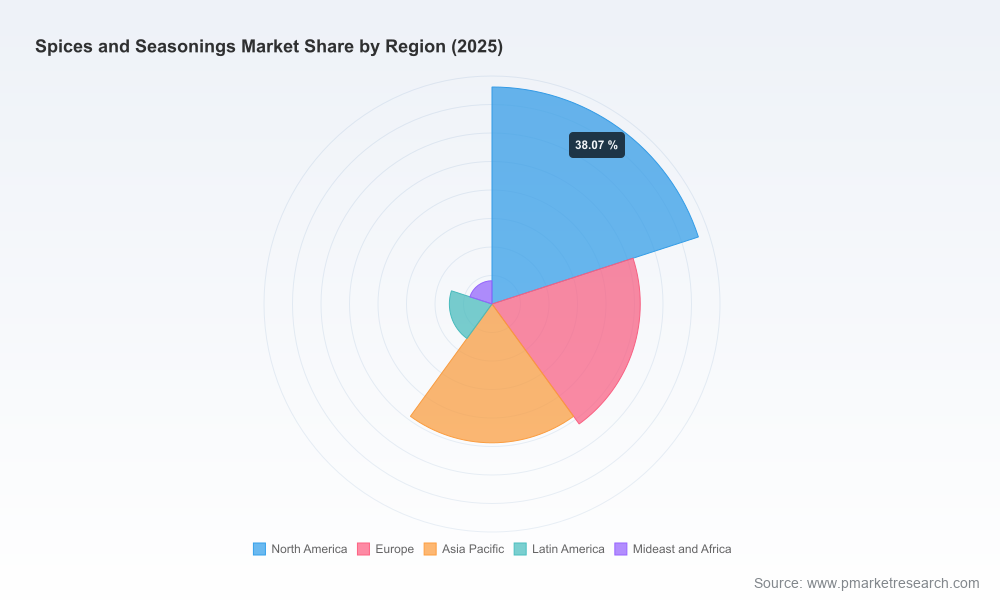

PW Consulting: Spices & Seasonings poised for 5.5% CAGR through 2032

Health |

2026-07-09 15:47:22

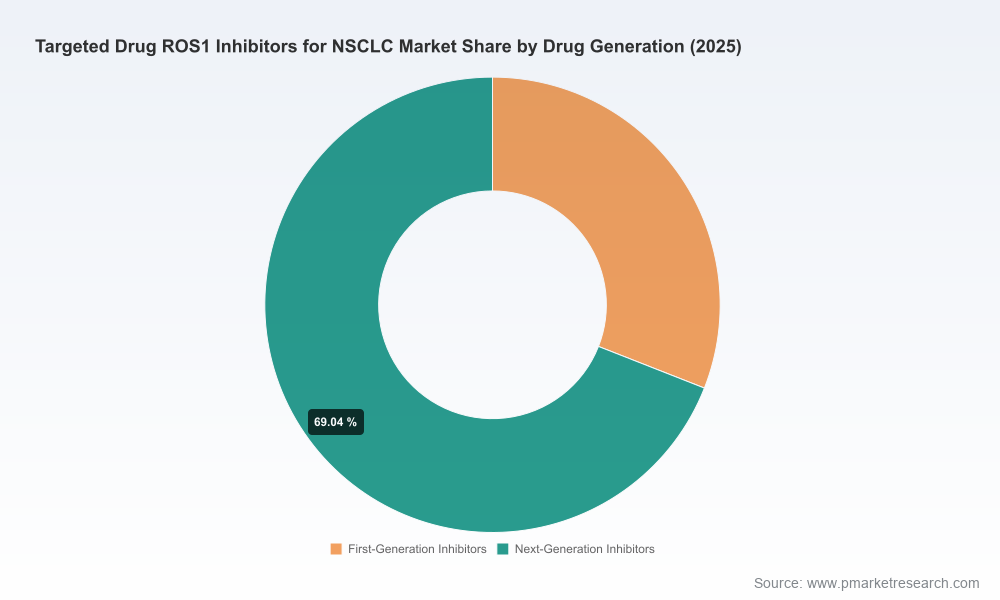

As ROS1-targeted therapies transition from niche innovation to a commercially consequential segment of the non–small cell lung cancer (NSCLC) market, 2026 emerges as a pivotal year for product strategy, market access, and corporate portfolio decisions. Our new PW Consulting market study—covering 2020–2025 historical performance with a 2026–2032 forecast—shows the global ROS1 inhibitors market expanding from roughly USD 655 million in 2025 to an anticipated USD 1.73 billion by 2032, with a compound annual growth rate of 14.85% across the forecast window. This trajectory reflects an accelerating shift toward next-generation inhibitors, label expansions, evolving diagnostic uptake and payer dynamics.

Targeted Drug Ros1 Inhibitors For Nsclc Market

Inflection point timing: The market’s near-term uplift around 2026 creates tight windows for first-mover advantages—whether through launch sequencing, lifecycle management, or licensing deals.

Targeted Drug Ros1 Inhibitors For Nsclc Market

Regulatory momentum and patent clocks intersect: Recent label approvals and upcoming originator patent expirations change the calculus for generics, authorized generics and defensive strategies.

Targeted Drug Ros1 Inhibitors For Nsclc Market

Diagnostics and patient identification: As ROS1 remains a low-prevalence target in NSCLC, commercial success depends on integrated diagnostic-commercial models rather than volume-driven sales alone.

The market’s compound growth of 14.85% through 2032 signals robust uptake beyond incumbent therapies, driven by clinical differentiation and expanded indications. Our study shows a multi-fold increase in addressable revenue from the 2025 base year to 2032, underscoring both the commercial opportunity and the competitive urgency for organizations that want to shape standard of care and reimbursement norms. Importantly, growth is concentrated in a few molecules and geographies, so strategy must be highly targeted rather than broadly diffusionary.

The ROS1 inhibitor field is dominated by a small group of industry leaders and recently consolidated innovators. Key players examined in the report include:

Roche (Basel) — market presence through an established ROS1 inhibitor with ongoing label expansion efforts and strong diagnostics integration. (https://www.roche.com)

Pfizer (New York) — originator of the first approved ROS1-targeted therapy and a global supplier with entrenched clinical guideline inclusion. (https://www.pfizer.com)

AstraZeneca (Cambridge) and Genentech (South San Francisco) — commercialized next-generation agents with regulatory breadth across age cohorts and tumor histologies. (https://www.astrazeneca.com, https://www.gene.com)

Turning Point Therapeutics / Bristol Myers Squibb (San Diego / Princeton) — developer and now commercial steward of a next-generation ROS1 inhibitor that secured key regulatory approvals in 2024; their trajectory illustrates how acquisition can accelerate route-to-market. (https://www.tptherapeutics.com, https://www.bms.com)

Our analysis dissects these players across clinical differentiation, label breadth, commercial infrastructure, diagnostic partnerships and likely responses to patent expiry and generic threats.

Regulatory updates and label expansions: Notable FDA actions through 2023–2024 expanded indications and age coverage for ROS1-targeted therapies, and 2024 approvals materially changed first-line/post-line treatment considerations.

Patent expiry implications: The impending loss of exclusivity for legacy agents alters pricing benchmarks and creates opportunities for authorized generics and competitive discounting strategies.

Diagnostic enablers: Companion diagnostics with regulatory clearance have improved patient identification but also raise requirements for joint go-to-market models with diagnostic vendors.

Clinical evidence pipeline: Ongoing Phase 3 programs remain the primary determinant of continued label expansion and long-term market share shifts; real-world evidence (RWE) will play an increasing role in payer negotiations.

For executives evaluating portfolios, alliances or new investments in 2026, the report identifies five decision levers that will determine commercial outcomes.

Prioritize next-generation differentiation: Clinical attributes that meaningfully improve intracranial control, durability or tolerability will command premium positioning and improved reimbursement prospects.

