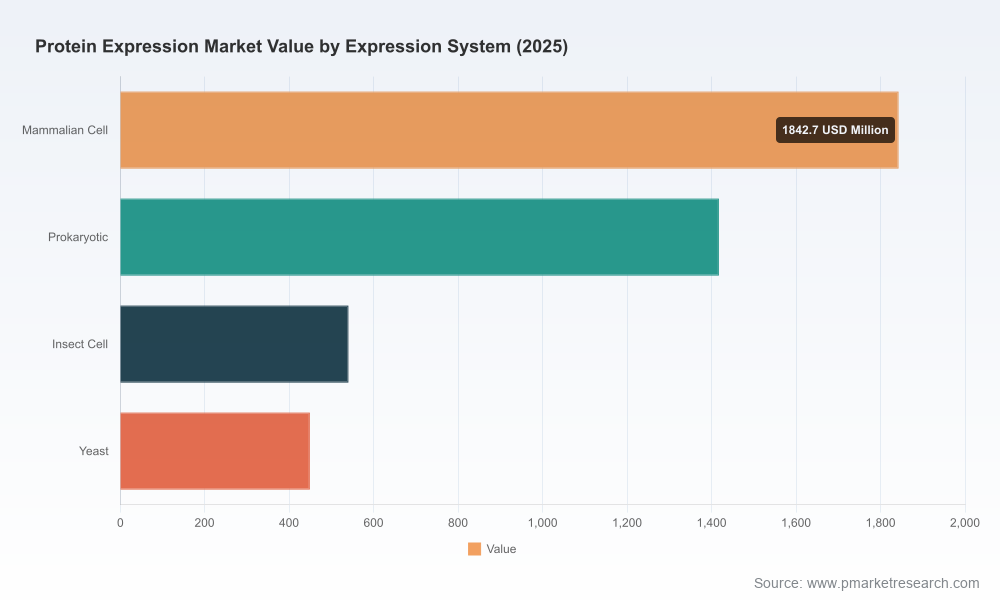

PW Consulting: Protein Expression Market Tops USD 4,250 Million in 2025, Poised for 9.2% CAGR Through 2032

Other |

2026-07-06 13:51:16

As industrial operators, facility managers, equipment OEMs and investors prepare priorities for 2026, compressed air leak detection is moving from tactical maintenance activity to a measurable contributor to energy efficiency, operational resilience and regulatory compliance. PW Consulting’s latest market study — covering 2020–2025 historical performance with a 2026–2032 forecast horizon — provides the actionable intelligence required to shape procurement, product roadmaps and M&A bets in the coming 12–36 months.

