Artificial Intelligence (AI) Chipset Market: Size, Share, and Future Growth

Other |

2026-05-26 04:47:58

As electrical-safety priorities tighten across new construction, retrofit programs, and smart-home rollouts, the Arc Fault Circuit Interrupters (AFCI) market is entering a phase of sustained expansion. PW Consulting’s latest market study, anchored on a 2025 base year and projecting through 2032, benchmarks the global AFCI market’s trajectory and delivers the practical inputs executives need to convert regulatory momentum and technological innovation into profitable product, supply-chain, and go-to-market strategies.

Arc Fault Circuit Interrupters Market

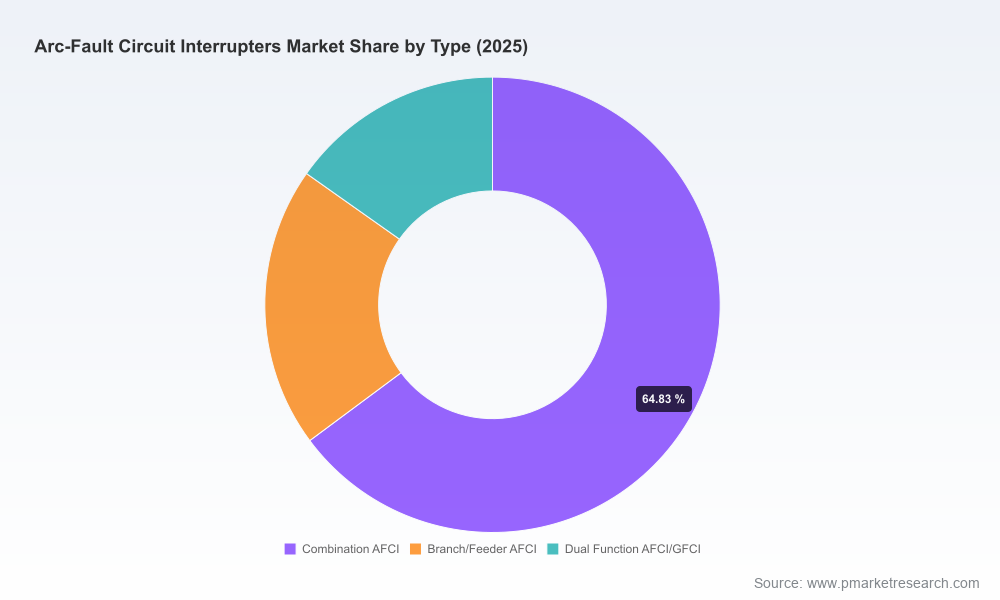

At a compound annual growth rate (CAGR) of 6.3% over the forecast horizon, the market shows durable, mid-single-digit growth underpinned by code adoption, device evolution, and increasing retrofit activity. Market concentration is meaningful—three leading suppliers control a substantial majority of the market and the top five firms command over three quarters—creating both stability and strategic entry barriers for challengers.

Arc Fault Circuit Interrupters Market

Actionable forecasting for capital allocation: The report converts high-level growth into decision-ready scenarios—optimizing R&D investments, manufacturing scale-up timing, and channel expansion plans for 2026 budget cycles.

Arc Fault Circuit Interrupters Market

Risk-to-reward mapping for supply chains: We quantify exposure to raw-material swings and propose hedging and dual-sourcing blueprints tied to component-intensity profiles for AFCI devices.

Regulatory playbook: The work synthesizes NEC adoption trends and certification requirements into checklists and launch-gate criteria so product teams can accelerate compliant rollouts without losing margin discipline.

Competitive positioning framework: The report translates market concentration and vendor capability matrices into defensible white-space and partnership opportunities for incumbents and new entrants alike.

PW Consulting’s modeling shows a steadily expanding overall market from the 2025 base into 2032 under a 6.3% CAGR, reflecting an environment where regulatory upgrades (both mandatory and voluntary), increased residential retrofit penetration, and the rise of integrated safety/connected solutions combine to push replacement and new-install volumes upward. This is not a short-term spike but a multi-year market expansion where companies must align product roadmaps and manufacturing footprints to capture share.

Two structural features are notable for strategic planners:

Concentration-driven dynamics: The market’s concentration ratio underlines the power of established electrical-electronics portfolios and channel relationships; competitive moves by top-tier players will disproportionately influence pricing bands and technology adoption curves.

Regulatory cadence as a demand accelerator: Incremental NEC updates and wider state-level adoptions act as discrete demand inflection points that translate into step-function growth for compliant devices—creating windows of elevated opportunity for firms with certified product lines.

Code and standards. The National Electrical Code’s progressive expansion of AFCI requirements, coupled with rigorous testing standards such as UL 1699, means product development cycles must embed extensive validation across series and parallel arc scenarios. Compliance is table stakes; innovation comes from reducing cost-to-certify and accelerating time-to-market.

Material-cost volatility. Copper, silver, and specialty polymers account for a significant majority of production cost in AFCI devices, and the market experienced notable price swings in recent years. Procurement strategies that combine long-term purchasing agreements, alternative-material engineering, and production locality optimization will be decisive for margin protection.

