F3 Firefighting Foam Market: Strategic Imperatives for 2026 — PW Consulting Announces New Market Intelligence Briefing

PW Consulting today releases a strategic industry briefing that synthesizes the latest market dynamics for fluorine-free firefighting foams (F3/FFF). The briefing frames the commercial, regulatory and technological inflection points that will govern procurement, capital investment and supplier strategy through 2026 and beyond. It is designed as an executive decision-support piece for corporate risk officers, procurement leads, airport operators, petrochemical site managers, and public-sector emergency services planning multi-year transitions away from legacy AFFF.

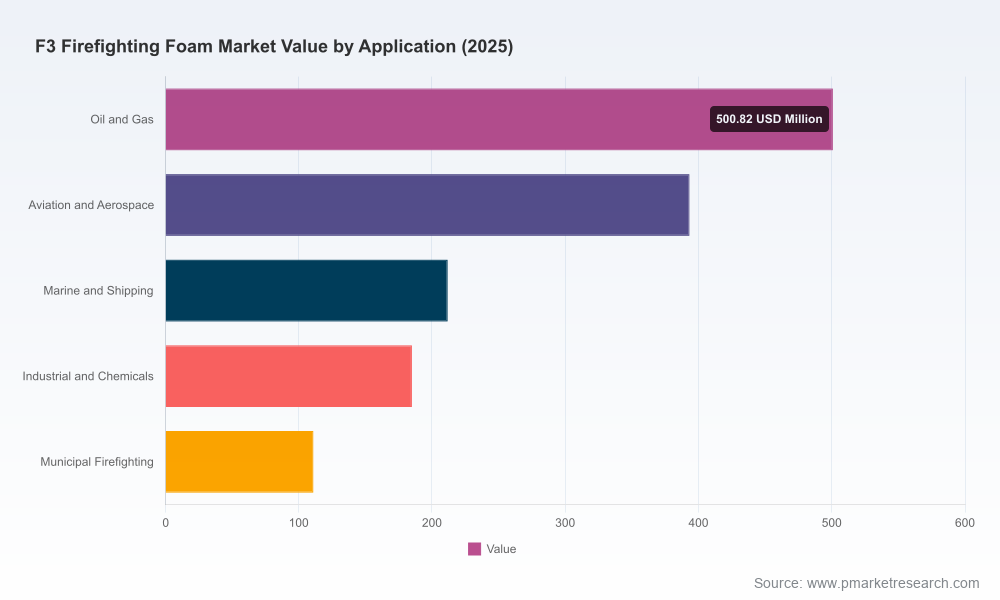

F3 Firefighting Foam Market

Why this matters now: a market in transition

The F3 market has moved from niche environmental demand to mainstream fire-protection procurement. Our analysis shows the sector expanding from approximately USD 810.45 Million in 2020 to USD 1,401.62 Million in 2025, and we forecast further growth to roughly USD 2,954.30 Million by 2032. That trajectory corresponds to a compound annual growth rate of 11.24% across the forecast window — a pace that creates both opportunity and risk for organizations that defer strategic action.

F3 Firefighting Foam Market

Importantly, market concentration remains moderate: the top three suppliers account for roughly a third of global sales, while the top five represent just over half the market. These concentration dynamics inform negotiating leverage, certification pathways and supply-chain resilience for buyers seeking to diversify suppliers without forfeiting performance or compliance.

F3 Firefighting Foam Market

Report highlights — what PW Consulting delivers

- Forward-looking market sizing and revenue scenarios to support capital and operating budgeting through 2032.

- Regulatory impact mapping that translates recent DoD, FAA, IMO and EU actions into procurement timelines and compliance triggers for operators worldwide.

- Supplier scorecards and capability profiles focused on certifications, application coverage (AR/hydrocarbon/polar solvents), biodegradability claims, and quality standards acceptance.

- Operational playbooks for testing, pilot adoption and conversion of fixed and portable systems, including retrofit cost drivers and O&M considerations.

- Risk matrices covering environmental liability, training and legacy stock disposition, plus scenario planning templates for supply disruptions or accelerated regulatory deadlines.

- Negotiation levers and commercial contracting templates tailored to mid-sized and large end-users navigating multi-source supply strategies.

Note: consistent with our "trailer" approach, this public briefing summarizes strategic conclusions while withholding the granular regional, type and application split tables and full supplier scorecards that are provided exclusively in the full report available from PW Consulting.

Regulatory tailwinds and their operational implications

- U.S. Department of Defense transition mandates and FAA guidance have converted what was regulatory risk into procurement momentum for certified F3 agents. Organizations supporting military, airport and DoD-adjacent infrastructure face immediate qualification and testing timelines.

- IMO prohibitions on PFOS-containing foams for offshore units effective from early 2026 shift maritime and offshore procurement to certified fluorine-free alternatives, increasing demand for products with marine approvals.

- EU restrictions and multiple U.S. state bans on PFAS use in training and response compress windows for legacy-product utilization and increase the cost of compliance for entities that retain AFFF inventories.

