Solid State Lasers For Laser Processing Equipment Market — Strategic Preview for 2026 Decision-Makers

PW Consulting’s new market study, Solid State Lasers For Laser Processing Equipment Market, offers an actionable, strategy-first view designed to inform C-suite and corporate development decisions as companies prepare for 2026. The research synthesizes historical performance, a seven-year forecast horizon (2026–2032), technology roadmaps, regulatory constraints, and competitor intelligence into a compact set of plays that leaders can implement immediately. This release previews the report’s strategic value without disclosing the granular segmentation data reserved for subscribers.

Solid State Lasers For Laser Processing Equipment Market

Why 2026 Is a Pivotal Year

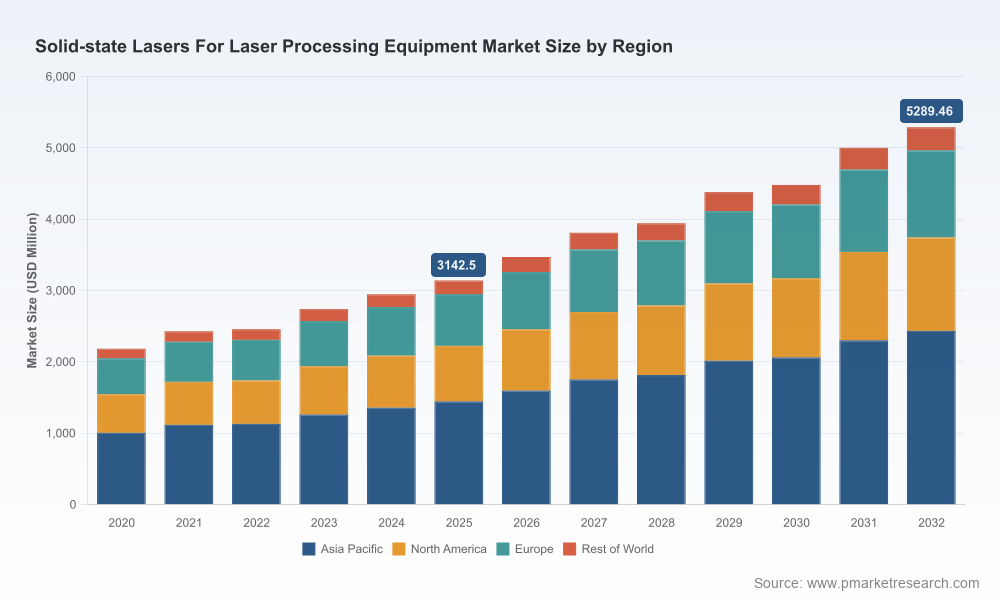

The solid-state laser market for processing has been on a steady upward trajectory, expanding from the low billions in 2020 to over USD 3.1 billion (revenue in USD Million) in the base year 2025. Our forecast models project sustained growth through the 2026–2032 period at a compound annual growth rate (CAGR) of 7.72%, driving the market toward a materially larger addressable opportunity by 2032.

Solid State Lasers For Laser Processing Equipment Market

For executives planning 2026 initiatives, this combination of healthy mid-single-digit growth and technology-driven demand signals three practical imperatives: accelerate capability-mapping for ultrafast and high-brightness platforms; re-evaluate supply‑chain exposure to rare-earth dopants; and prioritize compliance and export-risk mitigation for higher‑power systems. The report converts these imperatives into executable workstreams backed by quantitative scenario analysis.

Solid State Lasers For Laser Processing Equipment Market

What the Report Delivers — Practical, Transaction-Ready Intelligence

- Strategic Forecasting and Scenario Packs: Demand scenarios segmented by technology trajectory and end-use intensity, including upside/downside cases that incorporate raw-material shocks and export-control escalations.

- Technology Roadmaps and Product Positioning Frameworks: Comparative analysis of DPSS, ultrafast, and lamp‑pumped approaches with decision matrices for product investment, migration timing, and modular platform design.

- Go‑to‑Market and Pricing Playbooks: Channel mapping, OEM partnership archetypes, value-based pricing frameworks, and component-cost elasticities to support margin-protective pricing strategies.

- Supply‑Chain and Sourcing Risk Module: Concentration risk metrics, alternative-material pathways, procurement sprint-plans for rare-earth constraints, and hedging strategies aimed at reducing dopant-price volatility impact on gross margins.

- Regulatory & Export Compliance Checklists: Practical steps to certify products against IEC/ISO safety regimes and adapt product families to Wassenaar Arrangement export constraints for high-power systems.

- M&A and Partnership Playbook: Target criteria, valuation sensitivities, and integration checklists for bolt-on acquisitions or joint ventures to capture capabilities in ultrafast processing and fiber-conversion stacks.

- Competitive Positioning and Battlecards: concise, field-ready intelligence on leading suppliers—capability vectors, differentiating features, and go-to-market strengths—designed for bids, RFP responses, and strategic negotiations.

Market Structure and Concentration — What Leaders Must Know

The market demonstrates a material degree of concentration among global suppliers. Our concentration analysis shows that leading manufacturers capture a meaningful portion of global revenue, with the top three firms together controlling close to half of the market and the top five approaching two-thirds. For incumbents and challengers, this structure has strategic implications: scale enables investment in high‑margin ultrafast platforms and global service footprints; challengers must therefore choose focused segments or disruptive cost models to create defensible niches.

