How Smart Equipment Is Revolutionizing the Crawler Dozers Market

Dance |

2026-06-25 13:43:03

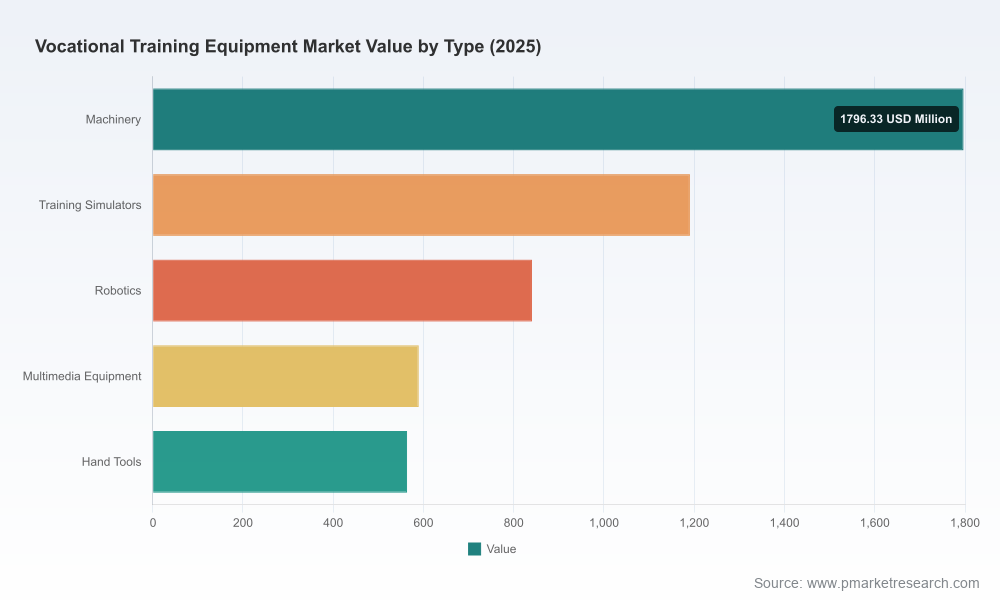

PW Consulting’s latest Vocational Training Equipment Market report positions executive teams to make confident, high‑impact decisions in 2026. Built on a 2020–2025 historical base with 2025 as the base year and a 2026–2032 forecast horizon, the study quantifies an industry that reached approximately USD 4,980 Million in 2025 and is forecasted to grow at a steady 4.6% CAGR across the projection period to a multi‑billion dollar market by 2032 (revenues reported in USD Million). The analysis blends granular vendor intelligence, scenario modeling, supply‑chain stress testing, and actionable go‑to‑market playbooks — enough depth to inform immediate strategic choices while directing readers to the full report for proprietary segment matrices, pricing benchmarks, and vendor scorecards.

Vocational Training Equipment Market

Procurement and CAPEX alignment — The market’s steady mid‑single‑digit growth and visible troughs/peaks across the historical series make 2026 a pivot year for capital plans: choose between accelerated modernization or phased investment tied to curricular adoption cycles.

Vocational Training Equipment Market

Supply‑chain and cost risk mitigation — New trade measures and raw‑material dynamics are reshaping onshore vs. offshore sourcing economics, making supplier footprint strategy and hedging policies business‑critical.

Vocational Training Equipment Market

Product and service mix optimization — Hardware remains core, but software, simulation, and lifecycle services are growing strategic importance: a shift in revenue mix is underway and must be planned for at the board level.

Regulatory compliance and safety standards — The latest ISO guidance on stationary training equipment introduces compliance thresholds that change product development and warranty exposure assessments.

Methodology and transparent market‑sizing framework (historical tracking, bottom‑up vendor validation, demand drivers, and model assumptions).

Seven‑point vendor benchmarking toolkit covering product breadth, curriculum integration, after‑sales maturity, geographic reach, price bands, customization capability, and technology roadmap.

Scenario models and sensitivity analyses (tariff shocks, raw‑material spikes, accelerated digital substitution) with quantified P&L and working‑capital outcomes for representative profiles.

Operational playbooks: sourcing hedges, local assembly options, modular design templates for rapid curriculum upgrades, and service‑based commercial models (subscription, outcome‑based contracting, multi‑year maintenance agreements).

Regulatory and standards impact assessment, including implementation guideposts to meet new safety criteria and testing protocols.

M&A and partnership roadmaps: target archetypes, valuation heuristics, and integration checklists for bolt‑on deals or strategic alliances.

Opportunity heatmaps and prioritization matrices for product teams and commercial leadership (by technology theme, institutional buyer profile, and go‑to‑market channel).

