SaaS-Based IT Security Market Size, Growth Trends, and Key Players Forecast 2024-2031

Other |

2026-06-17 14:37:26

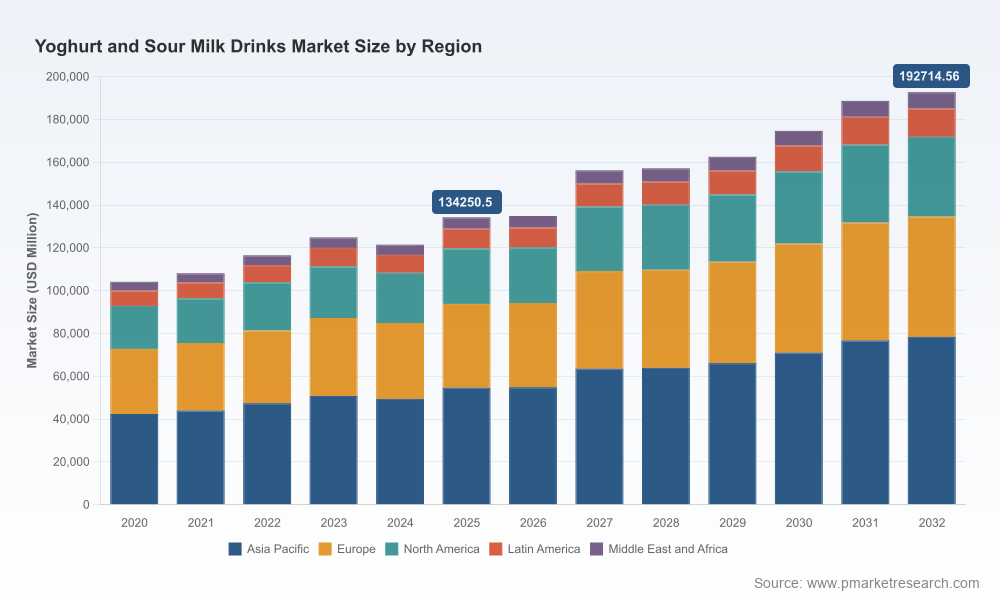

PW Consulting’s new market study on Yoghurt and Sour Milk Drinks reframes the strategic choices facing manufacturers, retailers and investors as they enter 2026. The category has demonstrated resilient expansion since 2020, with total industry revenue rising steadily to a 2025 base of approximately USD 134.3 billion (base year 2025). Under our central forecast scenario the market grows at a compound annual growth rate (CAGR) of 5.3% over the 2026–2032 horizon, reaching substantively higher levels by 2032. These macro dynamics — combined with mounting regulatory change, input-cost volatility and accelerating product innovation — create a high-opportunity, high-complexity operating environment for the coming 18–36 months.

Yoghurt And Sour Milk Drinks Market

Action orientation: the report translates top-line growth into a succinct set of strategic imperatives and operational levers that commercial teams can deploy in 2026 (product portfolio, pricing, channel mixes, and promotion cadence).

Yoghurt And Sour Milk Drinks Market

Risk mitigation: it quantifies the impact of near-term supply shocks and regulatory shifts so procurement, legal and finance functions can prioritize hedging, reformulation and labeling updates ahead of enforcement cycles.

Yoghurt And Sour Milk Drinks Market

Deal readiness: we overlay competitive positioning and concentration metrics with valuation and integration sensitivity to generate a short-list of M&A and partnership targets for buyers and private equity.

Go-to-market playbook: actionable retailer negotiation levers, e-commerce conversion frameworks and SKU rationalization templates to lift margins without eroding distribution.

The category’s historical momentum (2020–2025) establishes a clear baseline for corporate planning. A mid-single-digit CAGR through 2032 under our central case points to steady but heterogeneous opportunity: pockets of premiumization, probiotic-led expansion, and plant-based substitution will outperform commoditized, price-sensitive SKUs. Firms that treat 2026 as a year to lock strategic bets — on innovation, supply resilience and channel economics — will capture disproportionate share over the forecast window.

Consumer health and functionalization: demand is markedly shifting to products that carry clear digestive-health claims (probiotics), protein fortification and reduced-sugar positioning. These attributes are increasingly table stakes for product launches and promotions.

Input-cost volatility: dairy input markets are tighter — global milk powder prices averaged materially higher in Q1 2026, reflecting supply constraints. This amplifies the urgency for procurement strategies (forward buying, index-linked contracts) and price-pass mechanisms.

Regulatory inflection points: the EU’s front-of-pack Nutri-Score mandate (effective January 2025) and updated US Nutrition Facts requirements for fermented dairy (compliant by 2025) are now live considerations for labeling, formula adjustments and retailer listings.

Trade dynamics: new tariffs and trade policy shifts — for example, recently announced import duties affecting some cross-border yogurt flows — reframe sourcing and export plans, particularly for companies with pan-regional supply footprints.

