Absorbable Cranial Clamp Market — Strategic Briefing for 2026 Decision-Makers

Executive summary

PW Consulting’s latest market research on absorbable cranial clamps delivers a clear, evidence-based narrative for boards, corporate strategists, and clinical commercial teams preparing decisions in 2026. Drawing on a validated historical series (2020–2025) and our forecast horizon (2026–2032), the report situates the market within an incremental-growth environment driven by clinical innovation, regulatory evolution, and concentrated competitive dynamics. At the market level, the sector is projected to expand at a mid-single-digit compound annual growth rate (CAGR) through the forecast period, underscoring steady commercial opportunity but also highlighting the need for granular, execution-focused strategies to capture value.

Absorbable Cranial Clamp Market

Market trajectory and macro outlook

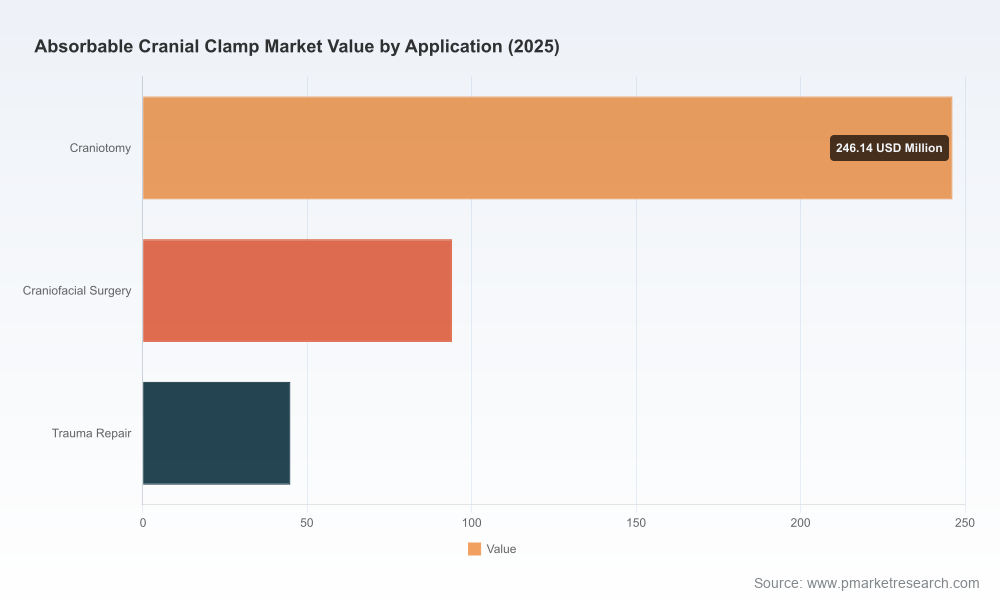

Using 2025 as the analytical base year, PW Consulting models show the absorbable cranial clamp market growing from its early-decade size to a materially larger market by the end of the 2032 forecast. Our quantitative model, calibrated to procedure volumes, pricing trends, product life cycles, and adoption curves, produces a clear expansion path over 2026–2032 under a central scenario that reflects current regulatory and clinical realities. The market’s concentration metrics indicate a moderately consolidated structure, with the top three and top five players commanding a significant portion of the current market — a dynamic that shapes pricing power, channel behavior, and partnership incentives.

Absorbable Cranial Clamp Market

Why this matters for 2026 decisions

- Prioritize scalable clinical evidence: With reimbursement and hospital procurement increasingly evidence-driven, investing in targeted, multicenter clinical programs that demonstrate not only mechanical equivalence but bone-healing and patient-reported outcomes will be decisive.

- Time-to-market and regulatory strategy are differentiators: Recent 510(k) clearances and pathway optimizations have lowered barriers in some jurisdictions, but regulatory timelines still materially affect ROI windows. Strategic sequencing of submissions across geographies can accelerate adoption while managing cost.

- Channel and OEM partnerships will be strategic levers: Given current market concentration, smaller entrants should consider selective licensing, distribution alliances, or OEM supply agreements to gain access to established procurement channels without excessive commercial investment.

- Commercial focus should be surgical-procedure specific: Adoption velocity varies by surgical sub-specialty and institutional practice patterns. Sales deployment that aligns with high-volume neurosurgical centers and centers of excellence will generate advocacy and diffusion faster than broad, unfocused coverage.

Competitive landscape — who matters and why

Our competitive mapping combines product design attributes, clinical evidence, regulatory status, and commercial footprint to identify strategically viable pathways. Three companies consistently surface as reference points for incumbency, innovation, and regional disruption:

Absorbable Cranial Clamp Market

- B. Braun Melsungen AG (Aesculap) — Aesculap’s CranioFix Absorbable system exemplifies engineered polymer solutions that balance initial fixation strength with predictable resorption. Its multi-year absorption profile and instrument-free design have established it as a clinical default in numerous institutions, contributing to durable hospital contracts and a recognized brand advantage.

- Johnson & Johnson (DePuy Synthes) — DePuy Synthes’ RAPIDSORB offering, built on a defined PLGA copolymer formulation, is positioned around rapid resorption and short-term mechanical stability demands. Its stability profile in the early postoperative window targets surgeon concerns around immediate fixation without long-term implant presence.

