Fully Wireless Fire Detection System Market Size, Share, Driving Trends, and Industry Forecast by 2032

Other |

2026-06-30 09:51:52

PW Consulting’s latest Anechoic Chamber Material Market report (base year 2025) offers a focused, action‑oriented view tailored to the priorities of corporate strategy, procurement, and R&D leaders planning for 2026. The market for anechoic chamber materials has moved beyond niche engineering procurement to become a predictable, capital‑intensive ecosystem supporting telecom rollouts, automotive sensing, aerospace testing and broader EMC/compliance activity. Our study combines an independent five‑year historical lens with a forward forecast through 2032, enabling leaders to align investment choices with likely demand and supply dynamics without relying on vendor narratives.

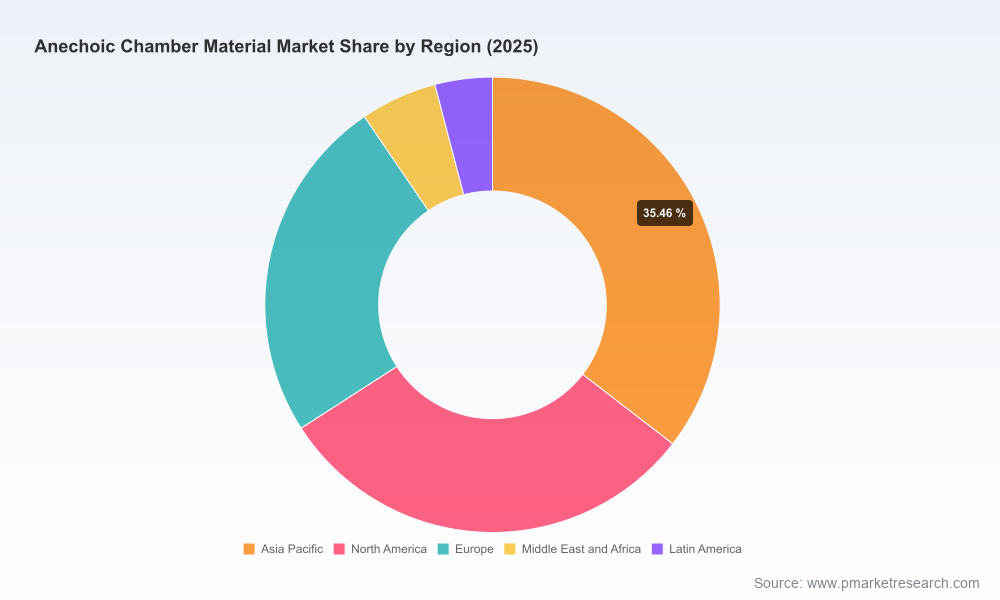

Anechoic Chamber Material Market

Market scale and growth: The report benchmarks total global market size through 2025 and presents a coherent forecast for 2026–2032. Across the forecast window the market expands at a compound annual growth rate (CAGR) of 6.54%, underpinned by continued capital spending on RF and acoustic test infrastructure.

Anechoic Chamber Material Market

Concentration and competitive structure: The market exhibits moderate concentration — our concentration metrics signal a three‑player cluster and a broader five‑player tier that together account for over half of the market value. This structure creates both collaboration and competitive displacement opportunities for mid‑market players and new entrants.

Anechoic Chamber Material Market

Demand inflection points: Multiple end‑use sectors are driving incremental capacity additions and replacement cycles in 2026. These include next‑generation telecom testing, radar and sensor validation for automotive ADAS, and expanded radar production for defense platforms. The timing and scale of these projects are crucial inputs to 2026 procurement and capex plans.

2026 will be a year where procurement windows, certification calendars, and raw material cycles converge — creating both upside and execution risk. Our analysis synthesizes market sizing, supplier benchmarking, and scenario modelling to deliver three pragmatic capabilities for executives:

Timing and prioritization: a calibrated view of when to accelerate capital commitments (e.g., chamber buildouts) versus when to defer or phase purchases to avoid peak raw‑material pricing.

Supplier selection and risk mitigation: a toolkit to assess supplier resilience on raw‑material sourcing, fire and chemical compliance, and modular versus bespoke chamber strategies.

Investment sizing and returns: bottom‑line oriented capex scenarios showing payback and sensitivity to material cost inflation, certification lead times and utilization rates.

Raw‑material exposure: Carbon‑loaded polyurethane and similar foam chemistries remain the dominant substrate for broadband absorbers. The polyurethane supply chain is dependent on TDI and polyol feedstocks. Recent constraints and price volatility in TDI markets have already transmitted into foam pricing and will continue to influence sourcing strategies and build‑vs‑buy economics in 2026.

