Trimethylaluminum (TMA) for High-Purity Applications: Strategic Imperatives for 2026 — PW Consulting Market Brief

As the microelectronics, LED and photovoltaic industries enter a new cycle of capital deployment and process refinement, Trimethylaluminum (TMA) is rapidly reasserting its strategic value as a high-purity precursor. PW Consulting’s new market research briefing — covering historical performance (2020–2025) and a forward-looking forecast for 2026–2032 — synthesizes supply dynamics, regulatory headwinds, supplier positioning and actionable procurement playbooks to inform executive decisions in 2026.

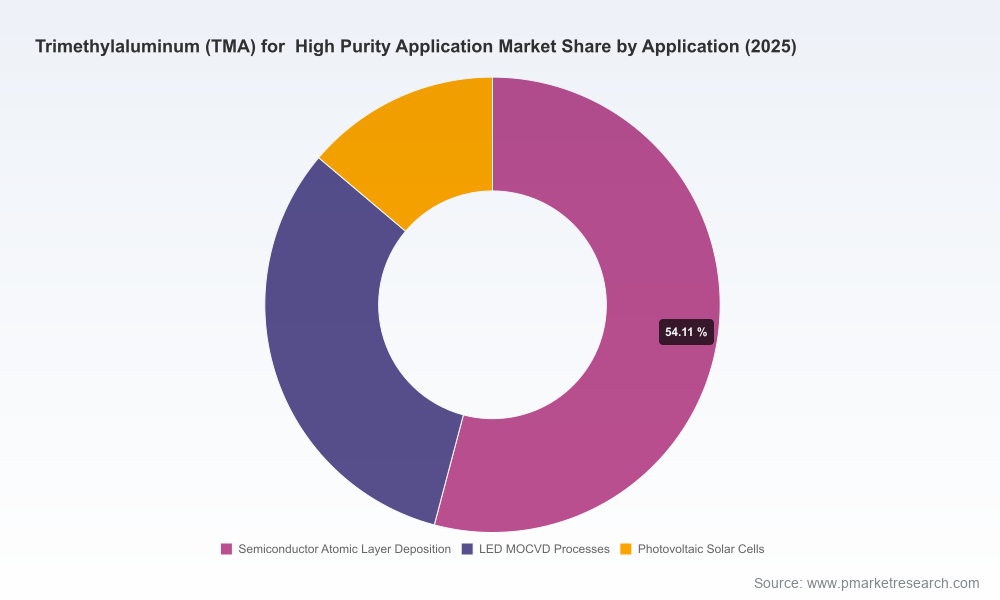

Trimethylaluminum Tma For High Purity Application Market

Why this briefing matters for 2026 decision-makers

- Macro traction: Our model shows the global high-purity TMA market expanding at a compound annual growth rate (CAGR) of 8.2% over the 2026–2032 forecast window. This growth profile makes TMA a material category for procurement, process R&D and capacity planning in adjacent advanced materials strategies.

- Concentration and supplier risk: The market exhibits a high level of concentration — the top three firms command a majority share, and the top five dominate the supply landscape. This concentration amplifies counterparty, capacity and pricing risks for buyers that rely on single-source supply or have compressed qualification timelines.

- Cross-industry leverage: TMA’s centrality to atomic layer deposition (ALD), metal-organic chemical vapor deposition (MOCVD) and Al2O3 passivation means decisions in semiconductor fabs, LED manufacturers and solar cell producers will have knock-on effects across the supplier ecosystem.

Headline market trajectory (strategic datapoints)

- Base year: 2025 (report base year and the final year of our historical series).

- Short-to-medium term outlook: The market is modeled to grow robustly through 2032 at a projected CAGR of 8.2% (2026–2032), reflecting recovery and reinvestment cycles in semiconductors, continued LED optimization, and selective uptake in high-efficiency photovoltaic processes.

- Revenue trajectory: PW Consulting’s topline modeling details the market’s progression from the 2025 baseline through 2032, providing scenario bands for conservative, base and accelerated growth cases to support capital and sourcing decisions.

Note: This brief intentionally omits the detailed regional and application splits contained in the full report to preserve strategic value for subscribers and to direct stakeholders to the full dataset and interactive dashboards.

Trimethylaluminum Tma For High Purity Application Market

Competitive landscape — what senior managers need to know

The TMA supply chain is anchored by a set of vertically integrated and specialty chemical producers. Our qualitative assessment of core providers highlights complementary strengths that shape commercial choices and contracting strategies:

Trimethylaluminum Tma For High Purity Application Market

- Albemarle Corporation (Charlotte, NC, USA) — Positioned as one of the largest high-volume producers, with multiple high-purity TMA grades configured for semiconductor ALD/CVD, solar and LED markets. Albemarle’s integrated North American production footprint and scale provide reliability but can also be sensitive to regional feedstock and logistics dynamics.

- Nouryon (Amsterdam, Netherlands) — A specialty producer that emphasizes ultra-high purity grades and consistent manufacturing controls tailored for electronics. Their positioning favors OEMs and fabs requiring highly consistent lot-to-lot purity and documentation packages.

- Nagase (Tokyo, Japan) — Focuses on ultra-low impurity electronic-grade TMA and global technical support; attractive to customers prioritizing vapor-phase performance and qualification support for advanced process nodes.

- Dockweiler Chemicals (Germany), American Elements (USA), and a set of East Asian producers (including Hunan Heaven, Jiangsu Nata, Argosun and Lake Materials) — These firms form a capability layer providing a mix of specialty grades, regional logistical advantages and alternative supply options for qualification or surge demand.

