Post-Weight Loss Surgery in Dubai Healing Process

Health |

2026-05-20 12:06:53

PW Consulting today publishes a forward-looking industry brief that frames the commercial inflection point for solid state chip batteries. As lead author and Chief Industry Analyst at PW Consulting, I present a synthesis designed to inform executive decision-making in 2026 — capturing where the market is, how it will evolve, and which strategic moves materially change outcomes for OEMs, component suppliers, investors and regulators. This summary highlights the analytical rigor of our full report while preserving the proprietary, segment-level intelligence that commercial clients use to act decisively.

Solid State Chip Battery Market

Solid state chip batteries have moved from laboratory promise into early commercial traction. Our bottom-up model pegs the overall market at approximately USD 245 million in the 2025 base year, accelerating to an expected USD 296 million in 2026 and tracking to roughly USD 828 million by 2032, implying a compound annual growth rate (CAGR) of about 19% across the forecast window. That trajectory reflects sustained demand across micro-power and larger format applications, compressed commercialization timelines for automotive and industrial prototypes, and accelerating investment in pilot manufacturing capacity.

Solid State Chip Battery Market

These macro figures understate the heterogeneity within the market: technology readiness, manufacturing scale, customer qualification processes, and regulatory acceptance vary widely across suppliers and applications. Our report quantifies those deltas and overlays scenario-based forecasts that show how targeted investments or regulatory shifts could materially reallocate value among incumbent battery manufacturers, new entrants and component specialists.

Solid State Chip Battery Market

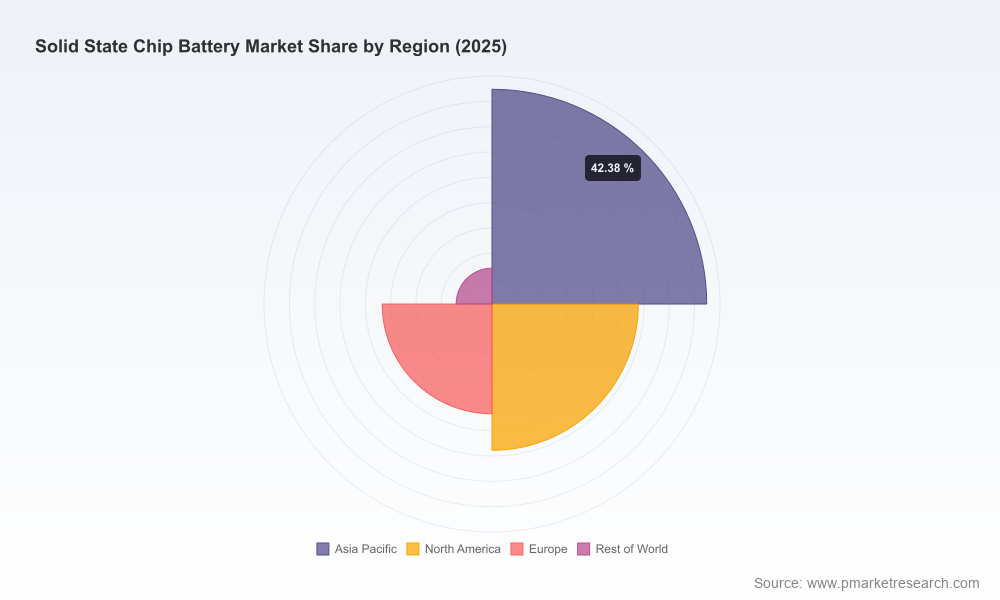

To preserve the strategic value of the analysis, detailed tables and segment-level figures (including regional and application splits) are available exclusively in the full report.

The competitive field blends deep-pocketed incumbents, nimble specialists, and developer-suppliers with close OEM partnerships. Across this ecosystem we see differentiated routes to scale and defensibility:

Recent, material developments underscore this dynamic:

2026 is a pivotal year for the regulatory and standards environment. National and international actions — including planned technical standards from major markets and air-shipment state-of-charge restrictions that recently took effect — are shaping logistics, design constraints and certification timelines. Simultaneously, safety standards committees are developing tailored test methods for solid-state chemistries, creating new compliance pathways but also temporary uncertainty during standard harmonization.

On the manufacturing front, solid electrolyte materials remain a primary cost and process hurdle. Relative material costs and the need for moisture-controlled, scalable assembly remain acute challenges. Our supply-chain analysis quantifies the production inflection points where economies of scale and process innovation can reduce per-cell costs to compete with incumbent Li‑ion solutions in select use-cases.

Our brief synthesizes proprietary modeling, factory-level cost analysis, interviews with technology developers and OEM procurement leads, and an up-to-the-minute review of regulatory developments to create a practical roadmap for 2026 investments. The report translates headline growth into specific choices: where to spend, whom to partner with, which standards to track closely, and which commercial milestones signify market unlocking.

Importantly, this release follows a “trailer” approach: it demonstrates the depth of our methodology and the strategic implications we draw, while withholding detailed segment tables and proprietary split data that are essential for tactical execution. Those datasets — including granular regional, application and type-level forecasts, supplier scorecards and the full manufacturing cost curves — are included in the full PW Consulting report and are available through our client portal.

If you are making capital allocation, partnership, product or regulatory engagement decisions in 2026, this brief should be the starting point of your planning cycle. Contact PW Consulting to request the complete Solid State Chip Battery Market report, schedule a strategy workshop, or commission bespoke modeling aligned to your product roadmap.

PW Consulting’s market intelligence is designed to convert high-level growth narratives into executable strategies. For organizations that need to move from experimentation to commercial scale in 2026, informed, timely choices will determine who captures the disproportionate value in the decades to come.

For detailed analysis of this topic, please visit the official page:Solid State Chip Battery Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com