Precision Planarization Technologies Strengthen Semiconductor Equipment Market Outlook

Film |

2026-06-16 07:00:14

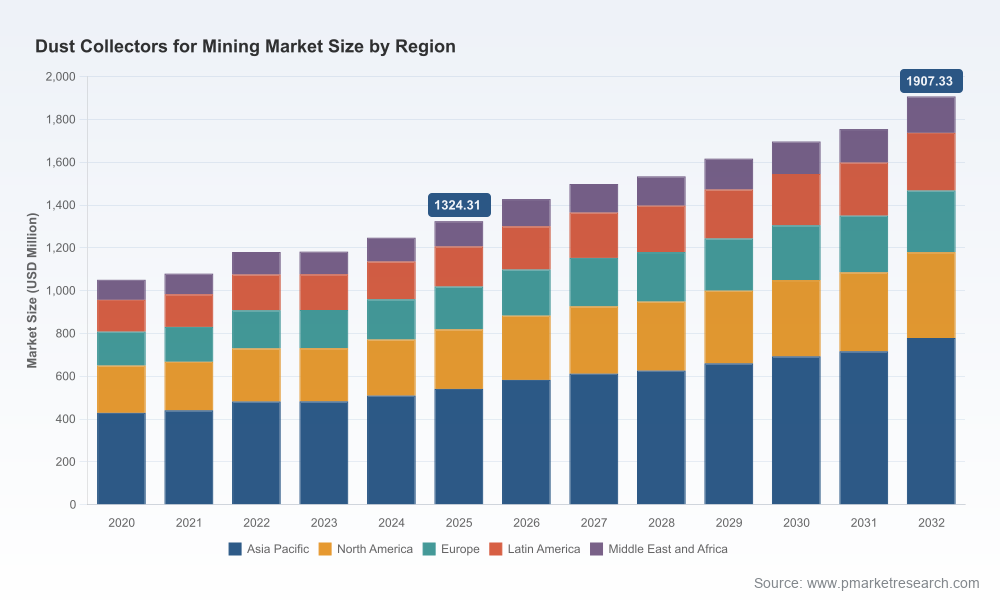

PW Consulting releases a strategic preview of our full Dust Collectors For Mining Market research (base year 2025; historical span 2020–2025; forecast 2026–2032). The market is projected to continue a mid-single‑digit upward trajectory (CAGR 5.35%) as mining operators, EPCs, and equipment OEMs reconcile tighter health-and-safety mandates, evolving process requirements, and supply‑chain pressure. Measured in USD (Million), the addressable market expanded from roughly 1.05 billion in 2020 to about 1.32 billion in 2025 and is modelled to cross the 1.9 billion mark by 2032 — a pace that makes 2026 a pivotal year for capital allocation and compliance roadmaps.

Dust Collectors For Mining Market

Regulatory imposition as catalyst: The Mine Safety and Health Administration (MSHA) established a uniform respirable crystalline silica PEL that requires engineering controls as the primary means of compliance, with compliance deadlines concentrated in 2026. For mining operators and equipment suppliers this changes procurement priorities from optional improvements to mission-critical upgrades.

Dust Collectors For Mining Market

Cost and supply pressure: Volatility in raw-material inputs used in heavy-gauge collector construction (notably steel) and forecasted commodity price shifts are compressing margins and extending lead times for capital equipment. Expect procurement cycles to lengthen as buyers hedge on price and availability.

Dust Collectors For Mining Market

Technology and safety convergence: The simultaneous rise in demand for systems that control respirable crystalline silica, combustible dust, and abrasive particulate places a premium on integrated solutions — modular architectures, explosion‑proof designs, and service‑centric aftermarket offerings.

Transparent market sizing and scenario models: Interactively model demand through 2032 with base/accelerated/stress scenarios, and a sensitivity engine tuned to regulatory timing, commodity price paths, and capex cycles.

Procurement playbook for 2026 buyers: Prioritized CAPEX triage, retrofit vs. greenfield decision frameworks, procurement templates, and vendor negotiation levers that reduce total cost of ownership (TCO) over 5–10 year horizons.

Vendor scorecards and sourcing matrix: Comparative assessments across product families (baghouse, cartridge, wet scrubber, cyclone, electrostatic) covering performance, MEAL (maintenance, energy, average life), compliance readiness, and service footprint.

Engineering and O&M guides: Practical retrofit pathways for legacy systems, explosion-risk mitigations, spare-parts rationalization, and predictive maintenance KPIs tied to uptime and regulatory audit readiness.

Case studies and deployment timelines: Real-world implementations that surface common pitfalls (scope creep, civil works sequencing, commissioning lead times) and proven mitigation tactics that shrink schedule slippage.

Supply chain and input-cost analysis: Procurement risk heatmaps, alternate-sourcing options, and suggested hedging approaches for long‑lead items and critical consumables.

M&A and partnership playbook: Where consolidation creates value, white-space areas for bolt-on acquisitions, and go-to-market alliance strategies for international scale.

