Auto Detailing Boca Raton: The Complete Guide to Keeping Your Vehicle Looking Brand New

Other |

2026-07-03 10:56:50

PW Consulting’s latest Collector Auto Insurance Market report (base year 2025; historical 2020–2025; forecast 2026–2032) delivers a decision-grade synthesis for insurers, investors, distributors and ecosystem partners planning materially in 2026. The global market — measured in USD (Million) — has expanded from a clearly differentiated niche in 2020 to a multi‑billion dollar specialty vertical by 2025, driven by hobbyist ownership patterns, rising asset values for collectible vehicles and evolving distribution models. Our bottom‑line forecast at a compound annual growth rate (CAGR) of 6.5% through 2032 underpins the report’s strategic scenarios and investment roadmaps.

Collector Auto Insurance Market

Resilience and growth: Collector auto insurance has outperformed many traditional personal lines niches in recent years, growing consistently from the historical period into our 2025 base and projecting continued expansion across the 2026–2032 forecast horizon.

Collector Auto Insurance Market

Asset-as-insurance risk: Collectible vehicles combine investment-grade appreciation with idiosyncratic risk profiles (low mileage, storage and transport exposures, event/concours participation). Underwriting and claims differ materially from mass-market auto insurance, creating differentiated margin pools for specialist providers.

Collector Auto Insurance Market

Distribution transformation: The rise of dedicated marketplaces, dealer consignment platforms and digital broker channels is creating important new points of contact — and new partnership opportunities — for specialty insurers that can adapt product, underwriting and onboarding workflows.

Data & regulatory complexity: Accelerating use of telematics, marketplace analytics and customer data is creating both business intelligence upside and heightened compliance exposure (notably recent state privacy developments). Effective data governance is now a core go‑to‑market enabler, not just a back‑office obligation.

Robust market sizing and scenario forecasts across the 2026–2032 horizon, including base-case, upside and stress scenarios keyed to macro and hobbyist demand assumptions (figures expressed in USD, reporting unit: Million).

Actionable competitive intelligence: deep company profiles, benchmarking matrices and go‑to‑market playbooks for incumbent specialists, carrier partners and distributor alliances.

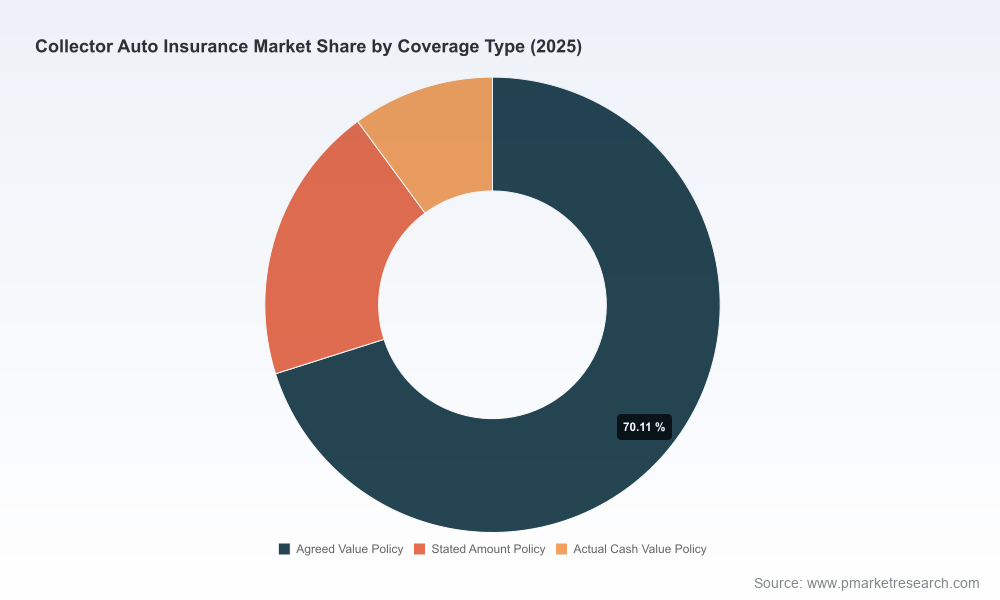

Underwriting and product playbooks: comparative analysis of agreed‑value, stated amount and cash‑value constructs with recommended pricing ladders, endorsement templates and operational triggers for new acquisition coverage and transit exposure.

Distribution and channel blueprints: templates for marketplace integration, affinity partnerships, dealer and auctionhouse arrangements, plus a prioritized list of partner archetypes and negotiation guidance.

Claims and loss‑adjustment frameworks: best‑practice processes for valuation disputes, restoration validation and specialty parts sourcing to protect margins and policyholder satisfaction.

