CNF Software Market 2026: Strategic Roadmap for Enterprise Decision-Makers

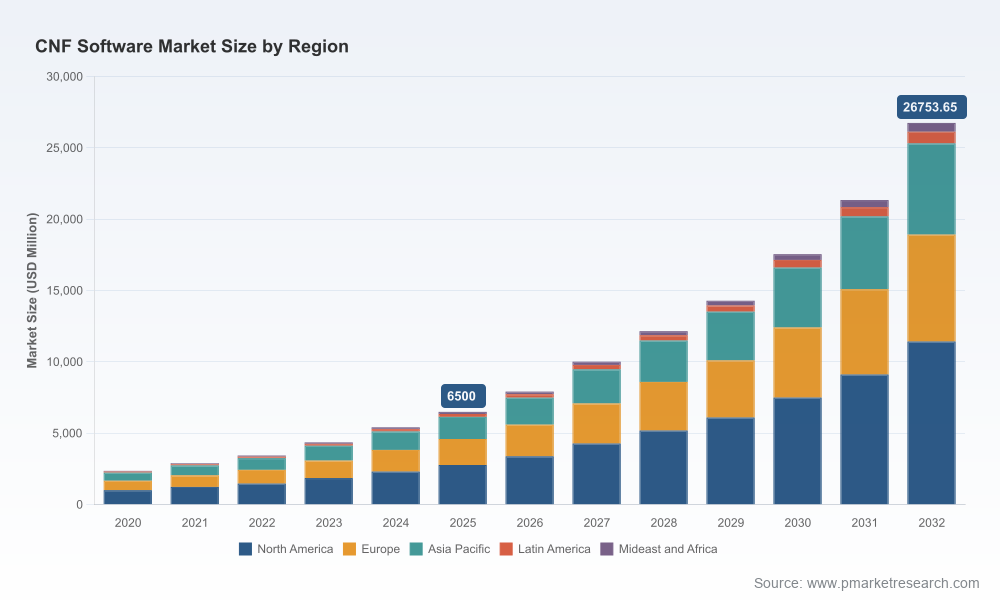

PW Consulting’s latest Cnf Software Market report — base year 2025, forecasting through 2032 — frames cloud-native network functions (CNFs) as a strategic inflection point for service providers, cloud platform operators, and large enterprises planning 5G, edge and cloud transformation programs in 2026. With a compound annual growth rate (CAGR) of 22.4% projected over the forecast horizon, the market trajectory makes CNF strategies a board- and investment-level priority rather than a narrow engineering choice.

Cnf Software Market

Executive snapshot: why this matters in 2026

- Market momentum: The CNF market has moved from early commercial trials into accelerating commercial adoption. Our topline sizing shows a multi-fold increase from the historical period (2020–2025) into the forecast window (2026–2032), underscoring rapid maturation across vendor, operator and cloud ecosystems.

- Strategic leverage: CNFs are now a lever for cost optimization, service velocity and vendor-neutral architectures — critical attributes for telco cloud, enterprise WAN/SD-WAN modernization, and AI-enabled edge services.

- Decision urgency: Capital allocation, partner selection and migration roadmaps drafted in 2026 will determine who captures platform economics and who becomes a legacy integrator over the next business cycle.

Market sizing and growth trajectory

Using 2025 as the report base year, our model integrates vendor disclosures, operator procurement pipelines, platform adoption signals and macro developer trends to produce an end-to-end market view through 2032. The market’s projected CAGR of 22.4% reflects both expansion of new CNF-native services and replacement/modernization of legacy VNFs. This growth is not linear: our scenario analysis highlights an inflection where cloud-native first-mover ecosystems (platforms, validated CNFs, developer communities) accelerate adoption and capture disproportionate share.

Cnf Software Market

For C-level leaders, the implication is clear: planning horizons must accommodate aggressive capex-to-opex shifts, evolving procurement models, and platform-first partnerships. The rapid growth also means that timing matters — delayed entry risks being locked out of platform-driven margins and ecosystem advantages.

Cnf Software Market

Key market dynamics shaping 2026 decisions

- Standards and orchestration parity: CNFs are being deployed within Kubernetes-oriented stacks and mapped into ETSI NFV MANO concepts. Container Infrastructure Service Management (CISM) and Kubernetes-native tooling have reduced integration friction, but telecom-grade requirements (stateful reliability, deterministic performance) still demand vendor-level certification and hardened distributions.

- Developer and skills market: The cloud-native developer population has expanded materially, driving competitive demand for specialized CNF orchestration and observability skills. Hiring and retention pressures will be a near-term operational risk for operators and integrators implementing CNF-based services at scale.

- Cloud/edge economics: Cloud-native design patterns enable more granular edge deployments and higher resource utilization. But economics vary by use case: while some operators will optimize for cost-per-bit, others will prioritize latency or regulatory data residency — each requiring distinct CNF packaging and lifecycle practices.

- Vendor validation and openness: Certification programs and partner validation initiatives are maturing to mitigate integration risk. Open validation frameworks and third-party CNF certification are becoming decisive procurement levers that accelerate deployment readiness.

Competitive landscape — who matters and why

The CNF ecosystem now blends incumbent network vendors, cloud-native pioneers and platform integrators. Market concentration is moderate: the top three vendors account for a significant but not dominant share, and the top five represent a clear leader tier — a structure that supports both scale and competition.

