Hospital Acquired Infection (HAI) Control Market — Strategic Preview for 2026 Decisions

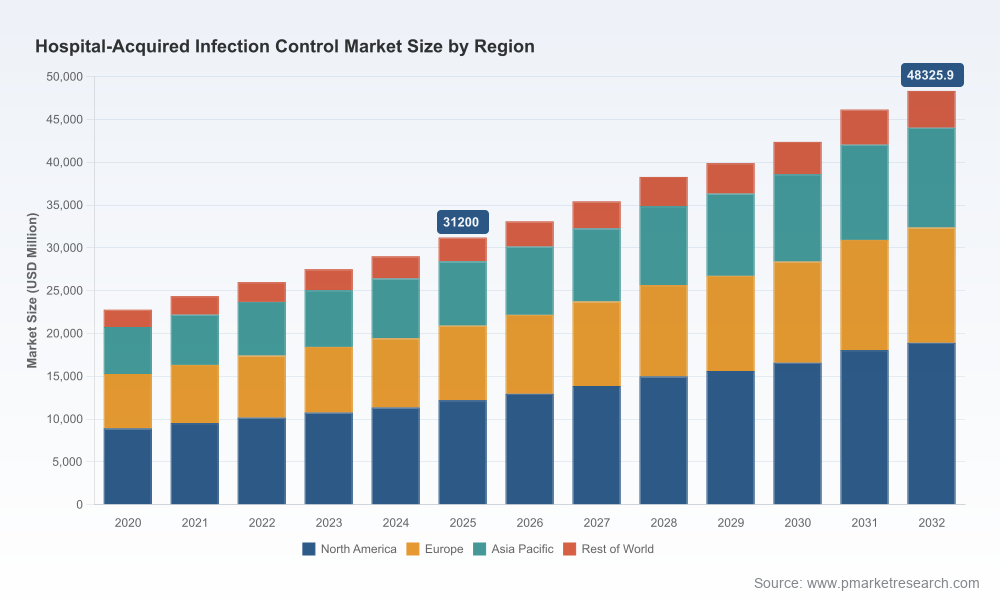

As healthcare systems enter 2026, infection prevention remains a strategic fulcrum for hospitals, device manufacturers, service providers, and payors. PW Consulting’s latest market study — using 2025 as the base year and projecting across 2026–2032 — shows the global HAI control market positioned for steady expansion, growing at a compound annual growth rate (CAGR) of 6.45%. In dollar terms, the market moves from roughly USD 31.2 billion in 2025 toward an expected market size in the high‑40s (USD millions) by 2032. This preview highlights the report’s strategic value for near‑term corporate decisions while intentionally withholding granular segment tables to encourage direct engagement with the full analysis.

Hospital Acquired Infection Control Market

Why this report matters for 2026 strategy

- Investment timing: The market’s mid‑single‑digit CAGR signals a durable upswing rather than a short cyclical spike — essential context for capex and product pipeline prioritization.

- Competitive positioning: The sector is moderately fragmented (top‑3 firms account for under one‑third of sales; the top‑5 fall below half), creating runway for both incumbent expansion and specialist entrants to capture share through bundled offerings or regulatory differentiation.

- Regulatory sensitivity: Recent agency activity and shifting post‑market obligations means product approvals and clinical claims will increasingly determine commercial access. Companies that bake compliance and evidence generation into product roadmaps will enjoy first‑mover advantage.

- Procurement pressure: Persistent financial penalties and value‑based purchasing in core markets continue to make HAI control not just a clinical priority but a financial imperative for provider systems.

What the report delivers (practical, board‑level to tactical)

- Robust market sizing and a seven‑year forecast (2026–2032) by product cluster and application class, with scenario runs that isolate upside from accelerated adoption of novel disinfection modalities.

- Competitive landscape mapping with capability matrices and go‑to‑market archetypes for dominant players, fast followers, and pure‑play specialists.

- Regulatory and reimbursement heatmaps linking device class to approval risk and payer exposure; includes implications of recent agency dialogues around germicidal UV and expanded MDR post‑market surveillance.

- Technology adoption curves and procurement playbooks for hospital systems — including ROI models calibrated to typical inpatient volumes and penalty avoidance pathways.

- M&A and partnership playbook: target screening criteria, valuation multipliers observed in recent deals, and diligence checklists tailored to sterilization, consumables, and service contracts.

- Operational diagnostics for supply‑chain resilience and manufacturing scale‑up, plus supplier due‑diligence templates for outsourcing sterilization services.

Market dynamics shaping 2026 decisioning

- Regulatory evolution: Regulators have sharpened attention on claim substantiation for technologies that purport to reduce HAIs. Recent advisory interactions and device clearances have established early precedents for whole‑room UV and other non‑traditional modalities — creating both opportunities and new evidentiary burdens for suppliers.

- Policy incentives and penalties: Payor mechanisms that penalize hospitals for elevated HAI rates continue to drive procurement of preventive technologies. Providers are prioritizing investments that deliver measurable reductions in infection rates and demonstrable financial ROI.

- Technology complementarity: Adoption is best understood as a portfolio decision across consumables, sterilization equipment, and software/monitoring services. Winners will be those who can bundle consumable economics with predictable uptime and measurable outcomes.