Technology convergence is accelerating. Traditional mechanical trainers and hand tools remain indispensable in vocational curricula, but robotics, advanced simulators and multimedia learning environments are closing the learning‑outcome gap faster than ever. Buyers increasingly demand interoperability with Industry 4.0 toolchains and remote learning capabilities.

Public and private vocational programs are expanding capacity. Major manufacturers and system integrators are launching training initiatives and software suites that integrate with institutional curricula — a trend that increases adoption velocity for vendors able to offer end‑to‑end solutions.

Cost inflation and trade policy are real constraints. For example, recent tariff adjustments on steel and aluminum and the related rise in hot‑rolled coil steel prices materially raise input costs for metal‑intensive rigs and simulators; this changes the total cost of ownership calculus for both buyers and suppliers.

Standards and liability exposure are tightening. The release of new ISO safety requirements for stationary training equipment necessitates product re‑qualification and changes to testing and documentation practices — noncompliance risks both market access and brand reputation.

Market concentration is meaningful but not monopolistic (CR3 and CR5 metrics indicate a mid‑range consolidation profile). Competitive dynamics blend established industrial learning system leaders with regional manufacturers focused on price and distribution. Key strategic profiles to watch include:

Amatrol — a leader in hands‑on training systems with strong curriculum integration and long tenure in advanced manufacturing and mechatronics education. Favorable for partnerships where curriculum credibility and instructor support are mission‑critical.

Festo Didactic — excels in factory and process automation learning systems; strong positioning where pneumatics, hydraulics, and Industry 4.0 simulation form the nucleus of vocational programs.

Lucas‑Nülle — known for high‑quality electrical and automation trainers with didactic, project‑oriented approaches that suit higher‑education and vocational lab environments.

FANUC America — strategically important where certified robotics education and CNC training are essential; offers an anchor for automation‑led curricula and OEM relationships.

Regional manufacturers (China/India/EU) — companies focused on TVET lab kits and cost‑competitive trainers provide broad geographic coverage and rapid local deployment options; they influence pricing thresholds and distribution strategies.

Recent vendor moves underscore the strategic playbook: multinational automation firms are forming partnerships to bundle hardware and metrology tools, while software and training suites from major automation vendors are pushing for curriculum standardization at scale. These dynamics create both opportunity (fast route to market via partners) and risk (increased competition on software and services).

Revisit sourcing architectures now: model landed cost under multiple tariff and freight scenarios and prioritize flexible local‑assembly nodes for heavy metal‑intensive equipment.

Shift product development budgets toward modular, software‑enabled simulators and remote training capabilities that reduce deployment cost and increase recurring revenue potential.

Design service and curriculum bundles: convert one‑time equipment sales into multi‑year relationships through subscription licensing, content updates, and certification programs.

Prioritize compliance investments: allocate near‑term product re‑engineering resources to meet new ISO safety standards and adjust warranty/legal frameworks to lower liability exposure.

Pursue selective alliances with automation OEMs and metrology vendors to accelerate route‑to‑market for integrated learning systems and to co‑develop accredited curricula.

Use M&A to acquire niche IP (simulation software, EV/hybrid training modules) or regional distributors that provide immediate channel and inventory leverage.

Tariff escalation and raw‑material spikes — rapid cost pass‑through to customers, margin compression, and inventory write‑downs unless hedges or local manufacturing are deployed.

Fast digital substitution — if virtual labs and cloud‑based simulation reach price parity with physical rigs, hardware demand could rebase; mitigate by bundling hardware with exclusive content and accreditation.

Standards‑driven product obsolescence — new safety and testing requirements may require immediate circuit redesign, causing short‑term production disruption and requalification costs.

Policy shifts in vocational funding — public funding increases rapidly in some markets but slows in others; maintain agile commercial strategies by maintaining mixed public/private customer pipelines.

Procurement teams: use the report’s supplier TCO templates to renegotiate contracts and to run make‑vs‑buy analyses under realistic tariff scenarios.

Product teams: apply the vendor benchmarking matrix to prioritize feature development and partner integrations that unlock higher‑margin service revenue.

M&A teams: use the target archetype and valuation heuristics to screen acquisition candidates that accelerate digital capability or geographic reach.

Policy and compliance teams: follow the standards implementation roadmap to de‑risk product launches and institutional deployments.

This briefing is deliberately high‑level to highlight strategic implications and immediate actions for 2026. PW Consulting’s full Vocational Training Equipment Market report contains the proprietary sub‑segment tables, regional and application heatmaps, vendor scorecards with comparative pricing bands, and downloadable scenario models that underwrite the recommendations above. Executive summaries, tailored briefings, and custom workshops for procurement, product, and M&A teams are available on request.

To access the complete data set, detailed vendor assessments, and forward‑looking scenario models that underpin this guidance, please visit the PW Consulting report page or contact our industry practice for an executive briefing.

For detailed analysis of this topic, please visit the official page:Vocational Training Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com