Best PVC Wall Panels for Homes & Offices – Affordable & Waterproof Solutions

Other |

2026-04-06 02:34:56

As pharmaceutical, biotech and academic stakeholders ready their 2026 plans, the primary cell culture market is emerging as both a high-growth opportunity and a strategic risk pool. PW Consulting’s latest market study — grounded in five years of historical data and a seven-year forecast horizon — synthesizes quantitative market trajectories with actionable playbooks for procurement, R&D, supply chain and M&A decisions. This release presents the study’s strategic highlights and explains why the market’s structural dynamics must shape corporate strategy heading into 2026. For full subsegment tables, granular regional splits and proprietary price models, please visit the report landing page.

Primary Cell Culture Market

Between 2020 and 2025 the global primary cell culture market expanded markedly, moving from approximately USD 3.85 billion to roughly USD 6.85 billion (USD Million units). Our base-year analysis (2025) captures a market that is already mature in capability but rapidly evolving in commercial scale. From 2026 through 2032 we project a compound annual growth rate of 12.5%, taking overall market value to an estimated USD 15.63 billion by 2032 — a near-doubling over seven years that underscores sustained demand across drug discovery, regenerative medicine and translational research.

Primary Cell Culture Market

Market concentration metrics highlight a moderately consolidated supplier landscape: the top three players account for approximately 38.5% of revenue, while the top five control over half of the market (about 52.3%). This structure creates pronounced advantages for established suppliers in distribution, quality assurance and regulatory trust, while leaving room for specialist entrants to capture high-value niches.

Primary Cell Culture Market

Actionable market-sizing and forecasting (2020–2032) with scenario runs that stress-test demand under alternative regulatory and reimbursement pathways.

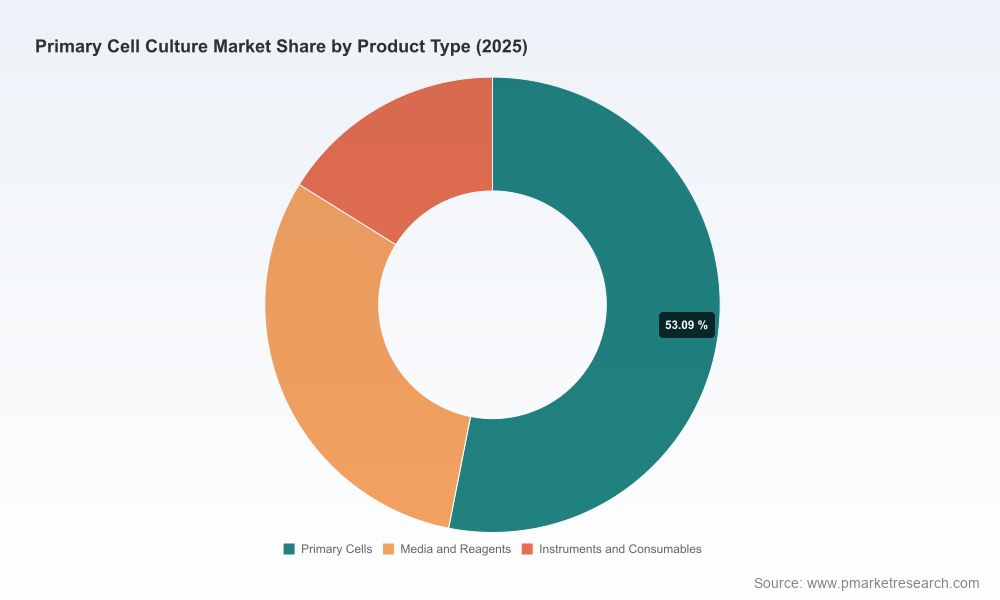

Commercial segmentation frameworks (product categories, applications and distribution channels) mapped to buyer personas and procurement cycles — presented as decision matrices that buyers and suppliers can deploy for budgeting and negotiations. Note: detailed subsegment figures and regional allocations are reserved for the full report to preserve competitive insight.

Supply-chain resilience playbook that quantifies exposure to key raw material volatility (including serum markets), logistics constraints, and regulatory export controls, with mitigation options ranked by cost/benefit.

Regulatory and reimbursement impact models that translate recent policy shifts into revenue and time-to-market implications for cell-based assays and primary-cell-enabled platforms.

Due-diligence templates and valuation heuristics for M&A or JV activity in primary cells, including customer concentration, IP leverage and integration risk assessments.

Vendor benchmarking templates and procurement negotiation scripts calibrated to market concentration and supplier capabilities.

The market’s competitive topology is shaped by a set of global incumbents and agile specialists. Leading life-science suppliers remain influential through recognized quality standards, certified product lines and broad distribution networks. Key players profiled in our study include Thermo Fisher Scientific, Lonza, Merck KGaA (Sigma-Aldrich), ATCC, Sartorius (PromoCell), and a cadre of specialized suppliers such as ScienCell, Celprogen, AcceGen and BioIVT.

Thermo Fisher Scientific: Leveraging its Gibco portfolio and broad service ecosystem, the company continues to set technical and logistical benchmarks for primary cells used in drug discovery and toxicology. Recent product expansion (mid‑2024) into lung fibroblasts and alveolar epithelial cells signals continued investment in respiratory and immuno-oncology toolkits.

