Professional Microneedling in Manchester for Skin Rejuvenation

Health |

2026-07-06 17:57:37

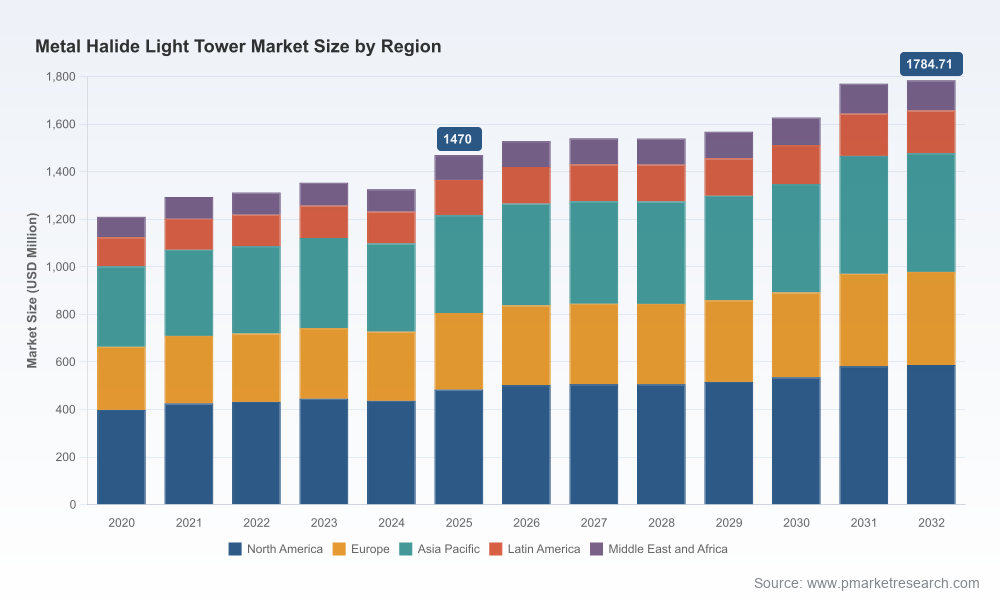

PW Consulting’s latest industry briefing, drawn from our full Metal Halide Light Tower Market report (base year 2025, forecast 2026–2032), distills the evidence-based guidance executives and asset managers need to set strategy in 2026. The market reached approximately USD 1,470 Million in 2025 and, under the central scenario in our model, is projected to grow at a compound annual growth rate (CAGR) of about 2.81% over the 2026–2032 forecast window, reaching the high‑single‑hundreds of millions in incremental value by 2032. This release highlights the strategic levers, competitive dynamics, and near‑term risks that should shape procurement, product development, and M&A choices next year.

Metal Halide Light Tower Market

Actionable timing: The market’s modest but steady growth profile means 2026 will be pivotal for firms deciding between scarce capital allocation for incremental product upgrades or targeted fleet renewals. Marginal gains in operational uptime or lamp performance can tilt ROI in constrained budgets.

Metal Halide Light Tower Market

Demand concentration and customer segmentation: Our analysis shows demand remains concentrated in heavy‑duty, large‑area illumination applications where metal halide retains technical advantages. The structure favors vendors that combine rugged engineering with flexible rental and service models.

Metal Halide Light Tower Market

Supply‑side fragilities: Raw material and regulatory trends (notably lamp component supply chains and on‑engine emissions standards) create windows of competitive advantage for firms with secured supply and early compliance plans.

Persistent niche demand: Despite LED adoption across many lighting categories, metal halide towers maintain relevance where very high lumen output and specific color rendering characteristics are mission‑critical — for example, large mining operations, major industrial turnarounds, and certain oil & gas sites. Buyers prioritizing area coverage and instantaneous high‑intensity light continue to opt for metal halide solutions.

Regulatory and emissions context: Diesel‑powered units intended for construction and industrial use must adhere to strict emissions regimes in key markets (for example, Tier 4 Final standards in the U.S.). Compliance timelines and retrofit costs should be modeled into 2026 capex plans; noncompliance risk can materially affect fleet usability on large contracts.

Component and lamp market pressures: Metal halide lamps rely on specialized halide blends and quartz arc tubes. The broader lamp market dynamics (with lamp market size indicators underscoring multi‑billion dollar scale) mean purchasing strategies and supplier diversification will be decisive for margin protection in 2026.

Rental market and asset utilization: The rental channel remains central to equipment deployment. In 2026, rental companies balancing utilization and replacement cycles will dictate spot demand patterns, creating opportunities for manufacturers that can deliver fast lead times and robust after‑sales service.

The market exhibits moderate concentration: the top three vendors account for a meaningful portion of industry revenue, and the top five command a majority share of organized supply. This concentration produces advantages for established global OEMs in procurement, distribution, and aftermarket services, while leaving room for specialized and regional players to capture niche projects through customization and speed.

Atlas Copco (Stockholm): Known for heavy‑duty HiLight series and ruggedized design features (e.g., HardHat canopies), Atlas Copco competes strongly in quarry, rental, and harsh‑environment segments. Their emphasis on durability and serviceability makes them a go‑to for operators prioritizing lifecycle cost.