Product convergence. Dual-function devices, plug-on neutral designs, and increasingly, connectivity features targeted at smart homes are reshaping product roadmaps. Differentiation is moving from raw detection performance alone to a mix of ease-of-installation, diagnostics/telemetry, and integration into broader energy-management stacks.

Installation and retrofit economics. The cost and labor profile of retrofitting AFCI protection into existing dwellings remains a critical adoption limiter. Business models that reduce installation time—through receptacle-level solutions, modular breakers, or installer training programs—unlock substantial addressable markets.

The report’s competitive chapter maps incumbent capabilities, recent product launches, and go-to-market postures across the industry’s leading suppliers. Highlights include:

Eaton Corporation — A broad residential AFCI portfolio and recent expansion into slim receptacle formats signal a multi-channel approach focused on compatibility across panel types and installer convenience. Their product breadth and global manufacturing footprint make them a bellwether for pricing and channel terms in North America and beyond.

Siemens AG — Positioned strongly on the performance and safety narrative, Siemens leverages engineering depth to emphasize detection fidelity. Their emphasis remains on embedding AFCI protection in comprehensive electrical-safety offerings.

ABB Ltd. — ABB’s combination and dual-function devices, alongside high-capacity breaker platforms, underscore a strategy that links residential safety with critical-infrastructure resilience. Their recent product releases point to cross-segment playability.

Schneider Electric SE — Schneider differentiates through connectivity and system-level integrations that serve smart-home and commercial property management use cases, aiming to capture higher value through software-enabled services.

Leviton Manufacturing Co. — A long-standing U.S. specialist in receptacles and breakers, Leviton’s emphasis on installer-friendly designs and fire-prevention messaging maintains strong pull in retrofit and residential channels.

CNC Electric — An agile challenger focused on high-performance AFCI devices with rapid global distribution. Their recent product launches indicate an intent to compete on detection performance and cost competitiveness.

General Electric (GE Industrial) — With established credibility in durable breakers, GE’s AFCI offerings aim to serve cross-market needs across residential and commercial segments.

Recent industry moves signal where momentum is building:

January 2026 — CNC Electric launched a high-performance AFCI breaker series that emphasizes advanced arc detection, reflecting challenger strategies centered on technical differentiation.

September 2025 — Eaton expanded its wiring-device portfolio with slim AFCI receptacles, aiming at retrofit-friendly installations and differentiation through form factor.

July 2025 — ABB introduced next-generation breaker technologies focused on energy resilience—an example of how AFCI capabilities are being bundled with broader infrastructure reliability propositions.

Based on the quantitative outlook and scenario work in the report, PW Consulting recommends the following priority moves for industry participants and investors in 2026:

Prioritize certification pipelines. Reduce time-to-market by investing in modular test fixtures and pre-certification partnerships; the ability to align new SKUs with UL 1699 test regimes will determine who wins regulatory-driven waves.

Hedge raw-material exposure. Establish multi-year procurement contracts for copper and critical polymers, explore alternative alloys and conductive plating strategies, and consider nearshoring options for critical components to protect margins against commodity volatility.

Seize retrofit economics. Invest in low-friction installation solutions—slim receptacles, plug-on neutral options, and installer training programs—that lower labor cost per install and accelerate adoption in existing housing stock.

Move up the value stack. For firms with systems capabilities, bundle AFCI devices with connectivity and diagnostic services to capture recurring revenue and lock-in channel partners.

Evaluate bolt-on acquisitions and JV targets. Given the market’s concentration, M&A can be an effective way to acquire certified technologies, channel access, or manufacturing scale—especially in regions where code adoption is accelerating faster than local production capacity.

The published study includes a detailed methodology, base-year sizing, scenario-driven forecasts through 2032, a market-concentration analysis, vendor profiles, product-technology roadmaps, supply-chain risk assessments, and go-to-market playbooks tailored to manufacturers, distributors, and private-equity sponsors. Crucially, the report contains granular segmentation and vendor share analytics that are omitted from this briefing to preserve the actionable value reserved for subscribers.

For product leaders: Use the certification and retrofit modules to sequence SKUs and define a prioritized release calendar aligned with expected local-code adoption timelines.

For supply-chain and procurement teams: Implement the raw-material risk matrix and supplier-qualification checklist to reduce cost exposure and maintain production continuity.

For commercial and channel executives: Leverage the partner evaluation criteria and installer-economics modeling to build distribution and training programs that accelerate retrofit conversions.

For investors and corporate development teams: Consider the acquisition-screening tool and competitive scorecards to identify targets that complement scale, certification footprint, or geographic reach.

The AFCI market in 2026 presents a rare combination of regulatory-driven demand and technological differentiation. Companies that move early to align certification pipelines, stabilize their supply base against commodity volatility, and capture retrofit economics through installer-friendly products will outpace peers. The market’s concentration both raises barriers and clarifies routes to competitive advantage—acquisition, partnership, or focused niche specialization.

PW Consulting’s full Arc Fault Circuit Interrupters Market report provides the underlying data, granular segmentation, and executable frameworks needed to translate the market’s 6.3% CAGR and concentration dynamics into concrete 2026 strategies. Access to the complete dataset and playbooks is available through our subscription portal and will equip your team to convert regulatory momentum into sustainable market share.

For detailed analysis of this topic, please visit the official page:Arc Fault Circuit Interrupters Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com