Nickel Electrode Plate Market: Insights and Competitive Analysis

Other |

2026-04-08 06:01:09

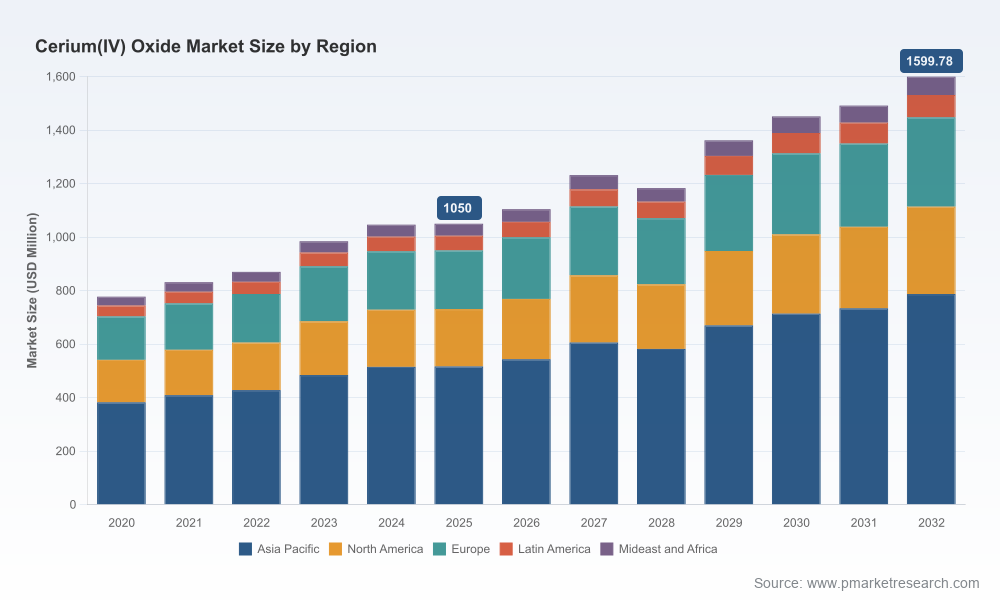

PW Consulting’s latest Cerium(IV) Oxide Market report (base year 2025) distills five years of historical performance (2020–2025) and delivers a forward-looking, actionable roadmap for 2026–2032. Our analysis shows the global Cerium(IV) Oxide market expanding from an estimated USD 1,050.0 Million in 2025 to approximately USD 1,599.8 Million by 2032, reflecting a compound annual growth rate (CAGR) of 6.2% across the forecast horizon. For executives planning near-term capital allocation, supply‑chain repositioning, or M&A activity, the report translates these macro trajectories into pragmatic go/no‑go decision points, scenario-tested supply risk matrices, and commercially executable playbooks.

Ceriumiv Oxide Market

2026 is a pivot year for players across the Cerium(IV) Oxide value chain. Demand drivers that were once incremental—advanced polishing for semiconductors, stricter vehicle emissions standards, and performance additives for glass and ceramics—are maturing into backbone markets. At the same time, supply dynamics are being reshaped by policy and capacity moves that create short windows of strategic advantage. Our report equips leaders with the intelligence necessary to convert market momentum into durable competitive advantage without exposing the granular segment-by-segment figures that are reserved for subscribers.

Ceriumiv Oxide Market

Two major structural developments have changed the playing field. First, export control measures targeting rare earth separation technologies have tightened cross‑border flows of advanced processing know‑how. Second, capacity additions in nontraditional producing regions have begun to alter long‑term supply elasticities. These dynamics are compounded by trade instruments—such as additional tariffs on certain imports to the U.S.—and environmental enforcement actions affecting mining and feedstock availability in some jurisdictions.

Ceriumiv Oxide Market

Operationally, that means procurement teams must move from price‑only strategies to capability‑aware sourcing: locking in secured access to processed cerium streams, negotiating technology‑protected tolling arrangements, and assessing the cost/benefit of vertical integration versus strategic partnerships.

Spot and contract pricing have been influenced by abundant light rare earth concentrates in some regions and constrained processing capacity in others. Historical reference points—like the 2023 FOB price benchmark for standard cerium oxide—underscore how low unit commodity prices can coexist with elevated processing premiums for high‑purity grades. For buyers and sellers, the critical takeaway is that feedstock volatility can be decoupled from finished‑goods margin volatility when firms actively manage conversion and technical yield risk.

The Cerium(IV) Oxide market presents a mix of specialized producers, chemicals majors, and regional industrial suppliers. Market concentration is meaningful enough to shape pricing and technology diffusion: the top three players account for a significant share of global commercial supply, while the top five widen that influence. This creates distinct strategic roles for market participants:

Our competitive profiles cover firms across all these archetypes—detailing capabilities, geographic reach, product portfolios, and strategic intent—so that commercial teams can calibrate partnership, procurement, and M&A approaches against credible business models.

Beyond headline market numbers, the report is designed as a toolkit for 2026 decision cycles. Key deliverables include:

Executives should treat the coming year as a decision window rather than a planning inertia trap. Our recommended priority actions:

Procurement teams can use our supplier maps and risk scores to renegotiate terms this quarter. R&D and product leaders will find the product‑spec‑to‑revenue impact models useful when prioritizing higher‑purity programs. Corporate development teams can apply our valuation comparators and deal‑screen templates to accelerate diligence and reduce time‑to‑offer. Importantly, each of these tools ties back to market scenarios that show when to escalate from pilot partnerships to full‑scale investments.

PW Consulting’s analysis provides audited macro market sizing (historical 2020–2025 and forecast 2026–2032), concentration metrics, and scenario outputs. In keeping with our “trailer” principle, we present robust, verifiable high‑level insights here to inform executive thinking while reserving the granular segment breakouts, supplier revenue shares, and custom sensitivity tables for the full report and client workshops. This approach preserves the commercial value of in‑depth segment data and incentivizes direct engagement for transaction‑grade intelligence.

For leaders ready to convert insight into action in 2026, PW Consulting offers three immediate engagement paths:

To request the full report or arrange a briefing, visit the PW Consulting research portal. In an environment where policy shifts and targeted capacity investments can redraw competitive boundaries within months, having validated forecasts, supplier intelligence, and executable playbooks ready at the start of 2026 will be the competitive advantage that separates resilient operators from reactive ones.

PW Consulting is a strategy and industry analytics firm specializing in critical materials and advanced chemicals. Our market studies combine proprietary primary research, regulatory tracking, and scenario‑based financial modelling to support corporate strategy, commercial negotiations, and M&A execution.

For detailed analysis of this topic, please visit the official page:Ceriumiv Oxide Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com