- Nokia (Espoo, Finland) — Nokia has positioned cloud-native packet core offerings and a Cloud Native Communication Suite designed as disaggregated CNFs optimized for Kubernetes. Their contributions to cloud-native standards and partner validations help reduce operator risk in 5G core transformations. (https://www.nokia.com)

- Ericsson (Stockholm, Sweden) — Ericsson’s Cloud Native Infrastructure Solution (CNIS) and dual-mode 5G Core investments, combined with an expanded third-party CNF certification program, are signaling an ecosystem play: platform openness plus curated validation to accelerate operator-grade deployments. (https://www.ericsson.com)

- F5 (Seattle, USA) — F5’s BIG-IP Next CNF family targets advanced traffic management, security and DPU-accelerated data planes for edge and 5G, emphasizing performance-optimized datapath acceleration and subscriber-aware policy functions. Recent releases and NVIDIA DPU integrations highlight a focus on AI edge and high-throughput service planes. (https://www.f5.com)

- Cisco (San Jose, USA) — Cisco extends its networking leadership into CNFs with containerized routing and mobile core functions, leveraging its installed base and systems integration capabilities to offer path-to-production solutions for large operators. (https://www.cisco.com)

- Ribbon Communications (Plano, USA) — Ribbon is converting classical session and IMS capabilities into cloud-native SBCs and policy functions, targeting operators needing migration paths with protocol fidelity and signaling maturity. (https://ribboncommunications.com)

- Titan.ium Platform (Canada) — A specialist in cloud-native signaling, routing and subscriber data M&S, this vendor focuses on microservices-first CNFs designed for 5G service stacks and rapid time-to-market. (https://titaniumplatform.com)

- Red Hat (Raleigh, USA) — As a leading platform provider via OpenShift, Red Hat is central to validated CNF deployments; its partner validations with vendors such as Nokia, Ericsson and F5 reduce operator integration risk in Kubernetes environments. (https://www.redhat.com)

Recent ecosystem moves underline competitive priorities: F5’s mid-2026 product and partnership announcements emphasize dataplane acceleration and AI edge readiness; Ericsson’s expanded certification program (early 2026) signals that vendor neutrality and third-party validation are now procurement differentiators; CNCF’s Q1 2026 reporting highlights an expanding developer base supporting telecom cloud projects. These signals should inform 2026 vendor selection criteria, partnership roadmaps and R&D investment priorities.

Practical content in the PW Consulting report

This report is purpose-built for decision-makers who must translate CNF market momentum into executable plans. It contains hands-on, actionable deliverables including:

- Operational playbooks for CNF onboarding, validation and lifecycle management that bridge engineering and procurement workflows.

- Procurement frameworks and RFP templates tailored for CNF-first contracts, including certification checklists and integration SLAs.

- Migration blueprints showing phased replacement of legacy VNFs with CNFs, including risk controls, rollback criteria and operator acceptance testing (OAT) matrices.

- Go-to-market and pricing playbooks for MSPs and cloud providers looking to monetize CNF-based services at the edge and in core networks.

- Financial models and TCO comparators that quantify capital and operational impacts across deployment flavors (public, private and hybrid clouds), together with sensitivity analyses for developer labor and DPU-enabled hardware costs.

- Vendor profiles and benchmarking (functional, performance and certification readiness) with blinded scorecards to support shortlisting without exposing proprietary customer data.

How to use these insights in 2026 planning cycles

- Board strategy: Use the market trajectory and concentration data to reassess platform bets, partnership investments and M&A targets — especially where scale or validated cloud-native capabilities are strategic differentiators.

- CTO roadmap: Prioritize tooling for observable, Kubernetes-native lifecycle management and hardened CI/CD pipelines. Mandate third-party certification as a procurement precondition for production CNFs.

- CFO focus: Re-evaluate capital allocation to favor platforms and software subscriptions that unlock recurring revenue or predictable Opex improvements; incorporate sensitivity to skilled labor inflation in financial planning.

- Commercial teams: Design bundled offers (connectivity + CNF-enabled edge services) that leverage platform integrations and validated partner stacks to shorten sales cycles.

Limitations and where to find the full data

This release is a strategic preview intended to equip executives with the arguments and decision frameworks needed in 2026. To preserve proprietary analytical value and encourage direct engagement, granular segmentation numbers (detailed regional and application splits, contractual-level vendor shares and underlying transaction-level datasets) are withheld from this summary. The full report contains the complete model, interactive scenario tools, and downloadable scorecards that power the conclusions summarized here.

Next steps and call to action

Executives preparing budgets, procurement strategies or platform partnerships for 2026 should request the full PW Consulting Cnf Software Market report to access: the full financial model, vendor and certification matrices, TCO calculators and bespoke advisory sessions. For immediate tactical guidance, our consulting teams are available to run a 90-day CNF readiness assessment tailored to your network topology, service portfolio and commercial objectives.

PW Consulting’s work combines market economics, deep technical validation and pragmatic go-to-market playbooks. In a market expanding at an annualized pace north of 20%, early alignment between strategy, engineering and procurement is the decisive factor separating platform winners from laggards. The full report provides the data and execution tools to make that alignment concrete.

For detailed analysis of this topic, please visit the official page:Cnf Software Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com