The market’s mid-single‑digit CAGR conceals a portfolio of structural drivers that will shape strategic outcomes in 2026 and beyond. Foremost is compliance-driven retrofit demand triggered by the MSHA silica rule, which elevates engineering controls into a primary compliance lever. That regulatory imperative creates near-term urgency for capital deployment while also re-prioritizing O&M spend toward monitoring, filtration consumables, and verification services.

Second, lifecycle replacement waves and increasing mechanization across mining operations sustain baseline demand. Third, capital and operating cost pressures — influenced by steel and related commodity prices — are forcing product manufacturers to innovate around lighter-weight, modular designs and alternative materials where performance permits. Finally, the market remains moderately concentrated: the top three vendors control a meaningful but not dominant share, and the top five expand that footprint further, indicating room for consolidation, strategic partnerships, and regional challengers to capture niche value.

Donaldson Company, Inc. — Known for established Torit® baghouse and cartridge systems, Donaldson competes on proven field performance and deep OEM integration into mineral-processing lines. Their strengths are engineering depth and aftermarket reach; buyers should evaluate long-term filter economics and local service coverage.

Camfil APC — With heavy‑duty modular collectors geared to harsh mining dusts, Camfil APC emphasizes robustness and ease of scaling. Their modularity is an asset for staged upgrades, though OEM alignment and lead-time management are critical negotiations.

RoboVent — Positions on heavy‑duty modular Senturion systems and combustible-dust control, bringing flexibility for bespoke installations and hazardous environments. Strong in sectors demanding tailored safety certifications.

Sly Inc. — Offers a diverse product mix (baghouse, cartridge, wet scrubbers) and plays to markets requiring versatility across abrasive and combustible dust applications. Their competitive edge lies in cross-product integration for complex process lines.

Imperial Systems, C&W DustTech, Camcorp, Baghouse.com — These specialists bring regional service intensity, explosion‑proof and hooding expertise, and competitive pricing for retrofit projects. They are frequently preferred for fast-turn or highly localized deployments.

Ducon Environmental Systems, AAF International, Scientific Dust Collectors — Companies with niche strength in cyclone/wet-dry scrubber technologies and patented cleaning systems. Their innovations are often incorporated into bespoke projects where material recovery or water use is a binding constraint.

Recent industry signals reinforce these positioning trends: case-in-point, exhibitors and product promotions at major trade events in late 2025 and early 2026 emphasize MSHA-driven product enhancements and transfer-point dust control; specialist vendors are using these platforms to accelerate dealer and service partnerships. For purchasers, this creates two parallel opportunities in 2026: lock in compliance-ready platforms from established vendors, or deploy focused pilots with specialists to test lower‑cost, rapid‑deployment alternatives.

Execute a regulatory readiness audit within Q2 2026: Map all respirable silica exposure points, identify engineering controls already in place, and cost-out prioritized retrofits with staged milestones tied to compliance checkpoints.

Prioritize CAPEX into high‑impact nodes: Start with transfer points, crushers, mill exhausts, and load zones where both particulate load and compliance risk converge. Use vendor TCO models rather than headline purchase price.

Negotiate service-level guarantees and parts consignment: Lock-in filter-supply agreements and response-time SLAs aligned to mining seasonality to prevent production downtime.

Mitigate supply risk: Qualify at least two vendors for critical systems and source long‑lead components early; explore modular or rental solutions to bridge immediate compliance gaps.

Run focused pilots for alternative materials/architectures: Where steel pricing drives cost, pilot lighter materials or modular assemblies to validate lifecycle performance before wide deployment.

Embed monitoring and verification: Instrument new and retrofitted systems with continuous particulate and differential-pressure monitoring to evidence compliance and optimize maintenance schedules.

Treat aftermarket as strategic differentiator: Vendors that offer predictive maintenance, rapid filter logistics, and verified compliance reporting reduce total program risk and should be prioritized.

Consider consolidation and partnership plays: Strategic acquisitions or long-term alliances can rapidly scale regional service networks and capture aftermarket revenue streams.

This article is a strategic companion designed to orient executives, procurement leads, and engineering teams for immediate decision cycles in 2026. The full PW Consulting report contains the granular intelligence buyers and investors will need to execute: downloadable financial models, vendor scorecards, granular regional and product segmentation, procurement term sheets, and detailed case studies with installation timelines. Those actionable datasets and operational templates are intentionally withheld here to preserve the consultative value of the full report and to support rapid adoption by organizations preparing binding 2026 investment cases.

For teams that must translate regulatory shock into competitive advantage, the pathway is clear: prioritize engineering-control investments that align with operational sequencing, hedge supply‑chain exposure, and select vendors by lifecycle economics and service capability rather than headline price alone. PW Consulting’s full market model and vendor playbooks are built precisely to accelerate those decisions with auditable, scenario‑based evidence.

Download the full report to access the complete segmentation, vendor scorecards, and our interactive financial model.

Engage PW Consulting for a custom briefing: we will translate the market scenarios into a site-level project prioritization matrix and a 90‑day procurement sprint plan.

PW Consulting — industry-grade analysis and practical execution templates to help mining operators, OEMs, and investors convert 2026 regulatory and market change into defensible competitive advantage.

For detailed analysis of this topic, please visit the official page:Dust Collectors For Mining Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com