Lonza: Known for cryopreservation and scale capabilities, Lonza’s catalog updates indicate a focus on donor-matched offerings and consistency for translational programs — a competitive advantage for biotechs running IND-enabling studies.

Merck KGaA (Sigma-Aldrich) and ATCC: These vendors play critical roles in authenticated cell sourcing, quality certification and distributor networks that matter to compliance-focused buyers.

Sartorius (PromoCell) and others: Specialists are winning share in defined niches — e.g., serum-free media, endothelial/epithelial primary lines, and certified manufacturing lanes (Sartorius’ ISO 13485 certification is emblematic).

Small and regional players: Companies such as ScienCell, Celprogen, AcceGen and BioIVT differentiate on catalog depth (e.g., tissue-specific offerings), advanced culture formats (3D scaffolds), and metabolically competent hepatocyte platforms for ADME work.

Recent vendor developments in the last 18 months — catalog expansions, certification updates and trade-show product rollouts — are consistent with a market investing heavily in both breadth and compliance. Buyers should treat vendor roadmaps as a leading indicator of where assay and model adoption will accelerate in 2026.

Regulatory trend: The FDA’s 2023 guidance emphasizing primary cell models for IND-enabling safety studies, particularly in oncology, is shifting internal R&D decisions away from surrogate models and toward primary-cell-based platforms. Organizations that align 2026 pipeline milestones with this guidance will realize shorter regulatory friction and more rigorous preclinical packages.

Reimbursement and trial coverage: CMS updates in 2024 that adjusted coverage for primary-cell-based assays in early clinical testing change the economics of high-cost, high-fidelity assays — making them more accessible within Phase I programs.

Raw material pressure: Serum markets were disrupted in 2024 with notable price increases tied to supply constraints and regulatory pressures. Procurement strategies that assume elevated input cost and build multi-source contracts will mitigate margin compression.

Export controls and supply chain policy: Tighter controls on cross-border transfers of human primary cells in certain jurisdictions increase compliance costs and may favor suppliers with localized manufacturing or robust export licenses.

Public funding: Significant public investment (e.g., NIH allocations for organ-on-chip technologies) is accelerating demand for primary-cell-enabled platforms in translational and replacement technologies, creating new commercial pathways for suppliers and collaborative opportunities for buyers.

Below are prioritized actions PW Consulting recommends to executive teams preparing 2026 budgets and programs. Each recommendation maps to tangible operational adjustments and expected strategic impact.

Align R&D portfolios with regulatory expectations: Prioritize primary-cell models for IND-enabling oncology assets where FDA guidance creates clearer submission pathways. Impact: reduced preclinical rework and more defensible safety packages.

Reassess procurement and supplier risk: Move from single-source contracts to tiered supply frameworks that include both global incumbents and vetted regional specialists, with contingency stockpiles for critical reagents such as serum. Impact: lowered disruption risk and improved cost visibility.

Invest in in-house capabilities selectively: For large biopharma, developing internal primary-cell banks for high-use cell types can reduce long-term costs and insulate from export controls — but only when anchored to high-volume programs. PW Consulting’s ROI models can help determine breakpoints.

Adopt certification and traceability standards: Require ISO and quality certifications in supplier RFPs. Certification reduces downstream compliance risk and accelerates adoption by regulatory reviewers.

Targeted M&A and partnerships: For mid-sized firms, consider bolt-on acquisitions of high-quality cell suppliers or platform providers to capture margin and technical differentiation. Use our due‑diligence templates to protect against hidden liabilities (donor consent, chain-of-custody, and export restrictions).

Commercialize adjacency services: Suppliers should bundle culture media and validated protocols with cells, and offer assay-qualification services that lock in recurring revenue and raise switching costs.

Our report is designed as a working tool — not a static document. Clients receive editable financial models, procurement negotiation playbooks and integration checklists tailored to their role (buyer, supplier, investor). We also offer scenario workshops that stress-test 2026 plans against regulatory shocks, raw-material price spikes, and accelerated public funding into organ-on-chip and regenerative medicine platforms.

PW Consulting’s diagnostics are particularly useful for:

Biopharma portfolio managers who must prioritize programs requiring primary-cell data to meet regulatory expectations.

Procurement teams seeking to craft resilient sourcing strategies and defend margins amid input-price volatility.

Investment teams evaluating strategic M&A targets or partnership opportunities in the primary cell value chain.

The combination of robust market expansion (12.5% CAGR projected 2026–2032), meaningful concentration among incumbents, regulatory momentum, and material cost volatility makes 2026 a year when tactical choices will compound into lasting strategic advantage or avoidable exposure. PW Consulting’s market study delivers the quantitative runway and the operational playbooks to convert market growth into sustainable enterprise value — while intentionally withholding proprietary subsegment detail here to ensure our clients derive exclusive, actionable advantage.

To access the full data tables, regional and application-level breakouts, vendor scorecards, and customizable scenario models, consult the PW Consulting report page or contact our advisory desk to schedule a briefing tailored to your organization’s 2026 priorities.

For detailed analysis of this topic, please visit the official page:Primary Cell Culture Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com