Europe Ostomy Devices Market Growth and Future Trends 2025 –2032

Health |

2026-06-25 09:04:51

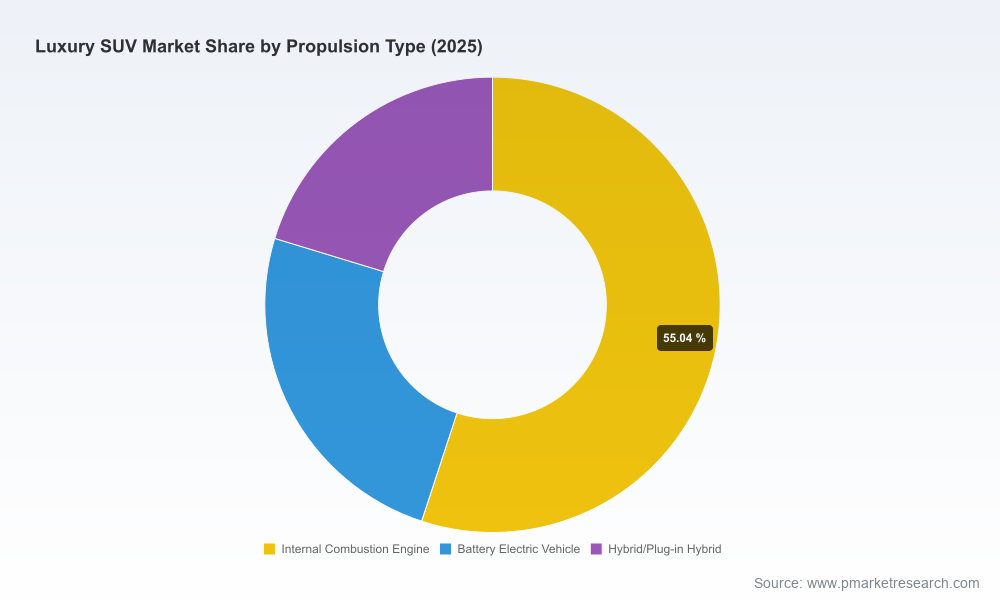

The global luxury SUV market is at an inflection point. After accelerating through the early 2020s, total industry value reached approximately USD 192.4 Billion in 2025 (base year) and, under our central scenario, is projected to expand to roughly USD 329.8 Billion by 2032. This trajectory reflects an underlying compound annual growth rate (CAGR) of about 8.0% across the 2026–2032 forecast period. For senior executives, investors, and strategy teams planning 2026 priorities, the market presents simultaneous opportunities — premium electrification, high-margin model introductions, experiential services — and structural risks driven by regulation, raw-material geopolitics, and changing consumer expectations.

Luxury Suv Market

Timing capital allocation. With a sustained mid-single-digit to high-single-digit growth path, OEMs and suppliers must sequence investments to capture upside while preserving optionality for technology shifts (notably electrification and software-defined features).

Luxury Suv Market

Portfolio prioritization. Luxury OEMs face trade-offs between scaling electrified platforms, expanding ultra-premium bespoke offerings, and protecting combustion-derived margin pools during the transition window.

Luxury Suv Market

Supply-chain resilience. Our analysis highlights how battery raw-material dynamics and evolving regulations will materially affect procurement strategies, inventory policy, and supplier partnerships through 2032.

Competitive positioning. Market concentration is meaningful: the top-tier manufacturers account for the majority of market share by revenue, reinforcing the strategic importance of brand and technical differentiation.

Historical momentum from 2020–2025 set the stage for a structurally larger market in the coming decade. Growth has been underpinned by premiumization, increased household wealth in key urban markets, and a strong appetite for high-specification SUVs that combine utility with luxury. Our forecast conservatively projects continued expansion to 2032, driven by new product cycles, electrification rollouts, and growing acceptance of battery-electric luxury SUVs among affluent buyers.

That said, growth will not be uniform. The interplay between regulatory tightening on CO2 emissions, the declining cost curve for EV battery packs (with several industry forecasts anticipating substantial price falls in the near term), and EU-level recycled-content mandates for batteries from 2031 will create a patchwork of both constraints and enablers for manufacturers. Strategic clarity in 2026 will depend on how firms balance short-term profitability with long-term regulatory compliance and technology investments.

Our competitive review covers established European and North American marques as well as emerging challengers. Key takeaways:

Premium German incumbents remain defensive and offensive simultaneously. BMW Group, Mercedes‑Benz Group AG, and Audi AG continue to invest across mid- and full-size platforms, coupling incremental internal-combustion efficiency with expanded electric model families. Their playbooks emphasize technology integration, performance differentiation, and premium user experience to protect ASPs (average selling prices).

Performance luxury brands (Porsche, Aston Martin, Lamborghini) are leveraging sports-car DNA to command price premiums on high-margin SUVs, while introducing electric derivatives to future-proof the lineup.

