Diagnostic Catheter Market Overview: Key Drivers and Challenges

Other |

2026-04-28 05:52:09

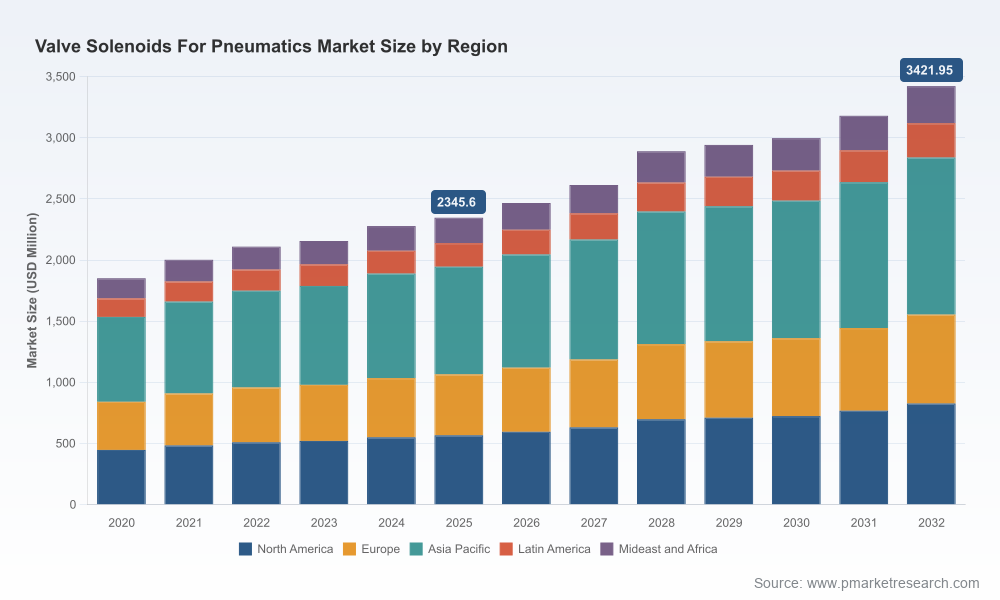

PW Consulting’s newest market research briefing synthesizes five years of historical performance and a forward-looking seven‑year forecast to equip corporate leaders with the actionable intelligence required for decisive 2026 strategy. The global valve solenoids for pneumatics market expanded from roughly USD 1,850.8 Million in 2020 to USD 2,345.6 Million in 2025. Our baseline forecast anticipates continued growth at a compound annual growth rate (CAGR) of 5.45% through 2032, taking the market toward approximately USD 3,421.9 Million by the end of the forecast window. This briefing explains why those headline metrics matter, how competitive and regulatory forces are reshaping supplier economics, and what concrete moves procurement, R&D and corporate development teams should prioritize in 2026.

Valve Solenoids For Pneumatics Market

Macro clarity: A reliable, audited view of market scale and trajectory removes guesswork from capacity planning, capex allocation and revenue targets for 2026–2027.

Valve Solenoids For Pneumatics Market

Risk-aware sourcing: The report maps the supplier ecosystem and raw‑material sensitivities that underlie lead‑time volatility and margin pressure for stainless‑steel bodies and high‑grade sealing materials.

Valve Solenoids For Pneumatics Market

Compliance-first product strategy: New and evolving safety and cybersecurity expectations (IEC 61511, ISA/IEC 62443) are converging with long‑standing interchangeability standards (ISO 5599/1), creating both barriers to entry and premium positioning opportunities.

Commercial signal: Our competitive benchmarking identifies how incumbents balance platform breadth with niche specialization—critical input when assessing M&A targets, co‑development partners or technology acquisitions.

Market sizing and validated forecasts (2020–2032) with scenario analysis reflecting supply‑side shocks and regulatory ramp rates.

Product and technology playbooks: design tradeoffs between direct‑acting and pilot‑operated architectures, low‑power coil options, manifold integration strategies, and materials selection for corrosive or hygienic environments.

Regulatory and standards impact assessment covering IEC 61511, ISA/IEC 62443 and ISO 5599/1 — with certification timelines and recommended product compliance roadmaps.

Competitive benchmarking and supplier capability matrix, including CR3 and CR5 concentration analysis and go‑to‑market models for tier‑1 and specialist vendors.

Procurement playbook: dual sourcing templates, inventory buffers calibrated by lead‑time volatility, and supplier KPI metrics for long‑term contracts.

M&A and partnership screening: scorecards and financial thresholds tuned to the sector’s margin profile and consolidation dynamics.

