Enhanced Adoption of Bipolar and Ultrasonic Energy Systems to Strengthen the Market at a 5.3% CAGR

Party |

2026-07-14 06:26:26

PW Consulting today releases an executive preview of its forthcoming market research on the Aeroengine Accessory Drive Train (ADT) market. Built from five years of historical analysis and a seven-year forecast horizon, this briefing is designed to help C-suite leaders, strategy teams, and M&A advisors align 2026 investment and program decisions with the sector’s near‑term trajectory and structural dynamics.

Aeroengine Accessory Drive Train Adt Market

Our analysis shows the ADT market continuing an expansion that resumes pace after the pandemic-era disruption: the market is projected to grow at a compound annual growth rate (CAGR) of 6.85% over the forecast period 2026–2032. In practical terms, PW Consulting models the global ADT market at approximately USD 1.025 billion in the report’s base year (2025), rising toward roughly USD 1.63 billion by 2032. This trajectory is driven by a combination of OEM platform ramp-ups, aftermarket tailwinds, and incremental demand for higher‑performance materials and precision components.

Aeroengine Accessory Drive Train Adt Market

Programme transitions: Several large commercial and military engine programs move from development to production scale in 2026–2028, creating timing-sensitive supply and capacity decisions for ADT suppliers and integrators.

Aeroengine Accessory Drive Train Adt Market

Aftermarket recovery and service economics: Airlines and MRO networks are prioritizing life‑cycle cost reduction and fleet availability, elevating the strategic value of ADT reliability, modularity, and repair‑by‑exchange choices.

Material & supply-chain pressure: Volatility in titanium and nickel‑alloy markets is forcing procurement and design teams to reassess sourcing strategies and material substitution options within ADT bill‑of‑materials.

Certification complexity: Stricter FAA/EASA requirements for new materials and design approaches mean longer lead times and higher up‑front engineering expenditures for first‑time entrants.

The published study is deliberately hands‑on. It combines market-size modelling with executable guidance across commercial, technical, and transactional dimensions:

Top‑down and bottom‑up market sizing (historical 2020–2025; forecast 2026–2032) and sensitivity scenarios to stress‑test demand under alternate civil and defense outcomes.

Detailed supply‑chain risk matrix: mapping raw‑material exposure, tier‑1/2 supplier single‑points of failure, and mitigation levers (dual sourcing, strategic inventory, long‑lead contracts).

Technology roadmap: assessment of design trends in gearboxes, shafts, bearings and seals, and advanced manufacturing that materially affect unit cost, weight, and certification timelines.

Commercial playbook for OEMs, tier‑1s and aftermarket service providers — covering pricing strategies, aftermarket capture tactics, and MRO network design to optimise lifetime value.

Granular competitor benchmarking and strategic options: capability heatmaps, program exposure matrices, and potential M&A target lists informed by capability gaps and concentration dynamics.

Regulatory and certification briefing: practical roadmaps for FAA/EASA approval pathways for novel materials and subassembly architectures, including recommended test program staging.

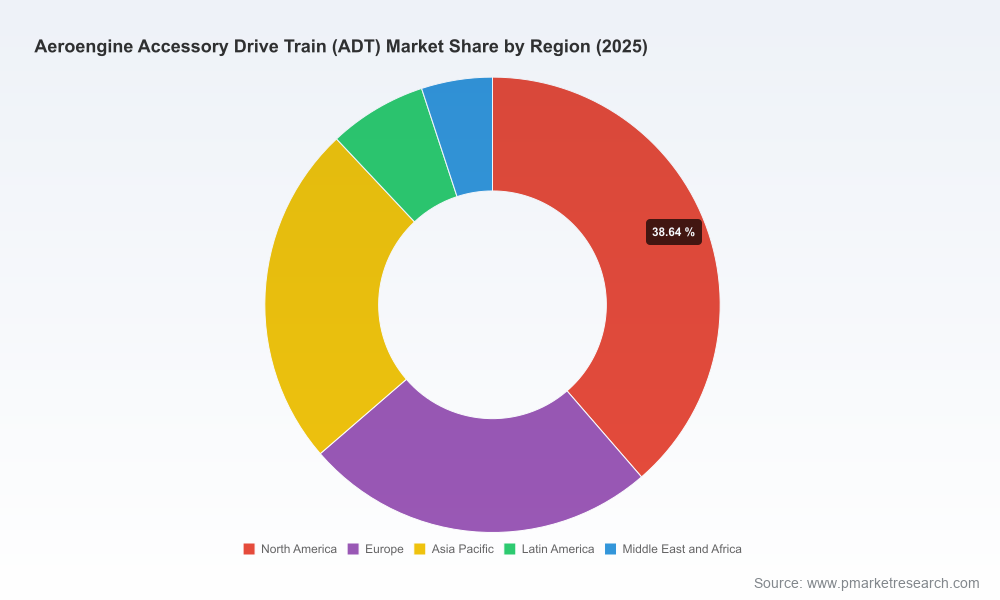

The report contains full segmentation by region, by component (e.g., gearboxes, shafts, bearings & seals, and others), and by engine type. These detailed splits are central to program‑level commercial planning and supplier selection, but in keeping with our pre‑release strategy we are intentionally not disclosing core subsegment figures in this preview. The full, source‑verified splits are available in the paid report and provide the granularity necessary for procurement, investment and engineering decisions.

