Future Trends in the Maple Syrup Industry Toward 2034

Food |

2026-05-22 11:28:46

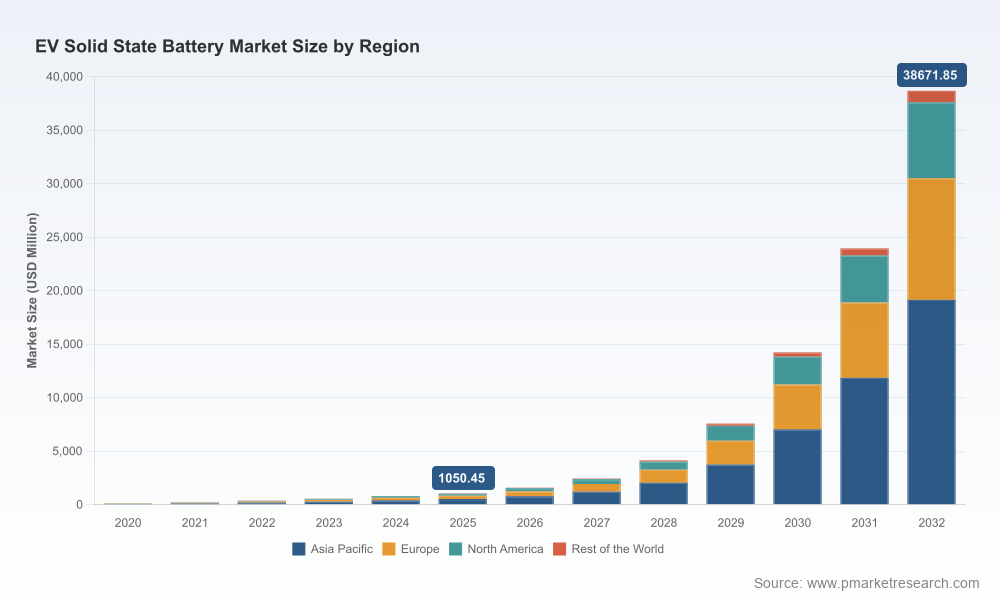

PW Consulting’s new Ev Solid State Battery Market report (base year 2025; forecast 2026–2032) is the practitioner’s playbook for executive decision-making in a market transitioning from laboratory promise to automotive-scale deployment. Our model shows the market expanding from roughly USD 1.05 billion in 2025 to an order-of-magnitude larger industry by the end of the forecast window — reflecting a 67.35% CAGR — with near-term inflection points already visible in 2026. This release distills macro momentum, technology inflection trajectories, competitive positioning and actionable operational guidance that senior leaders must use to shape investment, product and commercial strategies in 2026.

Ev Solid State Battery Market

Timing for capital allocation: Solid-state cells are moving from prototype validation to pilot and early production. Our report quantifies the implied capital intensity and breakeven horizons for different commercialization pathways, enabling CFOs and corporate development teams to sequence investments and financing rounds for 2026 board cycles.

Ev Solid State Battery Market

Technology selection under uncertainty: With multiple electrolyte chemistries and cell architectures advancing in parallel, product leaders need a risk-weighted framework to prioritize roadmap bets. We provide tech-readiness scoring, coupled with sensitivity analyses that show how small shifts in material or process cost assumptions change ROI and vehicle-level metrics.

Ev Solid State Battery Market

Supply chain resilience: The market dynamics show rapid growth beginning in 2026; procurement teams must lock in critical inputs, validate upstream capacity and hedge exposure to volatile components. Our supplier-mapping and contract negotiation playbooks are designed specifically for 2026 sourcing cycles.

Regulatory and incentive capture: Policy instruments (domestic production credits and evolving EU battery regulations) materially change the economics and must be integrated into 2026 investment decisions. The report includes scenario tax-impact models and compliance checklists for near-term programs.

Robust market sizing and forecasting: Annual market and unit forecasts across 2026–2032 with a transparent modelling methodology, sensitivity bounds and scenario narratives to stress-test strategic plans.

Technology deep dives: Comparative analysis of electrolyte families, anode concepts and cell formats, including maturity curves, manufacturability risk, and a “time-to-first-mass-production” mapping to inform product roadmaps.

Capital & cost engineering: End-to-end cost curves from raw materials to cell assembly, plus capex templates and a build-versus-buy decision matrix for gigafactory investments.

Supply chain maps and supplier readiness: Tiered supplier profiles, qualification pathways, and a supplier-de-risking scorecard tailored to solid-state specifics (e.g., foil handling, ceramic tooling, sulfide handling protocols).

Regulatory and incentives playbook: Practical guidance to align product specs with near-term regulatory regimes and to claim available production tax credits and incentives in major markets.

Commercial go-to-market and partnership templates: Negotiation strategies, JV models, licensing structures and integration checklists for OEMs, tier-1s and cell manufacturers.

Competitive intelligence & M&A screening: Actionable profiles and deal playbooks for engaging incumbents, new entrants and specialized IP owners — including an M&A heatmap that flags attractive targets by capability and geography.