Generac Mobile / Magnum (Waukesha): With compact vertical mast designs and several vertical lamp configurations, Generac’s Magnum MLT line targets mainstream construction and industrial sites. Their product breadth and dealer networks support rapid deployment strategies favored by rental houses.

Wacker Neuson (Munich): The company’s LTV and LTS platforms offer flexible configurations for site work and event applications. Their reputation for engineering consistency positions them well where modularity and parts commonality matter.

Specialists & regional manufacturers: Firms such as Grandwatt Electric Corp, Boss LTG (BossLTR), DMI Light Towers, Trime USA, and Larson Electronics play pivotal roles in custom projects, very large coverage solutions, and hazardous‑area applications. Their ability to engineer bespoke solutions or extremely high‑output arrays is an important complement to the global OEMs’ standardized fleets.

Market intelligence updates through 2025–2026 underscore steady, niche demand in construction, mining, and event rental segments, and signal that suppliers are diversifying architectures rather than pursuing a single conversion path to alternatives.

Procurement teams report increasing interest in mixed fleets (metal halide plus LED) to balance intensity requirements with energy and emissions goals; this hybrid strategy has implications for service footprints and spare‑parts inventories.

Our full report is designed as a practical playbook, not just a descriptive market brief. Key deliverables include:

Forward‑looking revenue model and sensitivity scenarios across a 2026–2032 horizon calibrated to multiple end‑market demand paths and regulatory trajectories.

Vendor scorecards assessing product robustness, service network quality, compliance readiness, spare‑parts logistics, and rental channel penetration — enabling quick comparative diagnostics for sourcing teams.

CapEx and fleet‑renewal optimization matrices that translate forecast volatility and price pressure into opportune purchase windows and lease vs. buy thresholds.

Commercial playbooks for manufacturers and rental operators: pricing tactics, warranty frameworks, modular product strategies, and aftermarket monetization models tailored for 2026 market conditions.

Regulatory impact assessment mapping emissions standards and retrofit costs to deployment constraints in major markets, plus supplier mitigation strategies to reduce compliance exposure.

Supply‑chain heatmap including lamp and key component risk indicators, with recommended supplier diversification and inventory strategies to safeguard lead times.

Deal pipeline guidance and M&A heuristics identifying target profiles (capability fills, geographic access, or service network expansion) most likely to accelerate scale or margin improvement.

For manufacturers: Prioritize ruggedization and serviceability updates that reduce total cost of ownership. Invest selectively in emissions‑compliant engine platforms and establish captive refurbishment capabilities to extend asset life without eroding margins.

For rental operators: Adopt a mixed‑fleet deployment model where metal halide units are reserved for high‑intensity, large‑area contracts while LEDs cover energy‑sensitive, long‑duration uses. Negotiate supply agreements that include priority allocation for lamp components to avoid project delays.

For investors and M&A teams: Seek bolt‑on targets that add unique engineering competence (high‑mast platforms, hazardous area certifications), regional distribution reach, or deep OEM service networks. Valuations should reflect the moderate market growth and the importance of aftermarket revenues.

For procurement and project owners: Factor emissions compliance and retrofit windows into tender specifications. In high‑intensity applications, prioritize uptime guarantees and rapid parts replacement clauses over headline lamp efficiency metrics.

PW Consulting’s deliverables are intentionally pragmatic: we combine granular operational inputs with scenario testing to produce near‑term operational directives while preserving the competitive confidentiality clients require. This press release highlights the strategic contours you need to evaluate, while the full report contains the detailed segmentation, supplier benchmarking tables, and downloadable decision tools that operational teams can use directly in procurement and capital planning.

The analysis integrates primary interviews with OEMs, rental houses and large end users, proprietary shipment and utilization datasets, and triangulation against publicly available regulatory and lamp‑component market indicators. Historical coverage spans 2020–2025 to anchor trend analysis, and multiple forecast paths are provided to reflect commodity and regulatory variability through 2032.

Run a 12‑month procurement scenario: assess cost of ownership outcomes under Tier 4 compliance and component shortage scenarios; prioritize inventory hedges where lamp lead times are greater than 8–12 weeks.

Test a mixed‑fleet pilot: deploy metal halide only on contracts with clearly defined high‑output requirements and benchmark utilization and downtime against LEDs in parallel sites.

Engage vendors on service guarantees and parts availability clauses in procurement contracts to protect against lead‑time shocks in 2026.

Note: this briefing intentionally omits detailed region‑ and application‑level percentage breakouts and other segment tables to preserve the value of the full market deliverable. For the complete intelligence suite — including segmented revenue models, vendor scorecards, and downloadable optimization tools designed for immediate deployment in 2026 planning cycles — consult the PW Consulting Metal Halide Light Tower Market report available through PW Consulting’s research portal.

Contact PW Consulting’s industry desk to arrange a briefing, obtain executive summaries, or license the full dataset and scenario models for integration into your 2026 strategic planning process.

For detailed analysis of this topic, please visit the official page:Metal Halide Light Tower Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com