Commercial case studies and 12‑month tactical roadmaps for OEMs, contract manufacturers and aftermarket service providers.

Market concentration: The sector exhibits moderate concentration (CR3 and CR5 metrics indicate leading groups capture a meaningful but not dominant share). This profile favors both scale plays (to win large automation OEM contracts) and focused specialists (to capture higher margin niches such as hazardous‑location or ultra‑fast actuation).

Global OEMs (examples): Companies like MAC Valves, Festo, SMC and Parker Hannifin continue to compete on breadth, system integration capability and channel reach. Their strengths are in product completeness—directional valves, manifold systems, balanced poppet and high‑flow designs—and in established relationships with automation integrators.

Process and high‑reliability players (examples): Emerson (ASCO) and other process‑oriented manufacturers are differentiating on robustness for industrial and process applications, with product lines tuned for harsh environments and high‑cycle requirements.

Specialists and custom suppliers: Smaller firms such as Solenoid Solutions, Magnet‑Schultz and Humphrey Products focus on configurable direct‑acting valves, rapid prototyping and customer‑specific manifolds—an attractive profile for OEMs seeking differentiation or faster time‑to‑market.

Recent product actions to watch: Festo’s 2025 catalog refresh underscores a push to consolidate system-level messaging and simplify specification; new compact direct‑acting launches from niche vendors point to sustained demand for space‑constrained solutions; Emerson’s prior product refreshes signal a continued emphasis on energy efficiency and flow optimization.

Standards and safety: Adoption of safety‑instrumented-system requirements and cybersecurity expectations means suppliers must deliver validated diagnostics, fail‑safe configurations and secure connectivity options for IIoT‑enabled valves. Buyers in 2026 will favor vendors that can demonstrate documented compliance rather than those promising retrofit solutions without evidence.

Materials & reliability: Stainless steel bodies and high‑grade seals remain standard in demanding environments; sourcing and qualification of these materials materially affects TCO and warranty exposure.

System integration: Customers increasingly demand valves as part of integrated control modules (manifolds + electronics + diagnostics), shifting value capture toward vendors who can offer plug‑and‑play solutions.

Cost and energy: Low‑power coils and flow‑optimized valve geometries are becoming procurement differentiators as factories seek energy reductions and lower lifecycle costs.

Channel evolution: Distribution partners are evolving into solution sellers—providing configuration, local certification and aftermarket support—creating opportunities for manufacturers to co‑invest in partner enablement.

Prioritize qualification for safety and cybersecurity standards now — delays create sales friction with cautious automation buyers.

Invest in modular manifold platforms that support both direct‑acting and pilot‑operated modules; this reduces SKU complexity while addressing diverse OEM needs.

Secure dual‑source agreements for critical stainless steels and elastomer compounds, and include rights to audit sub‑tier suppliers to manage quality and lead times.

Differentiate through diagnostics: embed low‑latency status reporting and basic self‑test capabilities to command premium positioning in retrofit and greenfield projects.

Use selective M&A to accelerate capability gaps—target specialists with field‑proven manifold integration, hazardous‑location certifications or proprietary fast‑actuation geometries.

Build distributor enablement programs (training, demo kits, local certification support) to turn channel partners into growth multipliers.

Adopt value‑based pricing for energy‑saving and safety‑certified products; quantify lifecycle savings in commercial proposals to overcome initial price resistance.

PW Consulting’s Valve Solenoids For Pneumatics Market report is designed as an operational tool for leadership, not just a desk reference. We combine bottom‑up market reconstructions, supplier financial and capability analysis, and practical toolkits—procurement templates, product roadmaps and M&A scorecards—so teams can move from insight to execution within 90 days. Our advisory package includes a tailored 2‑week workshop to translate market scenarios into a company‑specific 12‑month plan for product, procurement and commercial teams.

This briefing highlights the strategic contours you need to act with confidence in 2026. For access to the full dataset (including segmented demand forecasts, supplier scorecards, and granular pricing benchmarks) and to schedule a briefing with our industry team, please visit the report page. Core sub‑segment tables and proprietary benchmarks are available to subscribers and advisory clients only—request access to unlock the detailed inputs that underpin the headline forecasts referenced above.

Methodological note: Base year = 2025; historical window = 2020–2025; forecast = 2026–2032; currency = USD (revenue in Millions); forecast CAGR = 5.45% (compound, baseline scenario).

For detailed analysis of this topic, please visit the official page:Valve Solenoids For Pneumatics Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com