Market Dynamics Driving North America Capillary Blood Collection Industry Growth

Health |

2026-06-30 13:39:06

PW Consulting’s new Dc Ac Hybrid Solar Pump Market report is a practical intelligence product designed to convert market visibility into decisive action. As the industry navigates accelerating demand, material cost volatility, and shifting policy incentives, the choices made in 2026 will determine competitive positioning for the rest of the decade. This briefing highlights the report’s strategic value for corporate leaders, investors, and public‑sector program managers — and explains why accessing the full dataset and scenario models is essential before finalizing 2026 capital plans.

Dc Ac Hybrid Solar Pump Market

The hybrid solar pump market has moved from early adoption to structured growth. After a rapid recovery and expansion through the early 2020s, the market size reached USD 970.31 Million in our base year (2025). Under a set of conservative to moderate assumptions, the market is projected to grow at a compound annual rate of 11.28% during the 2026–2032 forecast window, reaching USD 2,052.95 Million by 2032. Historical trajectories through 2023–2025 show steady, demand‑led increases that underpin our confidence in the forecast range.

Dc Ac Hybrid Solar Pump Market

Two takeaways are immediate for 2026 planning: (1) the market scale and growth rate are now large enough to support dedicated product lines, distribution investments, and after‑sales networks; and (2) margins and deployment economics will be materially affected by upstream input pricing and evolving policy frameworks, which makes timing and procurement strategy critical.

Dc Ac Hybrid Solar Pump Market

Raw material pressure: Early‑2026 input cost cycles — notably a surge in silver prices — are reintroducing inflationary pressure into PV module and system costs. In many cases, raw materials constitute the majority of manufacturing operating expenses, and photovoltaics remain the dominant cost item in hybrid system bills of materials. That dynamic will compress margins for low‑value, high‑volume suppliers and reward OEMs that can secure supply, redesign BOMs, or vertically integrate procurement.

Incentive evolution: North American and other major markets continue to calibrate direct incentives and tax credits. Existing U.S. residential and clean‑energy incentives, alongside extensions under federal measures through the late 2020s, create windows for accelerated residential and distributed commercial adoption — but also add complexity to product certification and warranty packaging. Conversely, local policy changes (for example, alterations to property tax treatment in specific jurisdictions) will reshape total cost of ownership calculations for some buyer segments.

Technology convergence: Hybrid architectures — combining DC‑first solar input with AC grid or generator backup and smart MPPT and VFD control — are moving from niche to mainstream. The competitive premium now attaches to integrated control platforms, remote telemetry, and modular designs that simplify field installation and reduce service intervals.

This report is built for executives who must translate market signals into executable programs. Key practical deliverables include:

Validated market sizing and a transparent forecasting engine (2026–2032) that you can parameterize for alternative macro and commodity scenarios.

Scenario‑based cost models highlighting the sensitivity of system pricing and installer margins to silver, polysilicon, and shipment cost swings — equipped with break‑even and payback analytics for typical buyer archetypes.

Go‑to‑market playbooks for OEMs and distributors: channel design, bundling strategies (hardware + financing + service), and recommended warranty lengths tied to lifecycle cost targets.

Deployable supplier and procurement scorecards that enable risk‑weighted sourcing decisions and near‑term hedging tactics to mitigate raw material shocks.

Regulatory impact matrices and a calibration guide for capturing available tax credits and incentive schemes while preparing for phase‑outs or local policy reversals.

Benchmarked commercial models and financial KPIs for valuation, M&A screening, and JV diligence — including a prioritized list of capability gaps that make targets strategically attractive.

The market remains competitively dynamic: concentration metrics indicate that top players exert a meaningful but not dominant influence on pricing and technology direction, which preserves room for nimble challengers and differentiated product strategies. Our competitive synthesis focuses on product architecture, channel reach, and control systems — the axes that determine winning propositions in hybrid deployments.

Grundfos Holding A/S (Bjerringbro, Denmark, https://www.grundfos.com) — Leader in integrated submersible solutions with inverter‑based SQFlex platforms that run on multiple inputs. Strength: cross‑domain engineering that enables flexible grid‑connected and off‑grid hybrids, supported by strong global service channels.

LORENTZ GmbH & Co. KG (Henstedt‑Ulzburg, Germany, https://www.lorentz.de) — Pure‑play solar pumping specialist with deep expertise in off‑grid systems and hybrid functional integration. Strength: focused product roadmap and strategic partnerships that accelerate field deployment and system reliability.

Zhejiang Dingfeng (DIFFUL) (Zhejiang, China, https://www.diffulpump.com) — Innovative AC/DC hybrid manufacturer emphasizing dual‑input modes and controller R&D. Strength: rapid product updates and technical matching content that support installers and OEM partners (recent catalog and controller content published March 2026).

HYBSUN Solar (China, https://www.hybsun.com) — Focused on BLDC motor platforms and MPPT‑centric controllers for borehole and surface pumps. Strength: low operating cost designs and modular control electronics suited to rural electrification projects.

VEICHI Electric (China, global, https://www.veichi.com) — Offers hybrid systems with VFD and MPPT integration and practical warranty packages. Strength: competitive pricing and strong controller feature sets for agriculture and livestock markets.

Deye (Zhejiang, China, https://www.deyesolar.com) — Hybrid designs with integrated variable frequency drives and inverter expertise. Strength: product integration that simplifies installer workstreams under variable power conditions.

