Minimally Invasive Surgery Market Size, Share, Trends, and Industry Forecast by 2033

Other |

2026-06-08 10:18:04

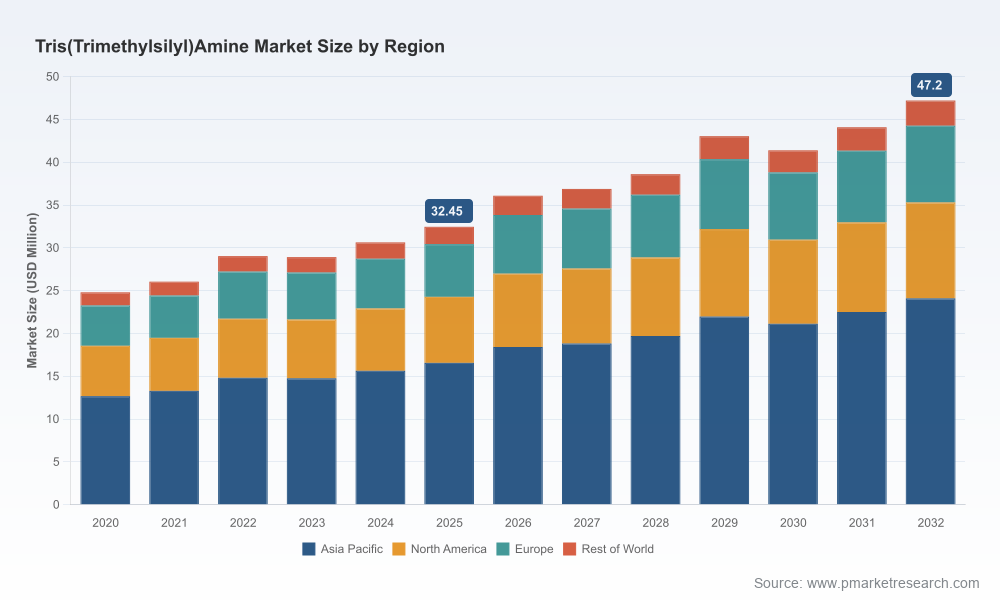

PW Consulting’s latest market brief on Tris(trimethylsilyl)amine presents a clear, actionable line of sight for executive decision‑making in 2026. At a macro level, the market recorded sustained expansion through the early 2020s and reached an estimated USD 32.45 Million in 2025. Our forecast model projects continued growth into the forecast window (2026–2032) at a compound annual growth rate (CAGR) of approximately 5.5%, with the market trending toward a materially larger size by 2032. These headline figures reflect a mix of steady demand from advanced electronics processing and fine‑chemicals synthesis, tempered by regulatory and supply‑side considerations that will determine competitive positioning over the next planning cycle.

Tristrimethylsilylamine Market

Timing: 2026 is a pivot year for firms that need to convert province‑level R&D traction into commercially scalable supply. The market’s steady CAGR signals opportunity, but returns will accrue to players who align capacity, specification control, and regulatory compliance ahead of volume inflection points.

Tristrimethylsilylamine Market

Margin dynamics: Sourcing for high‑purity electronic grades and advanced materials applications is driving a premiumization trend. Suppliers who can guarantee reproducible spec and on‑time delivery will command superior margin and contractual leverage with OEMs and research customers.

Tristrimethylsilylamine Market

Risk management: Regulatory clarity (including REACH registration) reduces uncertainty, but also raises the bar for documentation, supplier audits, and end‑use disclaimers. Firms ignoring upstream compliance and downstream labeling conventions face avoidable commercial friction.

Application pull from advanced manufacturing: Demand is concentrated where precision surface chemistry is mission‑critical—atomic layer and chemical vapor deposition processes, specialty organosilicon synthesis, and targeted surface modification workflows. These end uses favor consistent purity and batch traceability over commodity cost reduction.

Supplier landscape and concentration: The supply base is characterized by a mix of global life‑science distributors and niche silicon‑chem specialists. Market concentration metrics indicate that a minority of suppliers account for a substantive share of available commercial supply, creating both opportunity for scaling incumbents and openings for focused challengers.

Regulatory and labeling environment: Tris(trimethylsilyl)amine is registered under EU REACH, and major suppliers maintain product labeling that restricts use to research applications. These constraints influence commercial pathways to broader industrial adoption and necessitate careful regulatory engagement for firms seeking to commercialize beyond RUO (research use only) channels.

