Injectable Targeted Therapy Market Dynamics: Key Drivers and Restraints

Other |

2026-06-18 08:42:14

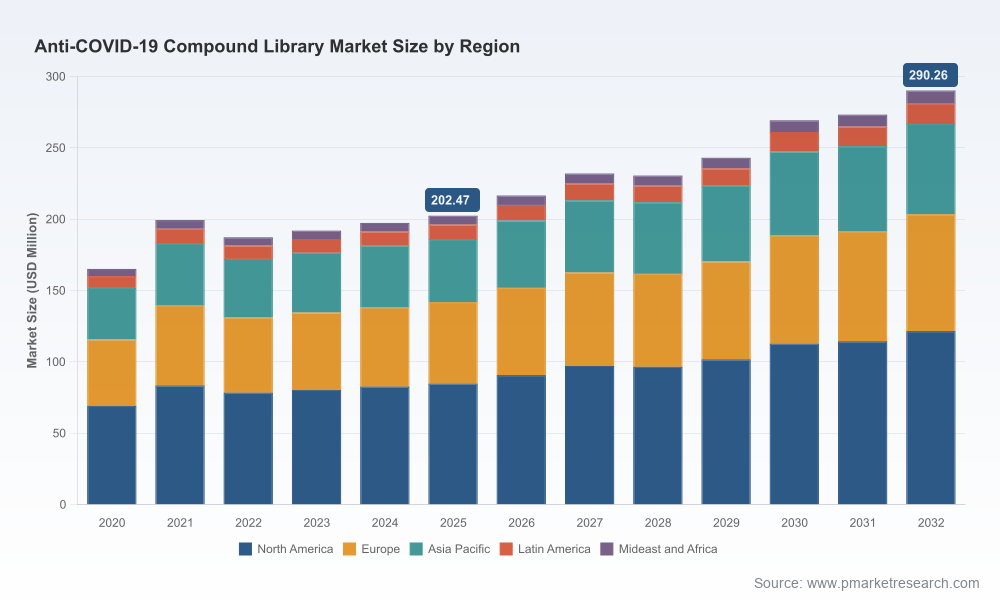

PW Consulting’s latest market study on the Anti‑COVID‑19 Compound Library market (base year: 2025; historical window: 2020–2025; forecast: 2026–2032) delivers a focused, actionable intelligence pack designed to support Boardroom and R&D leadership decisions in 2026. Anchored by rigorous market modelling and vendor due diligence, the report shows a steady expansion trajectory driven by sustained investment in antiviral discovery and renewed pandemic preparedness. The market is projected to expand at a compound annual growth rate (CAGR) of 5.28% over the forecast window, rising from the 2025 baseline to a materially larger market by 2032. This briefing highlights the strategic takeaways while deliberately withholding detailed sub‑segment datapoints to encourage access to the full report for transaction‑level intelligence.

Anti Covid 19 Compound Library Market

Strategic re‑prioritisation of infectious‑disease pipelines: Biopharma and biotech organizations are reallocating discovery budgets toward broad‑spectrum antivirals and coronavirus‑focused programs—creating steady demand for curated compound libraries built for rapid hit‑finding and downstream lead optimisation.

Anti Covid 19 Compound Library Market

Operationalisation of high‑throughput screening (HTS) and phenotypic assays: The growing adoption of pre‑dissolved, plate‑ready libraries and integration with HCS/AI workflows is shortening discovery cycles and changing supplier value propositions.

Anti Covid 19 Compound Library Market

Open science and consortium effects: Open initiatives and registries are reshaping how collections are curated and shared, increasing the pace of candidate identification while raising questions about IP, licensing and supplier differentiation.

Our modelling, calibrated against vendor catalogues, public disclosures and primary interviews, shows resilient year‑on‑year growth with modest volatility reflecting episodic R&D surges. The market structure displays a moderate concentration: the top three suppliers command a near‑majority share, while the five largest firms control close to two‑thirds of commercial activity. This concentration has meaningful implications for pricing leverage, catalogue uniqueness and supply‑chain concentration risk.

Regulatory and commercial caveats are central to supplier selection: compound libraries are marketed and sold for research use only (RUO). Many collections originate from virtual screening against SARS‑CoV‑2 targets (for example, 3CL protease, Spike, ACE2) and, as vendors state, such in silico selection does not equate to validated clinical efficacy. Buyers must treat in‑catalogue annotations as starting points rather than confirmed therapeutic claims.

Executive synthesis with scenario planning: multiple 2026‑to‑2032 demand scenarios and sensitivity tests that help executives stress‑test strategic choices under different pandemic and funding assumptions.

Market sizing and forecasting methodology: transparent inputs, assumptions and reconciliation of historical data (2020–2025), with a probabilistic forecast framework for 2026–2032.

Vendor benchmarking and capability maps: comparative scoring across catalogue depth, novelty of chemotypes, availability of pre‑plated/high‑throughput formats (e.g., pre‑dissolved DMSO solutions, 96/384‑well plates), custom synthesis and cherry‑picking services, QC workflows and lead times.

Competitive intelligence dossiers: tactical profiles and supplier playbooks covering commercial positioning, GTM strategies, price banding, partnership history and M&A signals.