Regulatory and data privacy playbook: state‑level risk mapping, required controls for usage‑based or telematics programs, and incident response procedures tailored to the unique telemetry and provenance data of collector vehicles.

M&A, JV and partnership decision support: valuation benchmarks, integration risk checklists and synergy capture plans designed for 100‑, 365‑ and 1,000‑day horizons.

Toolkits and templates: financial model spreadsheets, KPI scorecards, underwriting checklists and an executable 12‑month roadmap translated into a 100‑day tactical sprint for go‑to‑market or integration activity.

Specialist leaders: Established specialty providers remain the market’s reference points for agreed‑value underwriting, hobbyist community engagement and claims expertise. These firms have built durable brand equity through decades of focused product design, restorations knowledge and event sponsorship.

Incumbent insurers and HNW solutions: Global insurers treating collector coverage as part of their HNW portfolio offer a different risk/return tradeoff — premium scale and distribution reach versus specialized servicing that collectors value (e.g., valuation adjudication, restoration networks, transport coverage).

Distribution partnerships as growth levers: Recent strategic alliances highlight the evolving route‑to‑market. For example, a prominent specialist announced expanded access via a major national carrier partnership announced in late 2025, positioning its products for broader distribution starting in 2026. Separately, another specialist executed a preferred provider arrangement with a leading online collector marketplace in early 2026, integrating protection at point-of-sale.

Concentration and competitive implications: The market exhibits moderate concentration among the top firms (CR3 and CR5 metrics indicate that leading players hold meaningful shared influence but do not create immovable barriers to entry). This structure rewards focused scale — either via organic growth, distribution partnerships or targeted consolidation.

Customer experience as moat: High satisfaction across long-tenured collectors arises from trusted valuation processes, restoration‑savvy claims handling, and community engagement (events, clubs, content). New entrants that cannot replicate those capabilities face higher acquisition and churn costs despite potential digital efficiencies.

State privacy laws are moving from edge case to business‑critical. Recent updates require careful mapping of marketing, analytics and telematics data use against state consent, deletion and opt‑out frameworks. This is material for any insurer deploying usage‑based features or marketplace integrations.

Enforcement actions targeting data collection and monetization practices have increased the commercial and reputational risk associated with third‑party analytics suppliers. Contractual controls, data lineage and consumer‑facing disclosures must be hardened as a precondition to any telematics or data‑sharing strategy.

Regulatory change is asymmetric across jurisdictions. A centralized compliance playbook with flexible modules for state‑level variance is the pragmatic control architecture for players planning multi‑state expansion in 2026.

Lock in distribution partnerships early: Prioritize integrations with marketplaces, auction platforms and dealer networks to capture buyers at point‑of‑transaction. Structure trials that share risk and test conversion economics before nationwide rollouts.

Pursue capability M&A selectively: Acquire restoration‑savvy claims teams, valuation specialists or digital onboarding technology to compress time‑to‑competency and protect the customer experience that drives retention.

Design hybrid product architectures: Blend agreed‑value certainty with flexible endorsements for new acquisitions and limited usage events. Test premium elasticity across collector buyer segments rather than applying a mass‑market pricing rubric.

Operationalize data governance: Implement a privacy‑first telemetry program with tiered consent, robust vendor controls and a consumer education component. This reduces regulatory fragility and preserves the ability to monetize telematics insights.

Differentiate on claims and restoration: Invest in a certified‑restorer network, standardized restoration documentation and expedited parts procurement to shorten settlement cycles and protect customer lifetime value.

Run scenario‑based capital planning: Use the report’s scenario suite to stress test loss volatility from event cancellations, supply chain bottlenecks for parts, and rapid valuations swings driven by market narratives.

Measure the right KPIs: Track vintage vehicle tenure, restoration claim frequency, valuation dispute incidence, conversion rates from marketplace referrals, and partner economics (CAC/LTV) rather than only standard personal lines metrics.

Tactical playbooks convert insight into action: the report includes executable 100‑day sprints for partnership pilots, pricing experiments and telematics governance implementations tailored to carrier, MGA and broker models.

Decision-ready financial models: customizable templates allow teams to size opportunities, model capital requirements and evaluate M&A return profiles under multiple growth scenarios.

Competitive playbook and watchlist: curated intelligence on specialist firms and distribution platforms enables rapid response to marketplace moves and partnership opportunities.

Note: this briefing highlights the report’s strategic value while preserving the proprietary segmentation and modeling detail that underpin our recommendations. For full access to datasets, scenario models, company scorecards and downloadable toolkits, please visit PW Consulting’s Collector Auto Insurance Market report page or contact our client services team to request the complete dataset and licensing options.

For detailed analysis of this topic, please visit the official page:Collector Auto Insurance Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com