑1 biology; biologic approaches will face manufacturing and cold‑chain considerations but could deliver differentiated efficacy.

Late 2025–early 2026 regulatory and clinical milestones (e.g., DiaMedica’s FDA pre‑IND engagement and Health Canada Phase 2 clearance) materially de‑risk certain development paths and sharpen timelines for readouts that matter to commercial planning.

Diagnostics approvals and rollouts (for example, regulatory expansion of validated sFlt‑1/PlGF ratio testing) are lowering clinical uncertainty, supporting more precise trial designs and improving clinical uptake forecasting.

Academic and philanthropic trials (e.g., MitoQ vascular function studies supported by grant funding) highlight non‑proprietary approaches that could complement or compete with commercial therapeutics in certain markets.

Regulatory baseline: magnesium sulfate remains WHO‑recognized as the safest, most effective, and lowest‑cost medicine for severe preeclampsia/eclampsia, underscoring that any new therapeutic must demonstrate clear clinical advantage and cost‑effectiveness to displace entrenched standard‑of‑care practices.

Accelerate regulated evidence generation: Prioritize non‑clinical and early clinical packages that address pregnancy‑specific safety signals. Early, iterative regulator interactions reduce downstream risks and accelerate trial approval timelines.

Design diagnostics‑linked development: Co‑develop or partner on companion diagnostics and risk stratification tools to improve trial efficiency, label precision, and payer arguments.

Secure manufacturing and supply resilience: For biologics, oligonucleotides, and specialty small molecules, lock in capacity and redundancy early. For supportive therapeutics and repurposed drugs, plan for procurement innovations to mitigate stock‑out risks in emerging markets.

Payer engagement and health economics early: Develop robust value dossiers capturing maternal and neonatal outcomes, hospitalization reductions, and potential downstream cost offsets. Preventive and disease‑modifying claims will be judged on both clinical and economic impact.

Partnership and M&A scouting: Identify complementary assets—diagnostics, manufacturing, geographic reach—and consider staged alliances that preserve optionality while accelerating market entry.

Market access segmentation: Prepare differentiated launch plans tailored to hospital systems, obstetrics networks, and national maternal health programs; address access pathways in low‑ and middle‑income countries through tiered pricing and public‑private collaborations.

Proprietary market sizing model with scenario analysis across conservative, central, and accelerated uptake pathways for 2026–2032.

Clinical pipeline and translational risk matrix mapping mechanism, modality, development stage, and regulatory/readout timelines.

Commercial readiness checklists tailored to therapeutics, diagnostics, and device candidates—covering manufacturing, regulatory, payer, and provider adoption readiness.

Go‑to‑market frameworks including pricing and reimbursement playbooks, hospital contracting guides, and distribution channel strategies.

Strategic M&A and partnership heatmaps identifying targets by capability gaps and timing windows.

Country‑level access considerations and risk registers that prioritize actions for high‑impact markets while preserving global launch optionality.

This preview is intended to inform boardrooms, business development teams, and R&D strategy groups as they finalize 2026 budgets and go‑to‑market sequencing. The full PW Consulting report contains the underlying datasets, scenario model inputs, and granular segmentation required to operationalize these strategic recommendations.

For teams preparing investments, alliances, or launch plans in preeclampsia therapeutics, PW Consulting’s full report provides the definitive, actionable intelligence required to make high‑confidence decisions in 2026. Visit PW Consulting’s report portal to request the complete dataset, model access, and advisory engagement options.

For detailed analysis of this topic, please visit the official page:Preeclampsia Therapeutic Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com