Prepare for post-patent market structures: Firms must model scenarios for price erosion and channel substitution post-originator patent expiry and decide whether to pursue authorized generics, defensive patent strategies or accelerated label enhancements.

Make diagnostics a commercial partner, not a vendor: Co-funded testing programs, bundled reimbursement proposals and integrated patient-identification pathways materially improve capture rates in a low-prevalence disease.

Invest in evidence that payers value: Head-to-head data, quality-of-life endpoints, and economic models that demonstrate cost-offsets will be decisive in HTA and payer discussions.

Align manufacturing and supply strategies with launch pacing: Given concentrated demand signals and potential surge requirements following label expansions, flexible capacity and contingency sourcing reduce time-to-market risk.

Immediate (0–6 months): complete payer landscape deep dives for priority markets; finalize diagnostic partnership pilots; update pricing dossier to reflect generics scenarios.

Near term (6–12 months): secure regional supply agreements with capacity buffers; commence RWE programs aligned with payer endpoints; prioritize regulatory filings that expand histology-agnostic or pediatric labels where data support it.

Medium term (12–24 months): deploy commercial access teams in markets where HTA timelines align with forecast inflection; execute targeted M&A or licensing to shore up diagnostic or distribution gaps.

Our study is designed to be operationally actionable for 2026 planning cycles. It combines:

Market sizing and high-resolution forecast models (historical 2020–2025; forecast 2026–2032) with scenario modules for alternative clinical and pricing evolutions.

Competitive benchmarking templates that map clinical profiles against commercial levers to reveal realistic share pathways under multiple regulatory outcomes.

Go-to-market playbooks tailored to ROS1’s low-prevalence dynamics—diagnostic bundling, center-of-excellence targeting, key opinion leader (KOL) engagement, and payer negotiation scripts.

HTA and reimbursement trackers with jurisdictional evidence requirements and likely timelines for coverage decisions.

Transaction screens and valuation sensitivities for M&A and licensing, calibrated to forecast demand under differing generic entry timing.

Launch readiness checklists and manufacturing/risk matrices to align clinical, regulatory and commercial stakeholders around execution milestones.

Note: While the report demonstrates the depth and granularity of our analysis, detailed segment-level revenues, regional splits and channel-specific figures are reserved for subscribers and clients who access the full report on our site.

Frame investment decisions against scenario outputs: use the report’s conservative, base, and aggressive forecasts to stress-test ROI for new indications, manufacturing expansions, or acquisitions.

Incorporate market-access simulations into product launch gating criteria so reimbursement preparedness is evaluated alongside safety and efficacy milestones.

Identify acquisition targets not just by pipeline promise but by diagnostic assets and payer relationships that can accelerate patient capture.

Use the competitive playbook to anticipate responses from incumbents: consider defensive filings, strategic discounts or formulary contracting as potential countermeasures.

Clinical risk: negative readouts from pivotal trials or unexpected safety signals can materially alter uptake curves.

Regulatory and reimbursement unpredictability: divergent HTA outcomes across major markets can create fragmented access.

Patent and generic dynamics: timing of originator patent expiry and availability of effective generics will reshape pricing benchmarks rapidly.

Diagnosis rates: failure to scale diagnostic testing limits the effective addressable population and depresses forecast realization.

PW Consulting’s ROS1 inhibitors market study gives decision-makers a practical playbook for 2026—highlighting where to invest, partner, and defend in a market that is growing rapidly but concentrated among a few molecules and players. The combination of strong CAGR and imminent structural events (regulatory approvals, patent expiries, and shifting payer expectations) means that companies that act now—aligning clinical strategy with diagnostics, evidence generation and a realistic commercialization timetable—will be best positioned to capture disproportionate value.

For access to the full data tables, the segmented forecasts, and the downloadable decision-support canvases that underpin these recommendations, please consult the full report on our website. PW Consulting clients receive tailored briefings and a one-on-one workshop to convert insights into executable 2026 plans.

For detailed analysis of this topic, please visit the official page:Targeted Drug Ros1 Inhibitors For Nsclc Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com