Wafer FOUP Market — Strategic Imperatives for 2026: A PW Consulting Preview

As PW Consulting’s senior strategy advisor and lead industry analyst, I present an executive preview of our latest market research on Wafer Front Opening Universal Pods (FOUPs). This analysis synthesizes macro-scale market trajectories, competitive dynamics, technology imperatives, and practical, actionable guidance that should shape boardroom and procurement decisions throughout 2026. The full report contains exhaustive segment-level intelligence, supplier scorecards, and transaction-ready playbooks; this release follows a “trailer” approach—demonstrating analytical depth while reserving the granular tables and proprietary segment extracts for subscribers.

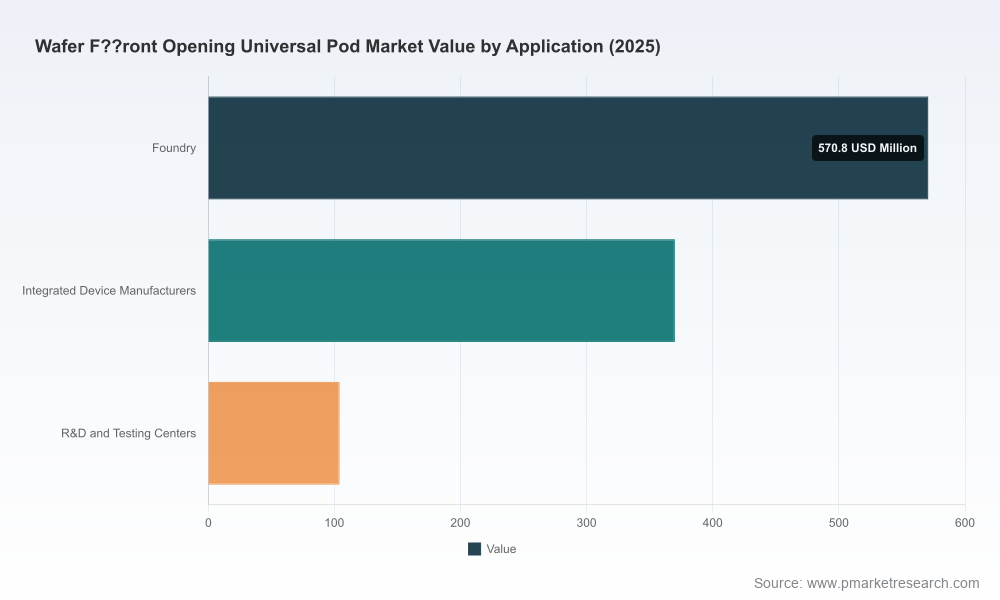

Wafer Front Opening Universal Pod (FOUP) Market

Market Outlook at a Glance

The FOUP market reached approximately USD 1,045 million in our base year (2025) and is forecast on a compound annual growth rate (CAGR) of 8.7% through our 2026–2032 horizon. Short-term projections anticipate continued expansion in 2026, driven by installed capacity growth in foundries and IDM upgrades, with sustained momentum into the early 2030s as advanced node production and packaging throughput scale. Market concentration is high — the top three and top five suppliers account for the large majority of industry revenue — a structural fact that materially affects supplier power, pricing dynamics, and entry economics for new competitive offerings.

Wafer Front Opening Universal Pod (FOUP) Market

Why this matters for 2026 Decisions

- Timing matters: With capital allocation cycles accelerating across wafer fabs, procurement and capacity decisions made in 2026 will lock equipment and consumable relationships that persist across multi-year manufacturing ramps.

- Supplier selection is strategic: High market concentration means a handful of suppliers will influence lead times, design compatibility, and aftermarket services. Understanding supplier footprints, compliance certifications, and recent capacity moves is essential to reduce supply risk.

- Standards and materials are non-negotiable: Compliance with SEMI specifications and the choice of ultra-low outgassing/high-purity polymers are core determinants of yield, contamination risk, and long-term TCO.

Key Market Dynamics and Strategic Drivers

- Fabrication mix and node transitions: Demand for FOUPs is tied to fab build-outs, new tool deployments, and transitions to larger wafer formats and EUV-enabled capacities. The interplay between foundry expansions and IDM modernization programs will be a dominant driver in 2026.

- Advanced microenvironment control: Nitrogen purgeable, diffusion-managed, and enhanced sealing FOUP variants are moving from niche to mainstream as fabs seek stricter particle control and extended wafer dwell with minimal contamination risk.

- Automation and AMHS integration: FOUP designs that prioritize robot-friendly interfaces, repeatable dimensional accuracy, and lifecycle robustness provide tangible savings in automation downtime and maintenance overhead.

- Regulation and standards pressure: SEMI standards (for dimensional, materials, and interface requirements) continue to set the baseline for design compliance. Nonconformance risks costly retrofits and throughput penalties.

- Geopolitical reshaping of supply chains: Regionalization trends and reshoring initiatives are driving suppliers to diversify manufacturing footprints. This influences lead times, freight costs, and local content requirements in procurement decisions.

Competitive Landscape — What the Leading Suppliers Tell Us

The FOUP supplier universe combines global incumbents with regional specialists. The market’s top tier demonstrates clear differentiation along three axes: product breadth (standard vs. purgeable/advanced variants), manufacturing footprint (ability to supply local fabs quickly), and services (cleaning, reuse, and aftermarket support).

