Polypropylene Market Market Drivers, Innovation Pipelines and Forecast to 2033

Other |

2026-02-04 11:10:16

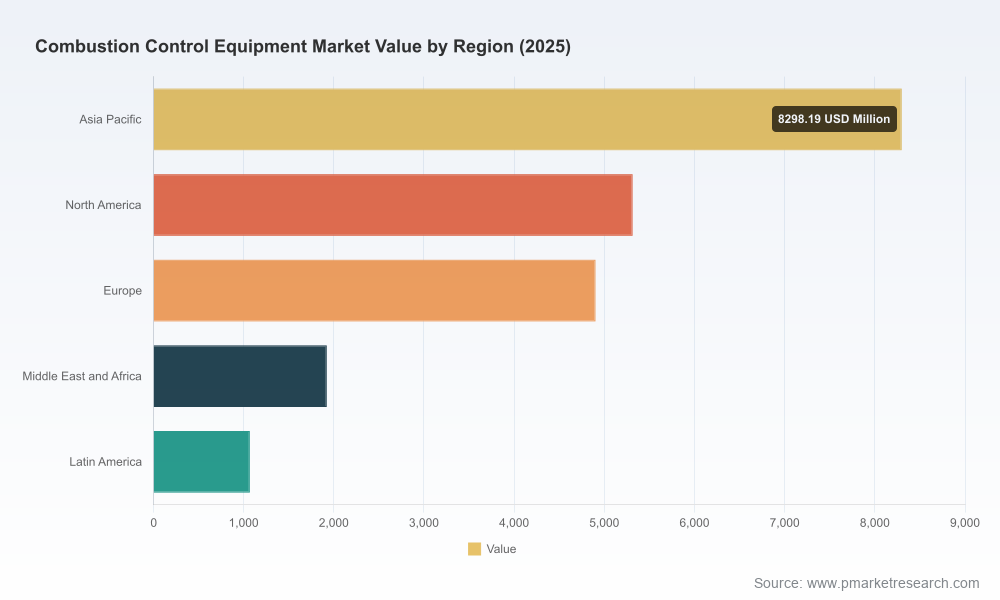

As energy transitions, emissions standards and capital discipline reshape industrial asset planning, PW Consulting’s latest Combustion Control Equipment Market report provides the tactical intelligence senior executives need to make high-confidence decisions in 2026. Built on a transparent historical baseline (2020–2025) with a 2025 base year and a seven-year forecast horizon (2026–2032), the study projects the total market to strengthen at a compound annual growth rate (CAGR) of 5.02% through 2032. Our high‑fidelity market model places the global market in the low‑tens of billions (USD million basis) in 2025 and forecasting a material uplift by 2032 — a trajectory that demands proactive strategy across procurement, plant engineering and product roadmaps.

Combustion Control Equipment Market

Budgeting and CapEx prioritization: The mid-single-digit CAGR and steady post‑pandemic recovery indicate predictable demand for combustion control upgrades. Procurement and asset teams can use our scenario outputs to sequence retrofit, replacement and new‑build projects across a multiyear capital plan.

Combustion Control Equipment Market

Regulatory compliance and retrofit timing: Tightening NOx and combustion efficiency requirements in key jurisdictions create windows for coordinated upgrade programmes — delaying action risks non‑compliance and higher retrofit complexity.

Combustion Control Equipment Market

Vendor selection and negotiation leverage: Market concentration metrics in our study reveal a moderately consolidated supplier landscape. This creates both advantages and exposure: operators can secure integrated solutions but should also hedge single‑vendor dependencies where mission‑critical reliability is at stake.

M&A and partnership diligence: For private equity and strategic buyers, the report’s competitive mapping and margin‑pressure scenarios inform valuation assumptions and post‑transaction integration plans.

Efficiency and emissions mandates: Global policy momentum targets measurable combustion efficiency gains by 2030. This regulatory driver accelerates demand for low‑NOx burners, advanced control systems and continuous monitoring, changing the feature set buyers prioritize.

Technology convergence: Digitalization — from advanced PLC/DCS integration to cloud‑enabled monitoring and predictive analytics — is shifting value from hardware alone to system‑level optimization and services. Buyers increasingly prize solutions that reduce fuel consumption, lower maintenance and deliver verifiable emissions reductions.

Supply‑side cost pressure: Raw material volatility and localized labor inflation have raised component and service costs. For example, stainless steel input price fluctuations and specialized technician wage increases are squeezing margins and lengthening lead times for certain assemblies.

Standards and safety frameworks: Updated industry standards for combustion safeguards remain a key constraint on product design and deployment timetables — compliance is both a cost and a differentiator for vendors.

Adopt a staged retrofit playbook. Prioritize high‑ROI combustion control upgrades that deliver rapid fuel savings and emissions reductions; defer low‑impact replacements to later windows when negotiated pricing or bundled contracts may be more favorable.