The market’s macro trajectory is stark: a small but rapidly accelerating base in 2025 expands several-fold through the forecast period. This creates a window in 2026 where strategic moves—such as locking in supply agreements, initiating pilot production, or securing targeted incentives—can alter competitive positioning for the better. With a measured CAGR of 67.35% embedded in our central forecast, companies that treat 2026 as the year to operationalize deliberate, data-driven initiatives will capture disproportionate early scale benefits.

Market concentration is meaningful but not monopolistic: the top three firms account for a material fraction of the market, with the top five controlling a clear majority — indicating both the presence of powerful incumbents and a runway for specialist entrants and regional champions.

Toyota Motor Corporation (Japan) — Pursuing commercial deployment with prototypes that target long range and rapid charging; near-term commercialization plans in the late 2020s make Toyota a pivotal integrator for scaled automotive usage. (https://global.toyota/en/)

Samsung SDI (South Korea) — Demonstrating high volumetric energy densities in prototypes and deep OEM partnerships; positioned to translate cell-level energy density into vehicle-level differentiation. (https://www.samsungsdi.com/)

LG Energy Solution (South Korea) — Advancing sulfide-based chemistries with pilot production lines; strong manufacturing heritage could accelerate scale advantages if material challenges are resolved. (https://www.lgensol.com/en/index)

CATL (China) — Leveraging production scale and engineering resources to condense solid-state pathways into mass-producible forms; a key player for supply continuity in high-volume markets. (https://www.catl.com/en/)

QuantumScape (USA) — Focused on anode-free lithium-metal architectures with validated prototypes and automotive partner sampling — a technology-driven entrant to watch in partnership and licensing contexts. (https://www.quantumscape.com/)

Solid Power (USA) — Moving into EV cell production with sulfide electrolyte approaches and partnerships that validate automotive readiness. (https://www.solidpowerbattery.com/)

ProLogium (Taiwan) — Ceramic-based approach with operational gigafactory capacity and prototype supply to OEMs; a notable regional scale player. (https://www.prologium.com/en/)

Blue Solutions (France) — Polymer-based commercial deployments in niche vehicle fleets; demonstrates near-term commercial pathways that emphasize reliability over absolute energy density. (https://www.blue-solutions.com/)

Murata Manufacturing (Japan) — Translating miniaturized cell experience into scaled formats for automotive needs; watch for IP cross-licensing and scaling partnerships. (https://www.murata.com/)

Toshiba Corporation (Japan) — Emphasizing safety and longevity with SCiB variants; a conservative yet strategically significant participant for energy storage and EV niches. (https://www.global.toshiba/)

Raw materials: Lithium-metal inputs are stabilizing after early volatility; market averages have moved into a narrower range, but supply tightness for specific foil forms may create localized spikes. Procurement teams must include lead-time buffers and qualified secondary sources.

Electrolyte and component costs: Bulk prices for certain solid electrolytes remain a meaningful share of cell cost. Cost declines will be driven by process scale and material substitutions; our cost-engineering models identify where process innovation has the highest leverage.

Regulatory thresholds: Evolving regulation in major jurisdictions is shifting the minimum performance and recyclability bar. Manufacturers that integrate compliance into early design cycles reduce retrofit costs and accelerate market access.

Incentives and local production economics: Country-level production incentives materially affect location choices. Where available, production tax credits change the NPV calculus for greenfield gigafactories and should be modelled into site selection in 2026.

Standards and safety assurance: Existing ISO standards provide a framework for performance testing; establishing robust quality systems and third-party validation in 2026 will shorten OEM qualification timelines.

Run a condensed “first-mover readiness” assessment: Use our two-week diagnostic to identify capability gaps across materials sourcing, process controls and OEM integration requirements; prioritize quick wins that accelerate qualification timelines.

Lock strategic supply and offtake agreements with staged pricing and flexibility clauses to balance exposure to raw-material volatility and technology evolution.

Design modular pilot lines: Build pilot capacity that can be repurposed across chemistries and cell formats to reduce stranded asset risk while preserving the option to scale rapidly.

Embed regulatory and incentive capture into financial models: Model scenarios that include production tax credits and compliance costs to understand net returns across potential plant locations.

Prioritize collaborations over outright ownership in near-term: JV and co-development models de-risk scale-up while preserving technology optionality.

Institutionalize technical and commercial monitoring: Set up a 90-day intelligence cadence (materials pricing, prototype performance, OEM qualification progress, policy changes) to keep executive decisions evidence-based.

For 2026 planning cycles, use the report to (a) stress-test capital plans against a high-growth baseline, (b) validate technology roadmaps through our readiness scoring, and (c) structure supply agreements using the negotiation templates and cost-sensitivity outputs. The report is intentionally operational: alongside strategic narratives you will receive executable templates, supplier scorecards and investment playbooks that can be deployed immediately.

This press release highlights the analysis depth and practical utility embedded in PW Consulting’s Ev Solid State Battery Market report. Detailed segment-level tables, full regional and application splits, proprietary company valuations and model inputs are reserved for the full report to ensure clients derive exclusive, decision-ready insights. To access the full dataset, modelling workbooks and bespoke advisory services for 2026 execution, visit PW Consulting’s market report page or contact our advisory desk for a briefing and tailored 90-day action plan.

For detailed analysis of this topic, please visit the official page:Ev Solid State Battery Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com