Wafer Front Opening Universal Pod (FOUP) Market

- Entegris (Billerica, MA, USA): A systems-oriented incumbent offering a broad FOUP portfolio and recent production expansion in the U.S. This move reinforces its capacity to support North American fab investment and shortens supply chains for key customers. Its emphasis on microenvironment control and multiple form factors positions it to capture projects prioritizing automation compatibility and low total cost of ownership.

- ePAK International (Malaysia, global ops): Known for SEMI/FIMS-compliant eFOUP carriers with multiple purge options and strong AMHS compatibility. Recent catalog refreshes underscore product maturity and responsiveness to design-in requirements for global foundries.

- Miraial & Shin-Etsu Polymer (Japan): These suppliers emphasize precision materials engineering—high-function plastics, outstanding sealing and dimensional stability—addressing long-term operational reliability inside fabs. Their product strategies appeal to customers prioritizing contamination control and lifecycle predictability.

- Gudeng (Taiwan): A supplier with pronounced exposure to advanced packaging and foundry channels. Its product roadmap and geographic expansion efforts reflect the broader industry trend of diversifying production away from single-source regions.

- Regional players (3S Korea, CKplas, Dainichi, E-SUN, Pozzetta): These vendors add competitive depth, particularly in localized service offerings (cleaning, reuse programs) and specialized FOUP variants for niche fab processes.

Recent industry movements underscore these strategic currents: supplier production expansions in North America, renewed product catalog releases highlighting purge and AMHS compatibility, and targeted equipment supply agreements for high-volume fabs. These signals validate our view that capacity, standards compliance, and aftermarket services will be decisive procurement filters in 2026.

What the Report Contains — Practical, Actionable Modules

Our full market study is organized to inform operational decisions and corporate strategy with executable outputs. Key components include:

- Proprietary market sizing and forecast model (historical base 2020–2025, forecast 2026–2032) with scenario sensitivity for demand shocks, capex accelerations, and adoption curves for advanced FOUP variants.

- Supplier benchmarking and scorecards covering product lines, capacity footprints, compliance credentials, delivery performance, warranty and service terms, and aftermarket economics.

- Technology deep dives on materials selection, sealing systems, nitrogen purge architectures, and automation interface standards — including failure modes, maintenance regimes, and lifetime cost analysis.

- Procurement playbook: RFP templates, evaluation matrices, negotiation levers tied to lead times, volume discounts, and service SLAs; plus recommended inventory buffer strategies by risk profile.

- M&A and partnership primer: targets, value levers, and integration risk profiles for buyers or fab operators looking to internalize supply or vertically integrate handling solutions.

- Regulatory and supply-risk matrix: SEMI compliance mapping, raw-material exposure analysis, and contingency planning for geopolitical supply shocks.

Strategic Recommendations — Priorities for 2026

- Lock in compatible suppliers early: For fabs planning capacity ramps in 2026–2027, pre-negotiating supply agreements with tier-1 vendors mitigates lead-time premium risk and secures priority allocation during shortages.

- Prioritize standards-conformant designs: Contract language should mandate SEMI compliance and provide acceptance testing criteria to avoid retrofit exposure and downstream automation conflicts.

- Evaluate total cost of ownership, not unit price: Consider lifecycle cleaning, repair/reuse programs, contamination-related yield impact, and spare pool logistics when comparing vendor offers.

- Localize where strategic: Use supplier footprint as a selection criterion when regional policy, freight risk, or time-to-deploy are decisive. Shorter logistics translates into lower carrying costs and faster MTTR for damaged carriers.

- Incentivize modularity and future-proofing: Demand designs that allow upgrades (e.g., retrofit purge modules) to extend asset utility as fab needs evolve.

Risk Signals to Monitor in 2026

- Raw-material tightness: Availability of high-purity polymers and specialty conductive materials can create single-point supply risk; contractually obligate secondary sources and inspection rights.

- Standard evolution: Changes in SEMI standards or automation interfaces may force retrofits—monitor standards committees and incorporate change-management clauses into long-term supply agreements.

- Supplier consolidation or capacity redeployment: Given the high CR3/CR5 concentration, any supplier consolidation or repurposing of capacity could materially affect availability; maintain a diversified qualified-supplier list.

How Executives Should Use This Preview

Use the insights here to orient 2026 strategic planning cycles: prioritize supplier qualification, incorporate FOUP procurement into fab capex timelines, and align materials/R&D investments with contamination-control imperatives. For procurement teams, our procurement playbook will materially reduce negotiation cycle time and improve supply certainty. For corporate strategy teams, the report’s M&A primer identifies where verticalization or strategic partnerships can deliver margin or resilience gains.

Next Steps & Accessing Full Intelligence

This preview is curated to demonstrate the analytical rigor and operational utility of PW Consulting’s full FOUP market report while preserving the detailed segmentation, supplier share tables, and model outputs that subscribers rely on for transaction-level decisions. For access to the complete dataset, supplier scorecards, download-ready RFP templates, and our interactive forecast model, please visit the PW Consulting report page and request the full Wafer FOUP Market report.

In 2026, FOUP procurement and strategy will no longer be a commoditized checkbox: it is a lever of yield protection, automation efficiency, and supply resiliency. The right decisions now will materially influence fab economics for years to come.

For detailed analysis of this topic, please visit the official page:Wafer Front Opening Universal Pod (FOUP) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com