- Collectively, these measures raise the bar on certification and documented performance; suppliers with recognized approvals (MIL-SPEC, ICAO, EN, IMO, UL/FM listings and equivalent national designations) will capture disproportionately larger procurement share as buyers prioritize de-risking.

Competitive landscape — strategic positioning of leading suppliers

The vendor field is diverse, ranging from long-established chemical houses and niche specialists to regional manufacturers. Several strategic patterns emerge:

- Certification-led differentiation: Market leaders are investing in third-party approvals that unlock large institutional buyers. Recent examples include a leading U.S. supplier securing FM 5130 approval for a Newtonian fluorine-free concentrate in early 2026, reinforcing its suitability for hangar sprinkler systems and other fixed installations. Expect certification rollouts to remain a primary commercial weapon through 2026.

- Legacy advantage and branding: Firms that pioneered fluorine-free chemistry retain reputation capital. Early entrants emphasize proven field performance across aviation, marine and industrial use-cases — an advantage when buyers prioritize low-risk swaps.

- Product breadth vs. niche specialization: Some suppliers focus on comprehensive portfolios that span airport, marine and industrial foams with multiple formulation platforms; others emphasize a smaller range of highly optimized concentrates. Buyers must balance breadth (single-source convenience) against supplier concentration and platform lock-in risks.

- Training and service as value add: Providers that couple concentrate supply with accredited training, live-fire trials and conversion services increase switching costs and accelerate adoption at end-user sites.

- Regional supply dynamics: New entrants and regional champions are expanding manufacturing footprints to address lead time and inventory requirements in emerging demand centers, particularly where local regulatory pressures are strongest.

The full report contains blinded comparative scorecards and scenario-specific supplier shortlists to help procurement teams narrow options without exposing proprietary contract terms publicly.

Recent industry developments underscoring tactical urgency

- March 2026: A major manufacturer secured FM 5130 approval for its Newtonian F3 concentrate — a development that broadens the potential applications for fluorine-free chemistry into fixed sprinkler systems where hydraulic behavior matters.

- Late 2025: Another prominent supplier launched an AR-SFFF product listed at notably low proportioning rates on hydrocarbons, signaling continued product innovation aimed at minimizing dilution and inventory costs for high-volume users.

- Ongoing: Several suppliers now couple product launches with formalized training programs and field demonstration schedules — a recognition that buyer adoption hinges on operational familiarity and confidence in transition procedures.

Strategic recommendations for decision-makers in 2026

Based on our analysis of market dynamics, supplier capabilities and regulatory drivers, PW Consulting recommends the following prioritized actions for organizations taking 2026 procurement decisions:

- Perform an immediate compliance audit: Map your asset base (fixed systems, portable units, ARFF, training grounds) against applicable jurisdictional mandates and certification requirements; identify critical conversion milestones for your high-risk sites.

- Start staged pilots with certified vendors: Execute controlled live-fire trials and small-scale conversions in Q1–Q2 2026 to gather operational data, update SOPs and quantify retrofit costs before committing to enterprise-wide rollouts.

- Rationalize inventory and legacy disposal: Build a compliant plan for retired AFFF handling and disposal that minimizes environmental liability and aligns with insurer expectations; include OEM take-back and recycling clauses where feasible.

- Qualify multiple suppliers: Use supplier scorecards to qualify at least two approved vendors per critical application area to mitigate supply disruption and strengthen negotiating leverage given the market’s mid-level concentration.

- Budget for conversion capex and training: Allocate capital for nozzle, proportioner and sprinkler-system adjustments where required, and invest in certified operator training to reduce human-factor risks during transition.

- Negotiate performance- and certification-linked contracts: Tie pricing and renewal terms to maintenance of certifications and delivery SLAs; include clauses for accelerated supply in case of regulatory changes or product withdrawals.

- Engage insurers and regulators early: Notify insurers of planned transitions, document equivalency testing, and work proactively with local authorities to minimize operational disruptions and permit delays.

How PW Consulting supports your 2026 strategy

Our full F3 market report provides the operational playbooks, supplier scorecards, and financial models that procurement and safety leaders need to build defensible transition roadmaps. It includes: detailed forecast scenarios, certification-by-application matrices, OPEX/CAPEX impact modeling, and negotiated contracting templates for multi-year supply arrangements. The public briefing intentionally omits granular regional and application-level breakdowns; those tables and the vendor scorecards are available in the complete report.

To obtain the full report, validated datasets and customized advisory engagements for site-level transition planning, please visit the PW Consulting publications page or contact our industry team. Early-access advisory slots for Q3–Q4 2026 are limited and prioritized for clients requiring rapid compliance pathways and supplier selection support.

Closing view

The F3 market is no longer a peripheral sustainability play — it is central to regulatory compliance, operational continuity and reputational risk management for major industrial and transport operators. With a robust growth path and accelerating certification activity, 2026 is the year for decisive action: pilots, supplier qualification, contractual protection and training investments. Organizations that move early will capture lower transition costs, strengthen supply resilience, and reduce environmental and regulatory exposure as the market matures.

For detailed analysis of this topic, please visit the official page:F3 Firefighting Foam Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com