Recent supplier developments underscore both continuity and tactical shifts: Tier-1 producers have continued to advance production processes and grade portfolios to support semiconductor and optoelectronic customers, while several suppliers have emphasized global availability and low-impurity performance as part of their commercial messaging. Such developments influence buyer lead times, qualification windows and long-term contracting choices.

Supply chain & raw material dynamics to monitor

- Aluminum feedstock volatility: Primary aluminum is a critical upstream input for TMA manufacture. Early-April 2026 price points indicate elevated feedstock costs, with direct implications for pricing pass-through, margin compressions for producers, and procurement hedging strategies for large consumers.

- Bauxite and sourcing risk: The broader aluminum supply chain is exposed to geopolitical and critical-material designations; the EU’s classification of bauxite as a Critical Raw Material speaks to structural supply risk that can cascade downstream into metal alkyl supply.

- Trade and tariff considerations: Trade policy measures — including aluminum-related tariffs and tariff-rate quotas — continue to shape North American feedstock availability and cost. Organizations with North American manufacturing footprints should account for tariff scenarios in their 2026 sourcing playbooks.

- Regulatory compliance and handling costs: Aluminum alkyls such as TMA are pyrophoric and tightly regulated. Compliance with OSHA, REACH and comparable frameworks increases operational costs, warehousing requirements and supplier qualification hurdles.

What the full PW Consulting report delivers (practical, actionable content)

For decision-makers requiring executable outputs, the full study contains:

- Granular demand and supply modeling with historical data (2020–2025) and detailed forecasts (2026–2032) including scenario—base—upside bands to stress-test investment cases.

- Supplier scorecards and vendor diligence templates covering technical capability, quality systems, lot traceability, logistical reliability, and commercial terms to fast-track vendor selection and dual-sourcing strategies.

- Price benchmarking and input-cost pass-through analysis linked to primary aluminum indices and trade policy scenarios to support procurement hedging and forward-purchasing decisions.

- Regulatory matrix and safety-compliance checklist aligning OSHA/REACH/transportation requirements with CAPEX/OPEX implications for storage and handling at fabs and chemical intermediates sites.

- Contracting playbook with recommended commercial constructs (including strategic term lengths, volume-flex clauses, force majeure specifics for hazardous materials and inventory consignment models) tailored for both buyers and suppliers.

- Risk register and mitigation blueprints — covering feedstock shocks, production outages, qualification delays and certification bottlenecks — with recommended KPIs and governance rhythms for procurement and operations leaders.

- Near-term M&A and capacity outlook, identifying where mid-tier producers and regional players could become strategic acquisition targets or partners for securing regional supply continuity.

Strategic recommendations for 2026

- Prioritize dual-sourcing with at least one Tier-1 integrated supplier and one specialty regional supplier to balance scale reliability and qualification flexibility.

- Institute a 12–18 month qualification pipeline for alternative suppliers; lead times for ALD/CVD grade approvals remain a primary gating item.

- Hedge feedstock exposure by linking procurement cycles to aluminum price indices and by negotiating pass-through caps or collars in supply agreements.

- Invest in on-site handling and safety infrastructure early — compliance costs and lead times for permits can materially affect go-live dates for new capacity or process lines using TMA.

- Monitor regulatory and trade policy developments closely; incorporate scenario planning for tariff escalations and critical raw material access constraints into capital allocation decisions.

Risk scenarios & monitoring dashboard

PW Consulting’s scenario framework identifies three principal outcomes through 2028:

- Constrained Supply Scenario — triggered by raw material price shocks, a major producer outage or new regulatory restrictions; this raises premium on validated high-purity lots and favors integrated suppliers with secure feedstock access.

- Steady Growth Scenario — baseline case where demand growth tracks capital investments in semiconductors and optoelectronics, allowing for orderly market expansion and moderated price increases.

- Acceleration Scenario — advanced packaging, new ALD chemistries and expanded solar passivation uptake catalyze faster adoption; buyers who locked volume contracts early capture favorable economics and priority allocation.

PW Consulting subscribers receive a live monitoring dashboard that maps these scenarios to leading indicators including aluminum spot prices, supplier capacity disclosures, regulatory notices and trade policy moves.

How to use this briefing in 2026 planning cycles

- Procurement teams: Use the supplier scorecards and pricing scenarios to structure multi-year supply agreements and to define volume-flex mechanics tied to wafer starts or production ramps.

- R&D and process engineering: Align qualification timelines for alternate TMA grades with equipment vendor windows; prioritize vapor-phase impurity profiles rather than nominal purity labels alone.

- Corporate strategy and M&A: Evaluate mid-market producers as strategic bolt-ons to secure regional supply or to internalize specialty grade production where logistics or compliance risks are material.

Accessing the full intelligence

This press brief highlights the strategic implications of PW Consulting’s Trimethylaluminum market work. The full study contains the proprietary regional and application splits, supplier scorecards, price benchmarks and downloadable models that senior stakeholders require to operationalize their 2026 strategies. To obtain the comprehensive dataset, interactive dashboards and advisory support, please visit PW Consulting’s report page or contact our industry practice leads for a tailored briefing and near-term advisory engagement.

PW Consulting — helping materials, semiconductor and clean-energy leaders convert market intelligence into decisive action.

For detailed analysis of this topic, please visit the official page:Trimethylaluminum Tma For High Purity Application Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com