Regulatory and safety hurdles: Fire performance certification and chemical compliance are non‑negotiable for institutional and public sector projects. Growing emphasis on standards such as ASTM E84 class ratings, and REACH/ROHS restrictions on chemical content, means lead times for certified material and certified installers are a gating factor for project scheduling.

Material innovation and substitution: We tracked product introductions and certification milestones in 2024–2026 (including new polymer‑based RF absorbers entering the market). These innovations create opportunities to reduce cost, improve durability and address regulatory constraints — but they also raise adoption and qualification risk for OEMs and test labs.

Hybridization and modular design: Combining foam absorbers with ferrite tiles and other tiles continues to be a pragmatic route for balancing performance, weight, and fire performance; this is reflected in rising preference for hybrid installation approaches in retrofit and new‑build projects.

The competitive map blends legacy materials expertise with turnkey chamber system capability. Several established providers combine in‑house absorber manufacturing with full chamber integration; others focus on specialized absorber technology or modular systems. Key market participants we profile include long‑standing absorber manufacturers and chamber integrators across the US, Europe and Asia. Our vendor reviews examine product portfolios, certification track records, geographic footprint, and service capabilities — critical inputs for supply selection in 2026.

Technology‑led absorber specialists that emphasize high‑performance pyramidal and hybrid formulations and who offer turnkey chamber solutions backed by engineering services and long service histories.

Global chamber integrators that pair mechanical and RF/acoustic design expertise with supply chain coordination to deliver on tight project schedules.

New entrants and materials specialists that target cost or compliance niches, notably polymer‑based RF absorbers and high‑performance ferrite composites.

Recent market movements reinforce these themes: prominent trade show showings by absorber technology providers; launches of new polymer absorbers intended to reduce cost and address flame performance; third‑party fire certification achievements for absorber foams; and notable increases in testing capacity by radar OEMs — all of which directly influence absorber procurement and lead times.

Demand model with scenario branches: deterministic base case and tail scenarios that stress test demand against 5G infrastructure timelines, automotive sensor certification calendars and defense radar procurement waves.

Supply‑chain map and raw‑material sensitivity analysis: price pass‑through modeling for polyurethane feedstocks, lead‑time overlays and supplier concentration risk indices.

Vendor scorecards and procurement playbook: standardized evaluation criteria (technical, commercial, compliance, delivery) plus RFP language and contract clauses to hedge price and lead‑time risk.

Capex and ROI templates: build‑vs‑buy calculators for in‑house absorber fabrication, chamber construction phasing strategies and utilization thresholds to justify investment.

Compliance checklist and certification road‑map: actionable steps to secure ASTM/EN/REACH/ROHS compliance and to plan test schedules around certification bottlenecks.

M&A and partnership guidance: diligence checklists and valuation heuristics for targets in absorber manufacturing, chamber integration, and complementary services.

Lock in multi‑tier supplier contracts now, with indexed pricing and minimum volume commitments — but retain optionality for alternative chemistries. The market’s mid‑single‑digit CAGR creates growth runway, yet raw‑material tightness can spike costs.

Prioritize certified materials and certified installers for any public sector and defense projects. Certification lead times are a project‑level risk; securing certified inventory ahead of program start dates mitigates schedule slippage.

Invest selectively in modular chamber components and hybrid absorber approaches to shorten installation cycles and reduce exposure to single material class volatility.

Evaluate strategic partnerships with absorbers that combine materials IP and chamber integration capability — this can accelerate time‑to‑market for differentiated test offerings while keeping capital intensity manageable.

Build a near‑term R&D agenda focused on material substitution, fire performance, and recyclability. Early adoption of new certified polymer absorbers may deliver a sustainable cost advantage if paired with rigorous third‑party validation.

For C‑suite and board teams, the value lies in converting market intelligence into executable projects. Use our capex templates and scenario outputs to present defendable investment cases, to stage procurement actions across 2026–2027, and to define KPIs for supplier performance and certification milestones. Procurement and engineering teams should adopt the vendor scorecards to accelerate vendor shortlists and to harmonize RFP evaluation criteria across cross‑functional stakeholders.

This overview highlights the strategic lines of sight necessary for 2026 decision‑making while preserving the detailed segment tables and supplier financials that underpin project‑level commitments. The full PW Consulting Anechoic Chamber Material Market report includes granular segment forecasts, regional demand builds, detailed vendor benchmarking and downloadable procurement templates. Senior executives and project leads evaluating chamber investments, supplier partnerships, or M&A options should review the full dataset to convert these insights into binding decisions.

To obtain the complete report and the supporting models, including the complete breakdown of segment performance and supplier benchmarking data, please visit our research portal or contact PW Consulting’s Industry Practice for a briefing and a tailored dataset export.

For detailed analysis of this topic, please visit the official page:Anechoic Chamber Material Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com