Taizhou Edwin (EDWIN PUMP) (Taizhou, China, https://www.edwin-pump.com) — Wide portfolio across surface and submersible categories and global distribution. Strength: customization and export experience across multiple application segments.

Rafsun (China, https://www.rafsun.com) — Dual‑power hybrid submersibles with multiple operating modes for continuous operation. Strength: practical all‑day hybrid operation features that support critical water services.

Samking Pump (China, https://www.samkingpump.com) — Broad model range and investments in brushless DC and dual‑shielded motor technology. Strength: scale and model diversity to serve diverse application needs.

Oswal Pumps (India, https://oswalpumps.com) — Strong regional OEM with export capabilities and hybrid offerings. Strength: cost position and local market knowledge in high‑volume irrigation segments.

Recent strategic moves — from DIFFUL’s 2026 technical updates to LORENTZ’s partnership activity — underscore two ongoing themes: consolidation of technical standards around MPPT/VFD integration and the deepening of commercial partnerships (distribution, water services, and finance). These moves matter for incumbents and new entrants because they accelerate customer adoption while raising the bar on integration and after‑sales expectations.

Prioritize supply security and flexible procurement contracts for PV modules and critical electronic components. Hedging exposure to silver and polysilicon is now a material risk mitigant for manufacturers and large project developers.

Invest in control‑software and remote monitoring as differentiators. Services linked to telemetry, predictive maintenance, and outcome‑based SLAs will command premium pricing over commoditized hardware.

Consider bolt‑on M&A for companies with proven field service networks or proprietary MPPT/VFD IP instead of bidding for volume‑only targets. The market rewards integrated value chains that reduce installed cost and O&M friction.

Architect financing and warranty packages to capture residential and distributed commercial incentives. With tax credits and policy windows changing, the right finance product can unlock otherwise latent demand.

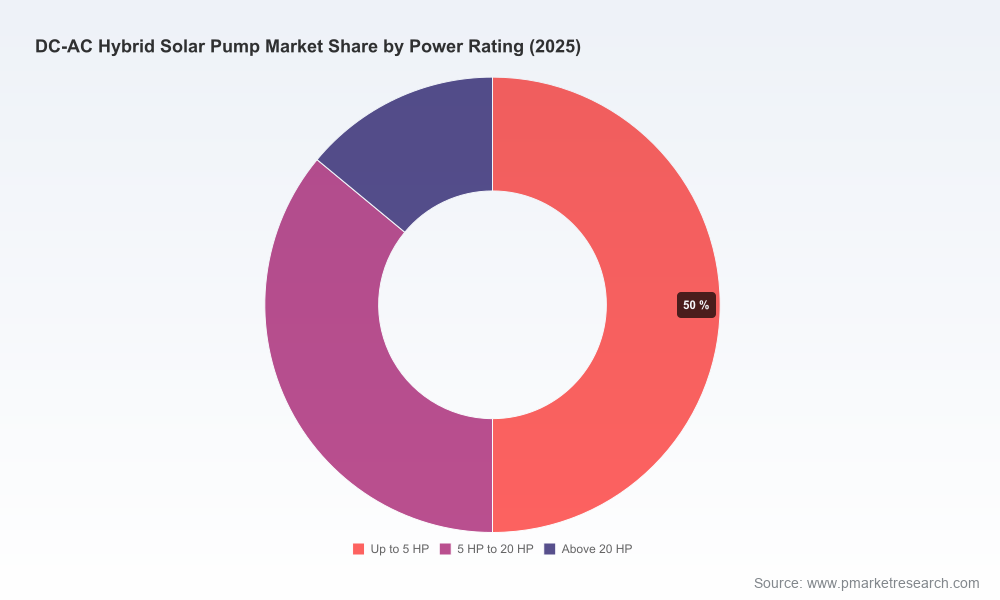

The report synthesizes a 2020–2025 historical dataset with a scenario‑driven forecast for 2026–2032. Coverage includes: market sizing, segmentation by geography, power rating and end‑use application; vendor benchmarking and CR metrics; component‑level cost breakdowns; and regulatory sensitivity modeling. For this release we are deliberately following a “preview” approach: we present headline market sizes, trajectory and strategic conclusions here, but have withheld granular region‑by‑region, application, and power‑rating split tables and the full company scorecards. These withheld datasets are part of the complete report package and the downloadable financial model on the report page, which is essential for transaction diligence or detailed commercial planning.

For 2026 corporate roadmaps, the priority is twofold: secure your supply and cost base against commodity swings, and invest in product and service features that materially reduce installation and O&M friction. The market’s compound growth trajectory to 2032 creates attractive upside for incumbents and new entrants who can combine technical differentiation with disciplined procurement and innovative commercial models. PW Consulting’s Dc Ac Hybrid Solar Pump Market report equips leaders with the datasets, models, and playbooks necessary to convert that upside into durable competitive advantage — but timing matters. Reviewing the full dataset now will influence procurement, R&D, and M&A choices that lock in 2026 outcomes.

Access the full report for granular regional and application breakdowns, downloadable financial models, and vendor scorecards that are indispensable for 2026 program execution.

For detailed analysis of this topic, please visit the official page:Dc Ac Hybrid Solar Pump Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com