What we will disclose here: the market remains moderately concentrated at the top end — PW Consulting’s concentration analysis shows that the leading three suppliers account for a substantial portion of the market, and a larger block of share is held by the top five. This concentration has direct implications for negotiating leverage, capacity availability, and programme risk.

The ADT competitive arena features a mix of large industrial integrators, specialist precision manufacturers, and component suppliers whose strategies are converging around programme partnerships, vertical integration, and niche capability plays. Key players covered in the report include:

Avio Aero (GE Aerospace) — strong platform integration capabilities; experienced in delivering inlet, transfer and accessory gearboxes for next‑generation high‑thrust engines. Its close OEM links give it programme insulation but also concentrate exposure to specific engine families.

Safran Transmission Systems — established supplier for both commercial and military ADTs, with deep certification and systems expertise. Recent collaborations expand its manufacturing footprint and programme scope.

BMT Aerospace International — specialist in complex accessory gearboxes and first‑article deliveries for business jet and defence programs; a recent flight‑critical gearbox delivery highlights its scale-up from component supplier to integrated gearbox assembler.

Liebherr‑Aerospace — focused on high‑precision gearing and systems integration with a reputation for engineering depth across aero‑engine and airframe power‑systems.

Triumph Group, Northstar Aerospace, and The Timken Company — represent a combination of precision drive system suppliers and bearing specialists whose component reliability and aftermarket service offerings make them strategic partners for both OEMs and MRO networks.

Strategic takeaway: suppliers that balance programme exposure with diversified end‑markets, and that can demonstrate robust certification pathways and resilient material sourcing, will command premium access to production slots and aftermarket flows.

Commercial scale deliveries: a major gearbox delivery by a specialist supplier in early 2026 evidences successful industrialisation of a previously development‑phase programme. Practically, OEMs and primes should assess tier‑1 readiness ahead of production rate increases to avoid bottlenecks.

Cross‑company manufacturing partnerships: formalised collaborations between booster/engine subsystem integrators and gearbox specialists indicate consolidation of programme responsibilities. For potential entrants, partnering is now a faster route to certification credits than sole‑sourced build‑outs.

Raw‑material pressures: titanium and nickel‑alloy supply volatility, along with geopolitical concentration of upstream producers, increases execution risk. Procurement teams must prioritise visibility to second‑tier sources and hedge exposure through long‑term agreements or qualified alternative materials.

Regulatory friction remains non‑trivial: leaning on incumbent suppliers’ certification data packages is an effective way for OEMs and new technology adopters to compress time‑to‑market.

Prioritise programme exposure mapping — quantify how many production slots and aftermarket revenue years are tied to each engine family in your portfolio, and stress‑test under +/-20% production scenarios.

Secure material continuity now — lock conditional commitments for titanium and nickel alloys, and fund qualification programmes for plausible material substitutions to mitigate single‑source disruptions.

Evaluate strategic partnerships over greenfield capacity — where certification timelines and capital intensity are high, partnering with an established gearbox integrator can accelerate market access and reduce capital at risk.

Embed certification strategy into product roadmaps — allocate engineering and test capital early to avoid late‑stage rework when introducing new alloys, surface treatments, or additive manufacturing approaches.

Use concentration dynamics to your advantage — smaller OEMs and Tier‑2s should pursue niche excellence in bearings, seals or specialty machining to become indispensable to the larger system integrators.

For teams preparing budgets, sourcing strategies, or M&A pipelines in 2026, PW Consulting’s ADT report provides the market models, supplier due diligence templates, and programme‑level exposure matrices needed to make decisions with confidence. The analysis is data‑driven, audit‑ready, and oriented toward pragmatic implementation — from supply‑chain contingency playbooks to go‑to‑market approaches for aftermarket capture.

This preview intentionally refrains from publishing the full subsegment breakdowns and programme exposure tables; those details are included only in the full report and client workshop materials. Organisations that need immediate support in translating the market findings into procurement, product, or M&A actions can request bespoke briefings, scenario modelling, and supplier diligence support from PW Consulting.

To access the complete Aeroengine Accessory Drive Train (ADT) market report, detailed segmentation, and the full set of appendices (methodology, supplier scorecards, and certification checklists), please visit the PW Consulting report page or contact our industry practice team for a tailored briefing.

For detailed analysis of this topic, please visit the official page:Aeroengine Accessory Drive Train Adt Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com