Haxhi Ali Cave – Albania’s Most Impressive Sea Cave Experience

Other |

2026-02-11 15:48:23

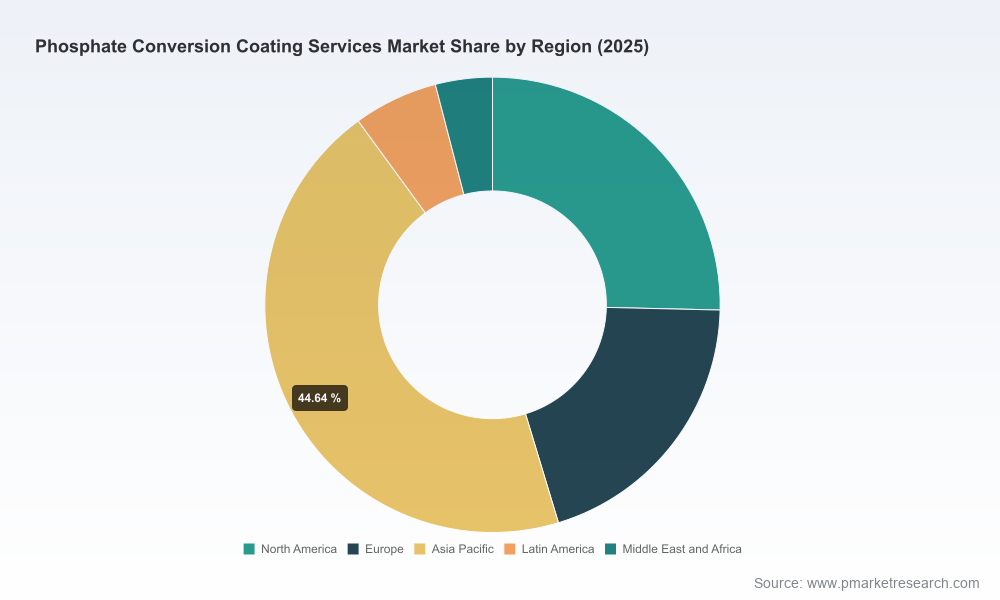

PW Consulting’s latest market study on Phosphate Conversion Coating Services (base year 2025; historical 2020–2025; forecast 2026–2032) provides a concise, decision-grade view of an industry at the crossroads of regulatory pressure, materials-cost volatility, and accelerating end-market requirements. The market, measured in USD Million, recovered to an estimated 650.0 Million in 2025 after short-term fluctuations during 2023–2024, and is projected to grow through the 2026–2032 forecast window at a compound annual growth rate (CAGR) of 4.5% toward a high‑single‑hundreds‑Million market by 2032.

Phosphate Conversion Coating Services Market

This briefing highlights the strategic implications for executives planning capital allocation, supply-chain strategy, and technology adoption in 2026 — showing where the opportunity and risk concentrations lie while withholding the full segment-level tables that are reserved for the full report.

Phosphate Conversion Coating Services Market

Resilience with selective volatility: After steady growth from 2020 to mid‑2023, the market experienced a modest contraction in 2024 followed by a stronger-than-expected recovery in 2025. That pattern signals durability in demand (especially from automotive, aerospace, and industrial maintenance sectors) but heightened sensitivity to short-term industrial cycles and raw-material swings.

Phosphate Conversion Coating Services Market

Sustained, moderate expansion: At a 4.5% CAGR across 2026–2032, the segment is not a hyper-growth market but offers predictable expansion that supports targeted investments — particularly in process efficiency, regulatory-compliant chemistries, and service differentiation.

Fragmentation and consolidation signals: Market concentration metrics show that the top three and five providers account for a minority share of overall revenue, indicating opportunities for regional scale plays, consolidation, and capability-driven differentiation rather than winner-take-most dynamics.

Capital allocation: With moderate CAGR and predictable demand pockets, capital should prioritize flexible, modular finishing lines and retrofit investments (e.g., low‑temperature, no‑rinse processes) that reduce unit cost and environmental footprint rather than large single-site greenfield builds.

Regulatory preparedness as competitive advantage: EPA and REACH-driven rules are accelerating adoption of low‑zinc, no‑rinse, and reduced-sludge chemistries. Early adoption of these technologies not only reduces compliance risk but is increasingly a procurement requirement for OEMs in automotive and aerospace supply chains.

Supply‑chain risk management: Raw-material pricing volatility—illustrated by regional phosphoric acid price differentials—is a near-term input cost driver. Hedging, supplier diversification, and vendor partnerships for material recycling/sludge minimization will be core to margin resilience in 2026.

Service-led differentiation: As the market remains fragmented, providers that bundle finishing with engineering support (e.g., process qualification to MIL/AMS standards, rapid prototyping, and coating performance verification) can capture higher-value, recurring revenue from OEMs and defense contractors.

The full PW Consulting report is structured to move executives from insight to action. Key, actionable modules include:

Market sizing and trend analysis (historical and forecast), with scenario-driven forecasts tailored to raw‑material and regulatory outcomes.