- MedArt Technology Co., Ltd. — An emergent innovator from China, MedArt has advanced high-purity PLLA-based fixation systems and recently reported multicenter clinical evidence indicating non-inferiority on stability metrics and promising bone-healing signals in comparative settings. The firm’s FDA 510(k) clearance in recent years has materially changed its addressable market and competitive posture in key markets.

Each of these players demonstrates distinct go-to-market logics: incumbent global medtechs leverage scale, integrated portfolios, and surgeon relationships; regionally-focused innovators compete on cost, localized evidence generation, and nimble regulatory strategy. Our report translates these dynamics into practical options for potential entrants, incumbents contemplating portfolio plays, and private investors evaluating M&A targets.

Recent developments and what they imply

- Clinical differentiation is emerging beyond “fixation equals fixation.” Recent multicenter trials have begun to surface bone-healing as a meaningful secondary endpoint — an outcome that can shift procurement preferences where long-term cranial integrity is prioritized.

- Regulatory clearances continue to be a gating factor but are increasingly navigable for well-prepared programs. Clearance pathways observed in recent years underscore the value of early regulatory engagement and harmonized data sets designed to satisfy multiple jurisdictions.

- Material science remains a practical battlefield: established formulations that prioritize extended strength retention contrast with newer copolymer strategies favoring more rapid resorption. The commercial trade-offs between handling characteristics, implant longevity, and manufacturing complexity will affect cost structures and reimbursement negotiations.

What the PW Consulting report contains — practical components

This study is designed not as an academic survey but as a toolbox for decision-makers. Key deliverables include:

- A validated historical market model (2020–2025) and a scenario-based forecast (2026–2032) with sensitivity testing around procedural volumes, pricing, and adoption curves.

- Competitive scorecards that evaluate product architecture, clinical evidence strength, regulatory status, manufacturing readiness, and commercial reach.

- Regulatory pathway playbooks for major jurisdictions, including dossier templates, recommended pivotal endpoints, and time/cost estimates for 510(k) and equivalent routes.

- Commercial go-to-market blueprints: segmentation of hospital types, prioritized clinical champions, distributor selection criteria, and sample incentive frameworks for early-adopter programs.

- Manufacturing and supply-chain assessment: supplier risk matrices, capital cost benchmarks for polymer processing, and scale-up timelines tied to demand curves.

- Valuation and M&A roadmap: target screen, deal structure considerations, and integration risk checklists that reflect current market concentration and growth expectations.

Actionable recommendations for 2026 planning

- Embed clinical endpoints that buyers value. Design registries and randomized comparative cohorts to demonstrate both mechanical equivalence and bone-healing or patient-centric outcomes.

- Sequence market entry by balancing regulatory speed with commercial potential. A dual-track approach — rapid clearance in one jurisdiction to generate early clinical data, followed by broader filings — reduces time-to-evidence while preserving geographies for full launches.

- Negotiate collaboration pathways with incumbent portfolio players rather than direct head-to-head commercial launches when access to OR-level channels is limited. Co-marketing or OEM supply can be a lower-capex route to scale.

- Invest in manufacturing quality and supply redundancy early. Polymer-based implants have tight process controls; early capital allocation to validated processing reduces the risk of post-market supply interruptions.

- Use targeted pricing pilots tied to demonstrated clinical value. Value-based contracting pilots with high-volume centers can accelerate adoption while generating real-world evidence to support broader pricing premiums.

Risks, signals to monitor, and suggested KPIs

Key risks include changes in hospital procurement criteria, faster-than-expected innovation in alternative fixation technologies, and shifts in polymer raw-material pricing. We recommend monitoring:

- Procedure volumes at top-tier neurosurgical centers (quarterly)

- Time-to-coverage decisions from major payers and hospital GPOs (median days)

- Rate of clinical adoption in targeted centers (early-adopter conversion rate)

- Supply-chain lead times for polymer inputs and finished-device replenishment

How to use this briefing — next steps

PW Consulting’s analysis is structured to support three immediate 90–180 day initiatives for 2026 planning cycles:

- Portfolio Prioritization: use our decision matrix to rank clinical and commercial projects by net present value under multiple adoption scenarios.

- Clinical Program Design: adopt the suggested core-plus registry model to generate both regulatory and commercial evidence with minimal incremental cost.

- Partner and M&A Scouting: deploy the target-screening framework to prioritize assets that fill critical capability gaps (clinical evidence, regulatory access, or manufacturing scale).

Closing note — why the full report is essential

This public briefing outlines strategic implications and high-level market dynamics. The full PW Consulting report contains the granular datasets, regional and application splits, downloadable financial models, and proprietary scoring that are necessary to build detailed business cases, negotiate deals, and finalize go-to-market budgets. For teams preparing 2026 budgets and three-year strategic plans, that granularity — including scenario tables, hospital-level adoption curves, and supplier cost benchmarks — is the difference between an informed hypothesis and an executable plan.

To access the full dataset, segment-level analysis, and the practical templates referenced here, please refer to the PW Consulting report page where subscribers can download the complete research package and interactive forecast model.

For detailed analysis of this topic, please visit the official page:Absorbable Cranial Clamp Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com