Food safety and brand risk: high-profile recalls remain a sector vulnerability and require rapid-response protocols. Past incidents illustrate how short-term supply disruptions can translate into protracted revenue and reputation costs if not managed decisively.

The competitive structure is moderately concentrated: the three-largest players account for roughly one-third of the market (CR3 ≈ 32.4%), while the top five approach the low‑forties (CR5 ≈ 41.8%). That configuration favors global champions with strong brand equity, scale in procurement and broad route-to-market capabilities, while leaving meaningful room for regional specialists, private-label players and premium niche entrants.

Danone (Paris, France): A global leader across fermented dairy and probiotic lines. Recent launches emphasize gut-health positioning and geographic expansion of premium variants — moves that reaffirm R&D-centered competitive defense in Europe and Asia.

Lactalis (Laval, France): Major industrial-scale producer with strength in branded and private-label portfolios. Recent low-sugar SKU introductions align with retailer health trends and margin-protection objectives.

Chobani (New York, USA): A disruptive growth story from Greek-style roots, aggressive in drinkable and protein-enhanced formats. Its mid‑2025 product launches underline a push to capture higher-value, on‑the‑go consumption occasions.

Yakult Honsha (Tokyo, Japan): Probiotic-focused specialist; capacity expansion in South Asia signals a strategic pivot to fast-growing emerging markets where consumption per capita is still rising.

Fage, Nestlé, Arla, General Mills, Mondelez, Stonyfield, Siggi’s, Forager Project: Each plays a distinct role — from authentic Greek skyr exportation and broad-based FMCG scale, to organic, premium and plant-based niches. Collectively these players sustain innovation and channel differentiation across geographies.

Recent company activity (product launches focused on probiotics and protein, plant-based innovations showcased at trade shows, and capacity expansions) points to a bifurcating market: premium, differentiated SKUs and functional claims versus cost-competitive, volume-oriented offerings that target mass channels.

Top-line market size, historical time series (2020–2025) and detailed forecasts (2026–2032) across demand scenarios.

Segment-level analysis by region, product type and distribution channel — with demand drivers, margin analysis and retailer economics.

Competitive benchmarking: 12+ company profiles, capability heat maps, and a 90-day watch-list of material moves.

Commercial playbooks: SKU rationalization templates, e-commerce conversion paths, retailer negotiation levers, and promotional ROI matrices.

Procurement and manufacturing playbook: input-price sensitivity models, hedging strategies, and capacity-siting decision tools.

Regulatory and compliance checklist aligned to Nutri-Score, FDA label requirements, and major export-market duties.

M&A and investment dashboards: valuation sensitivities, integration risk checklists and prioritized target archetypes.

Scenario stress tests capturing raw-material shocks, regulatory price pass-through, and demand-shift outcomes for 2026 planning.

Note: this release intentionally omits the granular segment-level numbers and splits that underpin our strategic recommendations. The full dataset, granular tables and interactive dashboards are available in the complete report on our website.

Reprice with discipline: implement staged price increases tied to transparent input-cost indices, paired with promotional rationalization to protect margins without sacrificing velocity.

Lock in dairy inputs: expand forward-purchasing windows and negotiate index-linked supplier contracts to dampen short-term milk powder volatility.

Prioritize processor flexibility: invest in SKU-flexible fill lines and modular plants to switch between spoonable, drinkable and alternative-base products quickly.

Accelerate label & formula compliance: complete Nutri-Score and Nutrition Facts remediation now to avoid listing disruptions and retailer de-listing risks.

Double-down on functional innovation: focus R&D on clinically backed probiotic strains, clean-label sugar reduction and protein fortification — these yield favorable shelf-space economics.

Refine channel strategy: rebalance assortment by channel (brick‑and‑mortar vs e-commerce vs convenience) using ABCSKU tools to prioritize high-margin, high-turn SKUs.

Targeted M&A: pursue bolt-on acquisitions to secure regional manufacturing, local brands with high consumer trust, or plant-based capability where margin pools are attractive.

Contingency & crisis playbook: strengthen traceability, recall protocols and communications playbooks to minimize brand damage and shorten recovery times.

Our analysts combine category economics, on-the-ground channel intelligence and proprietary modeling to convert headline growth into executable plans. For firms evaluating portfolio moves, pricing actions, or supply-chain reconfiguration, our advisory teams deliver tailored playbooks aligned to the 2026 operating calendar — from six‑month pilot sprints to full-scale rollouts.

To access the full report (including all segment-level tables, company scorecards and interactive scenario models) and to commission a bespoke executive briefing, please visit our report page or contact your PW Consulting account representative. The full dataset is the definitive basis for any 2026 strategic commitment in this category.

For detailed analysis of this topic, please visit the official page:Yoghurt And Sour Milk Drinks Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com