- Serviceization trend: Outsourced sterilization and robotics-as-a-service models are gaining traction among mid‑sized systems that lack capital budgets for in‑house scale. Contract sterilization providers and systems integrators are becoming strategic partners rather than passive suppliers.

Competitive landscape — strategic profiles

Our analysis profiles major industry participants and identifies how distinct strategic moves map to near‑term opportunity windows:

Hospital Acquired Infection Control Market

- 3M Company (Maplewood, Minnesota, USA): Portfolio breadth across prevention consumables and sterilization monitoring gives 3M a defensive advantage in bundled procurement scenarios. Their strength lies in cross‑selling and lifecycle contracts tied to consumable consumption patterns.

- STERIS plc (operational HQ: Mentor, Ohio, USA): With a strong foothold in sterilizers, washer‑disinfectors, and sterile‑processing services, STERIS competes on systems reliability and service penetration in centralized sterile supply workflows.

- Getinge AB (Gothenburg, Sweden): Getinge’s combination of capital equipment and consumables — complemented by targeted acquisitions to broaden U.S. distribution — positions it for share gains where end‑to‑end sterile processing optimization is valued.

- Ecolab Inc. (Saint Paul, Minnesota, USA): Ecolab’s strength is in enterprise hygiene programs and service delivery models that translate product consumption into operational outcomes — making it a preferred partner in multi‑facility contracts.

- Becton, Dickinson and Company (BD) (Franklin Lakes, New Jersey, USA): BD leverages device‑level infection prevention features — e.g., antimicrobial catheters — tying product innovation directly to clinical outcomes and hospital KPI improvement.

- Xenex Disinfection Services Inc. (San Antonio, Texas, USA): A specialist in pulsed xenon UV systems, Xenex exemplifies category specialists that can scale via regulatory validation and proof‑of‑outcome studies.

- Advanced Sterilization Products (ASP, Fortive) (Irvine, California, USA): With low‑temperature sterilization systems, ASP targets heat‑sensitive device sterilization — a technical niche that commands premium pricing where device throughput and instrument compatibility matter.

- Belimed AG (Zug, Switzerland): Focused on washer‑disinfectors and sterile processing equipment, Belimed competes on engineering quality and integration with hospital workflows.

- Sotera Health (including Sterigenics) (Broadview Heights, Ohio, USA): Contract sterilization services make Sotera a critical capacity partner for device manufacturers and hospital systems seeking third‑party sterilization or backlog relief.

Recent market events underscore shifting battlegrounds: regulatory clearances for UV‑based whole‑room systems and De Novo authorization of engineered microbial‑reduction devices (late 2025) have created new evidence corridors and go‑to‑market opportunities for innovators. Strategic acquisitions focused on consumables distribution further signal consolidation plays around installed bases and distribution reach.

Hospital Acquired Infection Control Market

Strategic implications and recommended 90‑ to 720‑day actions for 2026

- For manufacturers: Prioritize regulatory roadmap investments early. Allocate budget to clinical outcomes studies that match payer metrics; fast followers should consider licensing or co‑development agreements to accelerate time to claim substantiation.

- For investors and M&A teams: Target mid‑market specialists with asset light service models or unique regulatory clearances. Valuation arbitrage exists where clinical evidence is scarce but market demand is visible.

- For hospital systems: Conduct rapid portfolio optimization pilots (60–120 days) combining consumables, UV/hybrid disinfection, and monitoring software to quantify KPI improvements and cost offsets associated with penalty avoidance.

- For service providers: Expand outcome‑based contracting capabilities and analytics dashboards that translate device usage into financial and quality KPIs; these capabilities materially improve retention in multi‑facility engagements.

- For product teams: Embed post‑market surveillance and real‑world evidence generation into commercial launches to address escalating regulator expectations in both the EU and U.S.

How PW Consulting’s report reduces execution risk

Organizations using this study will benefit from scenario‑tested forecasts, supplier due‑diligence templates, and pragmatic ROI models aligned to actual hospital reimbursement levers. The combination of competitive intelligence, regulatory foresight, and executable procurement playbooks shortens decision cycles and de‑risks capital allocation in 2026.

Next steps (readers seeking the full intelligence)

- Download the complete report for detailed segment forecasts, proprietary company scorecards, supply‑chain stress tests, and an M&A target shortlist (full segment tables and downloadable datasets are available only in the full report).

- Book a strategic briefing with PW Consulting’s HAI practice to receive a tailored implications memo for your portfolio, including a 12‑month action plan aligned to your role (manufacturer, provider, investor, or service provider).

In short, the HAI control market presents a predictable growth runway underpinned by regulatory pressure, payment incentives, and accelerating adoption of bundled, outcome‑oriented offerings. Firms that invest now in evidence, integrated solutions, and flexible commercial models will be best positioned to capture disproportionate value across 2026 and beyond. For the granular tables and the proprietary scenario outputs referenced here, please consult the full PW Consulting Hospital Acquired Infection Control Market report.

For detailed analysis of this topic, please visit the official page:Hospital Acquired Infection Control Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com