Technical annexes: assay‑compatibility checklists, common library formats and handling guidance, and an annotated glossary of library types (FDA‑approved scaffolds, natural products, fragment sets, target‑focused collections) to align procurement and discovery teams.

Procurement and supply‑chain risk matrix: supplier concentration, geographic sourcing risk, inventory buffers and recommended procurement levers to assure continuity for critical screening campaigns.

Actionable recommendations: a 12‑month roadmap for R&D leaders outlining tactical sourcing, pilot engagements, and partnership models to accelerate hit identification while protecting program timelines and IP.

TargetMol (Boston, MA, USA) — Offers curated Anti‑COVID‑19 libraries with compounds annotated for confirmed or putative anti‑SARS‑CoV‑2 activity. Their value proposition is catalogue depth for targeted screening campaigns and rapid procurement workflows. Strategic implication: attractive for organisations that prioritise ready‑to‑screen, well‑annotated small collections with short procurement lead times.

MedChemExpress (Monmouth Junction, NJ, USA) — Markets large anti‑coronavirus libraries assembled from virtual screening against key viral targets and offers flexible formats (pre‑dissolved or solid). Strategic implication: well suited to HTS centres seeking extensive virtual‑enrichment sets but requires careful secondary validation to prioritise true actives.

Enamine (Kyiv, Ukraine) — Distinctive for very large coronavirus‑focused collections and an integrated custom‑synthesis capability. Notably, Enamine’s recent open‑science contribution generated >2,000 novel compounds and a pre‑clinical candidate — a clear signal of R&D throughput and upstream pipeline contribution. Strategic implication: optimal partner for organisations that require extensive chemical diversity and scalable synthesis for hit‑to‑lead follow‑up.

Life Chemicals (Burlington, ON / Kyiv, Ukraine) — Emphasises modular library construction with options for cherry‑picking and pre‑plating. Strategic implication: attractive for programs needing bespoke subsets tailored to specific targets or assay formats.

ChemDiv (San Diego, CA, USA) — Positions curated coronavirus libraries through ML‑driven and 3D‑shape analysis to enrich for phenotypic hits and nucleoside mimetics. Strategic implication: a supplier to engage when phenotypic screening and AI/ML‑augmented triage are core to discovery strategy.

Selleck Chemicals (Houston, TX, USA) — Offers broader anti‑infection and antiviral libraries that can support cross‑screening strategies between pathogen classes. Strategic implication: useful for programmes exploring repurposing opportunities or cross‑pathogen efficacy.

Open‑science contributions and candidate disclosure (e.g., a vendor’s 2025 synthesis of >2,000 compounds culminating in an early pre‑clinical candidate) accelerate the availability of novel chemistries but also raise questions about commercial exclusivity and partnering models.

Consortium efforts and registries now provide federated catalogues and comparability indexes; these tools lower search friction but increase the importance of provenance, QC and downstream validation for buyers.

Regulatory framing remains consistent: libraries are sold for research use only; vendors typically disclose that virtual screening does not equal biological confirmation. Procurement teams must bake in secondary validation workflows when forecasting timelines and budgets.

Define the discovery objective before choosing a supplier: clarity on whether the priority is rapid phenotypic hit‑finding, target‑focused screening, fragment‑based lead finding, or repurposing materially changes supplier fit and cost structure.

Blend catalogue depth with custom capability: for programmes likely to require rapid synthesis of follow‑ups, prefer suppliers who combine large, diverse libraries with in‑house or partnered custom‑synthesis capability to compress timelines.

Mitigate concentration risk: the market’s moderate concentration means single‑supplier dependence can create bottlenecks; implement dual‑sourcing and maintain a comparator panel drawn from orthogonal suppliers to reduce supply and novelty risk.

Operationalise validation: require suppliers to disclose selection methodology and QC data; mandate a staged validation budget to triage in silico hits into functional assays before committing to lead optimisation spend.

Use consortium datasets judiciously: registries accelerate scouting but demand stricter provenance checks—negotiate data‑use terms that preserve downstream IP options where needed.

Negotiate flexible commercial terms: program‑based pricing, pilot packs and cherry‑pick options help align supplier economics with discovery risk and reduce sunk inventory.

This briefing intentionally omits the granular sub‑segment tables and supplier market shares that underpin tactical sourcing and M&A decisions. The full PW Consulting report contains the detailed breakouts, vendor scorecards, pricing bands, and downloadable annexes required to operationalise sourcing and partnership decisions in 2026. For procurement teams, R&D heads and corporate development officers preparing 2026 budgets and strategic roadmaps, the full dossier provides the transaction‑grade evidence needed to negotiate supplier agreements, plan pilot screenings and structure partnership or acquisition diligence.

To obtain the complete report and the supporting datasets (including the model workbook and supplier dossiers), contact PW Consulting’s Market Intelligence team or visit our report page for ordering details. Our team can also arrange a tailored briefing to map the report’s scenarios to your organisation’s budget, pipeline and supplier footprint.

PW Consulting — we translate complex market dynamics into crisp strategic choices so your 2026 antiviral discovery investments convert into validated programs and durable competitive advantage.

For detailed analysis of this topic, please visit the official page:Anti Covid 19 Compound Library Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com