Design for software continuity. When replacing or augmenting hardware, ensure interoperability with existing DCS/SCADA layers and include lifecycle licensing and cybersecurity clauses in procurement contracts.

Force multiplier: services and outcome contracts. Consider shifting from capex‑heavy purchases to performance‑based contracts where vendors guarantee combustion efficiency or NOx thresholds — this aligns incentives and smooths cash flow.

Supply chain risk mitigation. Diversify sourcing for critical components and pre‑qualify multiple OEMs for spares and service to reduce single‑source exposure during raw material-driven lead‑time spikes.

Advanced burner management and integrated controls: Systems that tightly couple burner hardware with adaptive control algorithms are becoming baseline requirements for operators seeking sustained fuel and emissions gains.

Edge analytics and predictive maintenance: Embedded diagnostics and condition‑based maintenance models reduce unplanned downtime and O&M cost — shifting value capture from one‑time equipment sales to recurring service revenues.

Modular retrofit kits: To accelerate upgrades, vendors are packaging pre‑validated retrofit modules that reduce on‑site engineering time and simplify regulatory re‑approval.

Our qualitative and quantitative vendor analysis synthesizes company strategies, product stacks and recent moves. Market concentration is moderate — with the three‑player and five‑player concentration metrics indicating room for both established incumbents and well‑capitalized challengers to expand.

Honeywell International Inc. — A long‑standing provider of burner management systems and flame safeguard solutions, with a broad installed base in industrial boilers and furnaces and strong services capabilities.

Emerson Electric Co. — Brings integrated control systems (DeltaV) and burner management into tightly coupled automation solutions; recent product launches reinforce its focus on efficiency enhancement.

ABB Ltd. — Emphasizes integrated combustion safety and power‑electronic components; recent certification gains underpin its positioning for high‑safety applications.

Siemens AG — Offers process control platforms (PCS 7/SIMATIC) that enable system‑level optimization; demonstrations at major trade shows highlight roadmap alignment with digital control ecosystems.

Woodward, Inc. — Specialist in electronic controls and governors for engines and turbines, with strengths in high‑precision combustion management in rotating machinery.

Selected OEMs (Eclipse/Sterling, Fives/Maxon, Weishaupt, Oilon, Baltur) — These firms compete on burner hardware, safety modules and application‑specific control packages. Their depth in burner design and local service footprints is a competitive advantage in retrofit markets.

Notable recent industry moves reinforce the market’s direction: Siemens showcased advanced combustion solutions integrated with its newer PCS platform at Hannover Messe; Emerson launched a combustion controller aimed at enhanced boiler efficiency; and ABB secured high‑integrity safety certification for combustion safety modules. These developments signal vendor emphasis on integration, efficiency and safety — the three pillars buyers will demand in 2026.

Raw material volatility: Input cost spikes for component materials can compress supplier margins and be transmitted to buyers through sudden contract re‑pricing or extended lead times.

Skills shortage: Rising wage pressure for combustion systems technicians increases O&M bills and influences the economics of retrofits versus new builds.

Regulatory tightening: Longstanding directives and updated safety standards create compliance thresholds that materially affect retrofit scope, testing requirements and project timelines.

Proprietary market model: A transparent, scenario‑driven model with historical reconciliation (2020–2025) and edge cases for decarbonization and raw material stress. This model is exportable for in‑house sensitivity testing.

Vendor playbooks: Tactical sourcing templates, SLA language, and recommended qualification criteria by application class to fast‑track procurement cycles.

Technology evaluation matrix: Comparative assessments of control systems, burners, monitoring platforms and retrofit modules against efficiency, safety, digital readiness and TCO.

Use cases and case studies: Real‑world deployment examples illustrating project timelines, measured fuel savings, emissions outcomes and service models.

Regulatory and compliance roadmap: Jurisdictional impact summaries and recommended compliance staging for major standards and directives.

Deal and M&A playbook: Valuation sensitivities, integration checklists and 100‑day plans for target assets in the combustion equipment space.

Short term (0–12 months): Use our procurement templates and vendor scorecards to re‑run RFPs with new performance KPIs tied to fuel and emissions outcomes.

Medium term (12–36 months): Sequence capital works to align with regulatory deadlines and vendor product roadmaps; prioritize modular retrofits where lead times are constrained.

Long term (3+ years): Reassess fleet strategies — consider contracting for outcomes, consolidating vendors where integration yields measurable OPEX benefits, and positioning for digital monetization of monitoring and services.

The combustion control equipment market presents a measured growth opportunity through 2032, driven by regulatory pressure, efficiency mandates and continued digitalization. For executives formulating 2026 budgets and strategic plans, the choice is between reactive, one‑off upgrades and an orchestrated programme that captures fuel, emissions and service economics. PW Consulting’s report delivers the actionable intelligence — from scenario models to vendor playbooks — that turns market forecasts into executable strategy. To unlock the full dataset, detailed segmentation and our downloadable model, please visit the full report page for subscription and licensing options.

For detailed analysis of this topic, please visit the official page:Combustion Control Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com