Compressed Air Leak Detector Market

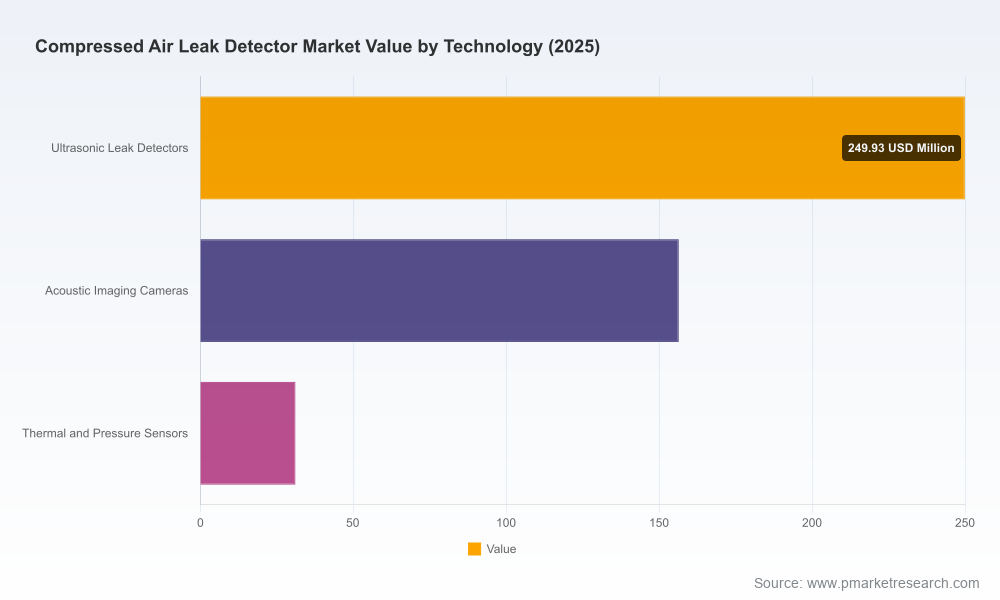

Market scale and growth: The global compressed air leak detector market has expanded materially in recent years, reaching an estimated USD 437.48 Million in 2025. Our model projects continued expansion through the forecast window at a compound annual growth rate (CAGR) of 6.8% (2026–2032), reaching an aggregate market size in the high hundreds of millions (USD) by 2032.

Compressed Air Leak Detector Market

Consolidation and competitive balance: The market demonstrates moderate concentration. The top three vendors account for roughly 42% of market revenues (CR3), while the top five capture about 58% (CR5), leaving meaningful opportunity for specialist players and regional challengers to differentiate through product, services, or channel strategies.

Compressed Air Leak Detector Market

Technology trajectory: Ultrasonic-based tools, acoustic imaging cameras and sensor-integrated thermal/pressure approaches are maturing along parallel paths. Each approach has distinct cost/performance trade-offs that influence buyer selection depending on scale, noise environment and digital integration requirements.

Compressed air systems are often among the most inefficient utilities in industrial facilities. For executive teams focused on energy cost reduction, carbon management, and plant uptime, leak detection represents one of the highest-return operational investments. Our analysis quantifies the link between detection capabilities and energy savings, and — crucially for 2026 planning — it translates those savings into procurement and deployment scenarios aligned to commonly adopted ISO energy and air quality standards.

Cost-to-benefit calibration: Buyers should prioritize devices and programs that deliver reliable localization at low inspection time per asset, backed by standardized energy-savings estimates. The report includes a prescriptive framework to size pilot programs, define ROI thresholds and scale rollouts without disrupting production.

Timing for CAPEX vs OPEX: For asset owners weighing handheld detectors, acoustic cameras, or integrated sensor networks, our guidance shows when CAPEX-intensive imaging solutions justify themselves (e.g., multi-site rollouts, rapid audit timelines) versus phased, handheld-first strategies that defer capital while capturing near-term savings.

Regulatory and certification alignment: With ISO 50001 and ISO 8573-1 increasingly referenced in corporate energy and quality programs, 2026 decisions must embed detection capabilities into compliance pathways. The report maps detector selection to common audit and reporting requirements so teams avoid retrofitting devices to meet certification needs.

We built this study as an operational playbook for leaders who must turn recommendations into measurable outcomes. The full report contains:

Modular implementation guides — from single-line handheld audits to enterprise acoustic imaging programs — with stepwise checklists for procurement, pilot design, data governance and ROI tracking.

Vendor selection criteria and scorecards tailored to common industrial profiles (e.g., high-noise heavy industry, clean-room production, multi-site manufacturing), enabling rapid shortlisting with weighted trade-offs.

Contract and service model templates that align incentives for vendors and buyers — including SaaS monitoring, outcome-linked service agreements and extended warranty considerations for sensor-intensive solutions.

Operational KPIs and reporting templates that integrate energy savings, leak rate trends, maintenance cycles and ISO compliance artifacts so teams can present a consolidated business case to finance and sustainability stakeholders.