Segment playbooks that evaluate the attractiveness and growth levers of regional footprints, coating chemistries, and end-market verticals — each with strategic options for customer targeting and price/volume sensitivity models.

Cost-and-margin heatmaps that highlight input-cost exposure (phosphoric acid, zinc compounds, energy) and identify where process investments can unlock margin expansion.

Technology and compliance roadmap assessing low‑zinc, phosphate‑free alternatives, no‑rinse chemistries, and sludge‑minimization techniques, plus timelines for regulatory impact and adoption.

Vendor benchmarking and M&A orientation: a vendor scorecard (service capability, quality certifications, scale, and geographic reach) and a short list of plausible consolidation targets by strategic fit.

Implementation playbooks with KPIs for plant upgrades, pilot programs, supplier contracts, and commercial pilot offers to OEMs.

Note: This public briefing intentionally omits full tables and specific segment-level revenue splits; those are available in the licensed report for executives and procurement teams requiring transaction- and investment-level detail.

The competitive map comprises specialized, regional, and full-service metal finishing providers. Key dynamics include capability-led niche plays (e.g., military-grade specs and large-tank capacity), full-service finishing with integrated workflows, and product-led disruption from formulators.

Nitretex (United States) — Known for large-tank zinc and manganese phosphate services, with capacity to handle line-of-production volumes and custom parts. Their strength is operational scale for high-throughput segments (oil & gas, automotive); strategic move: pursue OEM partnerships where tank size and throughput drive procurement decisions.

Keystone Corporation (United States) — Specializes in manganese phosphate and military/industrial spec processing (e.g., MIL‑DTL‑16232, AMS 2481). Their advantage is specification compliance for bearings and high-wear parts; strategic move: align with defense primes and tier‑1 suppliers for recurring contracts.

K&L Plating (Lancaster, PA) — Focused on zinc phosphate for defense and manufacturing markets, providing a base for organic coatings. Strategic move: expand value-added testing and qualification services to deepen lock-in with defense contractors.

Cor‑Pro Systems (Houston, TX) — Deep vertical focus on Gulf Coast petrochemical and refinery clients where long-term corrosion protection is mission-critical. Strategic move: tailor service bundles that address turnarounds and site‑specific environmental constraints.

Imagineering Finishing Technologies & Valence Surface Technologies — Both bring full-service finishing and aerospace/defense capability. Their differentiator is integrated pre- and post-phosphate treatment workflows; strategic move: cross-sell certification and component-level traceability to OEMs requiring supply-chain transparency.

Pioneer Metal Finishing — Concentrates on manganese phosphate for wear resistance in drivetrain and fastener applications. Strategic move: target aftermarket and remanufacturing channels where high-wear replacement demand is stable.

Recent supplier-side developments underscore the competitive inflection points: Henkel’s mid-2024 introduction of a single-step cleaner and phosphate‑free coater (and its 2025 trade-show showcases) illustrate that formulators are actively offering process-simplifying alternatives. These product innovations compress processing time and reduce sludge/chemical handling — an existential challenge to traditional multi-step phosphate processes if OEM acceptance accelerates.

Raw-material exposure: Phosphoric acid shows notable regional price variance (e.g., North America vs. Europe vs. Africa), which can shift supplier margins and create regional cost advantages or pressures.

Regulatory tightening: Accelerating EPA/REACH focus on sludge and heavy metals increases compliance costs and raises the bar for process modernization; laggard operators may face steep remediation or exit decisions.

Technological substitution: Growth of low‑zinc or phosphate‑free pretreatments may create stranded investments for operators with legacy process footprints unless they plan staged upgrades.

Service differentiation fatigue: As basic corrosion and adhesion requirements become table-stakes, providers that do not layer testing, qualification, or engineering services will see margin compression.

90 days — Rapid diagnostics: Run a focused cost‑to‑serve and input‑exposure audit across plants. Identify contracts vulnerable to price pass-through limitations and prioritize hedging or supplier contracts for phosphoric acid and zinc salts.

180 days — Pilot and partner: Launch pilot lines for low‑zinc/no‑rinse and phosphate‑free chemistries with lead OEMs; partner with formulators or testing labs to accelerate qualification to relevant MIL/AMS standards.

360 days — Capacity and M&A play: Consolidate regional footprints where scale yields processing-cost advantages and pursue bolt-on acquisitions that add capabilities (large‑tank capacity, MIL spec processing, full‑service finishing) to create defensible, integrated offers.

For boards, investors, and operating executives making 2026 allocations, the PW Consulting report is built to translate market trajectory, regulatory direction, and vendor capability into executable plans. The industry is neither commodity-trapped nor runaway hyper-growth: it rewards targeted investment in process modernization, regulatory alignment, and service differentiation. The full report contains the granular segmentation, vendor scorecards, financial proxies, and implementation templates needed to convert these strategic directions into measurable outcomes.

To access the complete analysis, detailed segment tables, and provider benchmarking necessary for transactional decisions, please refer to PW Consulting’s full Phosphate Conversion Coating Services Market report on our website or contact your PW Consulting account lead for licensing and enterprise distribution options.

For detailed analysis of this topic, please visit the official page:Phosphate Conversion Coating Services Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com