Competitive Landscape — Tactical Insights on Core Players

PW Consulting’s report profiles the principal firms shaping product, channel, and innovation dynamics. Below are distilled, decision-relevant observations on the market’s prime movers.

- Trumpf (Ditzingen, Germany): A market leader in disk and rod solid‑state lasers, Trumpf’s recent introduction of an ultrafast TruMicro platform equipped with pulse-on-demand highlights its focus on process efficiency and factory integration. Strategic takeaway: incumbents with deep machine-tool relationships are moving to lock in value through system-level solutions that bundle lasers with automation and service contracts.

- Coherent (Saxonburg, PA, USA): Coherent’s high‑power picosecond offerings signal a push into high-throughput micromachining and semiconductor process steps. Their product cadence underlines an emphasis on repeatability and industrialization of ultrafast modalities. Strategic takeaway: expect continued investment in high-power compact platforms tailored for volume manufacturing customers.

- IPG Photonics (Marlborough, MA, USA): Known for ytterbium-doped fiber lasers, IPG’s demonstrations of high‑brightness modules point to incremental gains in efficiency and beam quality. Strategic takeaway: fiber-based architectures continue to drive total cost of ownership advantages in cutting and welding; vertical integration of modules will remain a priority.

- Lumibird (Lannion, France): As a player with strong Q‑switched Nd:YAG offerings, Lumibird's portfolio speaks to applications requiring pulse energy control and durable pulsed operation. Strategic takeaway: niche application focus—marking, engraving, and selective ablation—remains defensible under cost and reliability criteria.

- Spectra‑Physics (MKS Instruments) (Santa Clara, CA, USA): With ultrafast Spirit and Empower series, Spectra-Physics is doubling down on microstructuring and surface-treatment markets where precision is the premium. Strategic takeaway: companies targeting sub-micron process windows must prioritize partnerships with ultrafast OEMs and invest in process validation labs.

- ROFIN‑SINAR (Coherent subsidiary) (Hamburg, Germany): The pulsed StarPulse lineage continues to address high-energy drilling and metal-cutting tasks; under Coherent’s umbrella, product rationalization and channel consolidation should be expected. Strategic takeaway: M&A-driven product portfolio optimization creates opportunities for specialized integrators to pick up legacy lines or service contracts.

Regulation, Standards, and Supply Risks — Operational Implications

Compliance and raw-material exposure are non-trivial operational variables. The IEC 60825-1 family and ISO 11553 series prescribe safety and machine-level requirements that directly affect system design, time-to-market, and capital outlay for certification. Separately, high-power systems face export-control scrutiny; systems with output above certain thresholds are subject to dual‑use controls, adding licensing overhead and transaction risk for international sales.

On the input side, the market depends on rare-earth dopants such as neodymium and ytterbium. Our supply-chain stress tests model price volatility scenarios where dopant costs swing by 20–30% annually—a realistic range given current mining dependencies. These shocks propagate into component lead times and margin compression unless companies implement material-substitution roadmaps, strategic inventory, or locked supplier agreements. The report contains playbooks to operationalize each mitigation approach.

Strategic Plays for 2026

- Prioritize Modular Ultrafast Investments: Allocate R&D and CapEx to modular ultrafast platforms that enable incremental upgrades (pulse duration, repetition rate) rather than full-platform replacements. This protects upgrade economics and shortens sales cycles to industrial customers.

- Hedge Supply Exposure: Implement a two-tier procurement strategy combining long-term supply agreements for critical dopants with a tactical spot program. Pursue engineering-to-cost initiatives targeting material substitution or reduced dopant loading.

- Export-Aware Product Segmentation: Re-architect product families to create export-friendly SKUs beneath high-power thresholds and maintain a separate high-performance portfolio for licensed or controlled-market sales.

- Service and Digital Monetization: Convert installed-base advantages into recurring revenue through remote diagnostics, consumables, and performance-based service contracts tailored to high-utilization industrial accounts.

- M&A and Partnering Targets: Seek tuck-in acquisitions that add complementary processing capabilities (e.g., beam-shaping modules, process software) and leverage partnerships to accelerate entry into adjacent high-growth end markets.

How This Report Supports Board-Level Decisions

Boards and strategy teams will find this study particularly useful as a due-diligence backbone for capital allocation, M&A screening, and product-roadmap approval. We translate market-size growth, concentration metrics, supply‑chain risk, and regulatory overlay into measurable KPIs and investment thresholds. The intent is pragmatic: reduce decision ambiguity for 2026 by turning macro trends and competitor moves into short, medium, and long-term action plans with measurable outcomes.

Next Steps and Access

This article is a preview designed to surface the report’s strategic value while preserving the proprietary granularity that actionable plans require. PW Consulting’s full Solid State Lasers For Laser Processing Equipment Market report includes detailed model outputs, segmented demand drivers, pricing elasticities, and executable playbooks. To access the full analysis, proprietary data tables, and subscriber-only workshops that translate the findings into an implementation timeline for 2026, please visit the report landing page on our website.

For immediate advisory engagements, custom scenario builds, or to commission a tailored market-entry or M&A scouting mandate aligned with the findings, PW Consulting’s industry strategy team is available for a consultation.

For detailed analysis of this topic, please visit the official page:Solid State Lasers For Laser Processing Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com