The market combines global instrumentation leaders, specialized ultrasound firms and smaller regional manufacturers. Competitive dynamics favor those who can pair detection hardware with software-enabled workflows, credible energy-savings claims and service models for repeat engagements. Representative companies covered in the study include:

Teledyne FLIR — Offers acoustic imaging platforms that combine ultrasonic detection with visual imaging to locate pressurized leaks at extended standoffs. Strong brand, broad OEM channels and integration potential into enterprise thermal imaging fleets.

UE Systems — A specialist in ultrasonic detection with handheld and imaging products that emphasize leak rate estimation and energy saving calculations; long history in acoustics-based condition monitoring.

EXAIR Corporation — Focused on cost-effective handheld ultrasonic detectors; competitive where simplicity, ease-of-use and unit-level affordability are priority procurement criteria.

CS Instruments — European provider with detector and camera offerings that include cost-calculation and ISO 50001 reporting features, appealing to regulated and quality-driven buyers.

Superior Signal Company, SUTO iTEC, LeakMaster, OptiNav and SDT Ultrasound — A mix of regional specialists and innovators addressing niche needs from low-cost handhelds to automated, stationary monitoring solutions.

Several recent market developments underscore shifting competitive priorities: notable M&A (e.g., a major industrial group’s acquisition of a U.S. leak detection specialist in early 2026) and product introductions from established players in 2025–2026 that broaden imaging and automated testing capabilities. These moves accelerate consolidation in system-level offerings and raise the bar for integrated service propositions.

Standards-driven demand: ISO 50001 energy management and ISO 8573-1 compressed air purity standards are increasing the non-financial value of leak detection. Buyers should treat detection not merely as maintenance but as a compliance and risk-management control.

Practical targets: Industry guidance commonly targets leak-related flow losses of 5–10% as a manageable reduction goal; devices and programs must be judged on their ability to reliably achieve and sustain reductions in that band.

Component supply dynamics: Core detector components (MEMS microphones, ultrasonic sensors) have stabilized through 2025–2026, reducing near-term disruption risk. However, firms should still model component lead times into procurement timelines for large-scale rollouts.

Adopt a hybrid deployment path: Run short-cycle handheld audits to capture immediate savings and validate hotspot hypotheses, while piloting acoustic imaging or fixed sensors in high-impact areas where rapid identification and verification accelerate ROI.

Insist on auditable energy-savings methodology: Require vendors to demonstrate energy-savings calculations tied to recognized measurement and verification protocols so that reported gains are finance-ready.

Design modular purchasing: Favor scalable procurement that allows a phased move from capex (hardware) to opex (monitoring-as-a-service) depending on proved program economics after pilot stages.

Evaluate M&A/partnership targets selectively: Given the market’s moderate concentration, strategic acquisitions or distribution partnerships can accelerate access to new geographies or complementary tech stacks. Prioritize targets with repeatable service revenue and data assets.

Build data governance early: Detection programs generate datasets that can inform predictive maintenance, compressor sizing and carbon reporting. Define data ownership, integration and analytics requirements before full deployment.

This briefing is an executive distillation. The full PW Consulting study contains the granular tools and proprietary analyses you will need to operationalize a 2026 program: detailed market scenarios, stakeholder-specific ROI models, vendor benchmarking matrices, procurement and contract templates, and step-by-step deployment playbooks. It also contains fine-grained regional and end-use segmentation, vendor share tables and our proprietary cost-model assumptions — intentionally withheld here to encourage direct engagement with the source report.

For leaders who must prioritize investments in 2026, the guidance in this report translates market growth dynamics (current market size, 2025 baseline and 6.8% forecast CAGR) into executable decisions: what to buy, when to scale, which partners to evaluate, and how to ensure the program produces auditable savings that contribute to both the bottom line and sustainability targets.

PW Consulting is available to brief executive teams and provide workshop-led roadmaps that convert these insights into procurement specifications, pilot plans and investment-grade business cases. For access to the full dataset, vendor-level analysis, and downloadable implementation templates, please visit our report page.

For detailed analysis of this topic, please visit the official page:Compressed Air Leak Detector Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com