Customer segmentation: The buyer base ranges from research labs purchasing small pack sizes for method development to materials manufacturers requiring scalable, specification‑driven supply. Commercial success in 2026 will depend on tailoring offers across this spectrum while maintaining cost discipline.

Proprietary, model‑driven market sizing and a granular forecast model (2026–2032) that can be licensed and integrated into corporate planning tools.

An executable go‑to‑market playbook covering product segmentation, packaging and logistics optimization for both lab and commercial customers, and pricing scenarios tied to purity tiers and contract terms.

Supply chain stress tests that map single‑source exposures, alternative sourcing pathways, and contract manufacturing options, including capex and lead‑time implications for scale‑up.

Regulatory roadmap detailing REACH implications, label‑to‑application risk assessments, and a compliance checklist that supports faster time‑to‑market for non‑RUO commercialization strategies.

Investor and M&A playbook with valuation sensitivity to purity mix, customer concentration, and backward integration potential; includes example deal structures and integration risk checklists.

Competitive benchmarking with supplier heat maps, capability gap analysis, and suggested partnership matrices designed to accelerate access to key end‑markets.

Primary research appendix summarizing interviews with procurement and R&D buyers, and an assumptions log for the forecast model—built to be auditable and to support scenario planning workshops.

The market features two broad supplier archetypes: large scientific distributors that leverage global logistics and catalogue penetration, and specialist silicon‑chem firms with deep technical know‑how in advanced materials. Key participants include established life‑science distributors that offer standard pack sizes and research‑grade purity, alongside specialist manufacturers that target advanced materials synthesis and surface modification markets.

Large distributors: Their strengths are breadth of catalogue, global fulfilment capability, and existing relationships with academic and industrial labs. They typically market research‑grade product SKUs and are effective at serving decentralized, small‑volume buyers.

Specialist suppliers: These players emphasize technical support, bespoke grades, and applications expertise—particularly for advanced materials and process integration in electronic applications. Their edge is in purity control and the ability to co‑develop formulations with OEMs.

Implication: Buyers seeking repeatable, high‑yield performance (for example in ALD/CVD lines) will prefer suppliers that can commit to tighter spec control and documented material performance. Conversely, price‑sensitive, one‑off research purchases will continue to flow through catalogue channels.

Concentration metrics show that a limited set of suppliers holds a meaningful share of market availability. This creates asymmetric negotiation power for those firms but also elevates near‑term entry economics for challengers that can address niche specification gaps or offer integrated services (e.g., technical application support, broader product suites). The strategic playbook for 2026 therefore focuses on either consolidating technical leadership or on differentiation through customer intimacy and application‑led services.

Segment and price by deliverable value, not by cost alone: Move beyond pack‑size pricing to value‑based contracts that reward consistent purity, batch traceability, and technical support tied to ALD/CVD performance metrics.

Invest in regulatory and documentation readiness: Convert RUO offerings into broader commercial use by proactively addressing REACH dossiers, end‑use declarations, and application safety data to minimize downstream commercialization friction.

Hedge supply with multi‑tier sourcing: For buyers, secure a primary supplier with a specialist backup to protect scaled processes; for suppliers, consider toll‑manufacturing partnerships to scale without prohibitive capital expenditure.

Pursue targeted partnerships with device and materials OEMs: Co‑development agreements that tie product specifications to process outcomes shorten buying cycles and create stickiness that is defensible against catalogue competitors.

Use M&A selectively to buy technical depth or fill critical capacity gaps: The most accretive deals are those that add purity control, analytical capability, or application engineering teams—assets that high‑volume distributors typically lack.

Our report is structured as a decision‑ready toolkit: strategic diagnosis, an auditable forecast model, supplier and customer playbooks, and an M&A decision framework tailored to the tris(trimethylsilyl)amine ecosystem. For executive teams planning 2026 initiatives, we offer a rapid activation package that includes a one‑day executive workshop, a customized sensitivity analysis of your current book of business, and a targeted supplier due diligence sprint.

This brief highlights the strategic contours and actionable options for stakeholders in the Tris(trimethylsilyl)amine market. For decision makers requiring the full dataset, granular regional and application segmentation, supplier revenue breakdowns, and the complete financial model, please access the full PW Consulting market report on our website. The detailed segmentation tables and downloadable model are intentionally gated to preserve commercial value and to ensure clients receive an auditable, enterprise‑grade dataset to inform 2026 capital and commercial decisions.

Contact PW Consulting to schedule a briefing, license the forecast model, or commission a tailored advisory engagement focused on operationalizing these recommendations.

For detailed analysis of this topic, please visit the official page:Tristrimethylsilylamine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com