British ultra-luxury houses (Rolls‑Royce, Bentley) sustain a bespoke, ultra-premium strategy focused on exclusivity and craftsmanship; their competitive moat is less sensitive to short-term commoditization pressures but faces long-term electrification cost and supply considerations.

Japanese and Korean luxury divisions (Lexus, Genesis) prioritize reliability, hybridization, and high perceived value, using advanced powertrain mixes to appeal to buyers seeking luxury with lower total-cost-of-ownership. Their disciplined pricing strategies are expanding share against legacy premium players.

North American players (Cadillac, Lincoln) are accelerating electrified full-size and flagship SUV entries. Recent near-term developments — including Cadillac’s prepared launches for electric luxury SUVs and OEMs’ high-profile model refreshes — indicate a cross-market push on EV luxury functionality and scale.

New entrants and EV-first brands are moving upmarket with differentiated battery-range claims and unique interior architectures; these entrants compel incumbents to sharpen their technology and customer-experience propositions.

Cadillac has been preparing electric flagship SUVs for market entry, signaling intensified competition in the full-size luxury EV space.

Audi’s next-generation compact luxury SUV refresh (2026) demonstrates continuing investment in platform modularity and powertrain flexibility at lower luxury price tiers.

Lucid’s Gravity launch highlights premium EV challengers’ capability to push technical envelope (range, interior space) and reposition buyer expectations.

BMW’s sustained sales strength in core SUV models confirms brand equity and distribution advantages that remain decisive in luxury segments.

Three external forces will shape strategic choices in 2026 and beyond:

Regulatory thresholds: Upcoming mandates such as recycled-content requirements for batteries impose multi-year lead times for compliance. Firms must integrate regulatory timelines into product-engineering calendars and supplier contracts to avoid retrofit costs late in vehicle lifecycles.

Raw-material dynamics: Continued volatility and geopolitical concentration in critical-mineral processing create significant procurement risk. A strategy emphasizing diversified sourcing, strategic stockpiling, and investments in recycling capability can materially de-risk manufacturing continuity and unit economics.

Battery-cost deflation: Rapid declines in battery-pack costs alter breakeven horizons for EV models. Organizations should run scenario-driven product-margin models to determine optimal timing for conversion of model lines from ICE-dominant to BEV-first architectures.

Our full market study is built for action. Highlights of deliverables: a set of executive-ready strategy frameworks, granular go-to-market playbooks, and implementation tools — including:

Investment-case templates and capex phasing scenarios tailored to luxury SUV portfolios, enabling finance and product teams to stress-test spending plans against multiple electrification and regulation outcomes.

Sourcing and supplier-mapping tools that prioritize critical-mineral exposure and identify high-leverage partners for cell procurement and recycling partnerships.

Demand-shift simulations and price-elasticity models for tiered luxury segments, coupled with marketing activation blueprints for premium EV launches.

Dealer and direct-sales channel strategies that reconcile showroom experiences with digital retailing and subscription-based ownership models.

Competitive playbooks that show where to attack, where to coexist, and where to divest or partner — informed by a detailed study of brand propositions, product pipelines, and recent market moves.

To preserve the strategic value of the dataset for subscribers, the report intentionally withholds the full set of granular regional splits and subsegment revenue tables from this summary. Those datasets, plus an interactive forecast model and supplier-risk heat maps, are available on the report landing page.

Prioritize platform flexibility: accelerate modular platforms that can accept multiple powertrains to hedge between ICE, hybrid, and full-BEV demand paths.

Lock strategic supply: secure long-term battery and component agreements with clauses for recycled-content compliance and price variation mechanisms tied to material indices.

Segment with precision: refine product and pricing ladders so customers clearly understand value differences between compact, mid-size, and full-size luxury offerings while protecting average selling prices.

Invest in software and experience: monetize over-the-air features and subscription services to maintain margins as drivetrain costs transition.

Pursue targeted partnerships and M&A: consider selective bolt-on acquisitions (battery recycling, software stacks, regional distribution) that accelerate capability without diluting brand equity.

Embed regulatory timelines into product roadmaps: ensure future model years meet recycled-content and emissions requirements without costly redesigns.

For boards and executive teams, 2026 is a decision-rich year: the market size and growth trajectory create material upside for firms that time investments correctly, but regulatory shifts and supply-chain exposures create asymmetric downside for the less-prepared. Our full report supplies the empirical foundation and practical toolkits to convert 2026 choices into sustained competitive advantage — from portfolio sequencing and procurement strategy to go-to-market execution and risk mitigation.

Access to the complete data tables, interactive forecast model, and supplier-risk heat maps is available on the report’s source page. For immediate advisory support, custom scenario runs, or an executive briefing tailored to your brand, contact PW Consulting via the report landing page.

For detailed analysis of this topic, please visit the official page:Luxury Suv Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com