Pulmonary Embolism Therapeutics Market: Strategic Imperatives for 2026 — PW Consulting Insight Brief

Executive summary

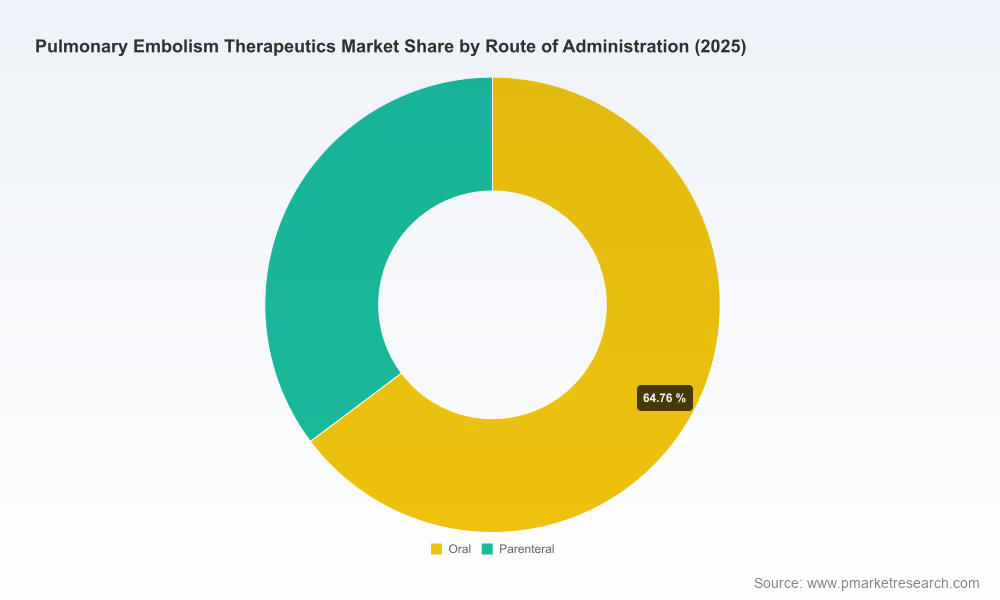

PW Consulting’s latest Pulmonary Embolism (PE) Therapeutics Market report frames a rapidly evolving landscape in which clinical innovation, device adoption, intellectual property events and reimbursement shifts converge to reshape competitive advantage. The global market reached roughly USD 2.19 billion in our base year (2025) and, under our central projection, will expand at a compound annual growth rate (CAGR) of 8.15% through the 2026–2032 forecast window — with clear inflection points driven by clinical trial readouts, generic entry, and accelerating uptake of interventional solutions. Market concentration remains material: the top three and top five firms account for a dominant share of market value, underscoring that strategic moves by a handful of players will continue to influence pricing, access and innovation dynamics.

Pulmonary Embolism Therapeutics Market

Why this report matters for 2026 corporate decision-making

2026 is a watershed year for PE therapeutics. Patent cliffs for established oral anticoagulants, growing clinical evidence for catheter-based and mechanical thrombectomy approaches, and payor policy adjustments are colliding with supply-chain vulnerabilities for key APIs. Executives who need to prioritize investment, align R&D and recalibrate commercial plans require a concise, playbook-driven synthesis that links market sizing to executable options. This report is designed to supply that synthesis — it provides the quantitative lens needed to size opportunity and the qualitative intelligence required to act, while deliberately preserving granular segmentation tables and proprietary unit economics behind a gated model so that subscribers unlock the full decision-support toolkit.

Pulmonary Embolism Therapeutics Market

What the report contains — practical deliverables

- Market model and forecast (2026–2032) with scenario variants (base, accelerated device adoption, and faster generic penetration) to stress-test capital allocation and launch timing.

- Commercial playbooks for product and device portfolios: go-to-market, channel optimization, and value demonstration templates for hospital systems and payors.

- Regulatory and patent heat map highlighting imminent expiries, exclusivity windows and likely generics/liberalization timelines that affect pricing and market share trajectories.

- Clinical-evidence tracker linking late-stage trials and pivotal device studies to adoption curves and revenue inflection points.

- Reimbursement and HTA intelligence: mapping of procedure codes, payment levers and payor behaviors that determine economic viability of interventional approaches versus drug-only strategies.

- Supply-chain risk assessment with mitigation frameworks to manage API shortages and raw-material price inflation.

- M&A and partnership playbook including target archetypes, valuation heuristics and integration checklists for bolt-on device or specialty pharma acquisitions.

- Customizable dashboards and an executive one-page decision matrix that synthesizes financial, clinical and regulatory risks for board-level briefings.

Competitive landscape — who matters and why

The PE market is a two-track competitive arena: established pharmaceutical leaders defend and optimize anticoagulant franchises, while a newer cohort of device-focused firms seeks to expand procedure-driven care pathways. Our report profiles the commercial and clinical strategies of the most consequential players and interprets how each can shift the market balance in 2026.

Pulmonary Embolism Therapeutics Market

- Bayer AG — With a marquee direct oral anticoagulant in its portfolio, Bayer’s near-term priorities will be lifecycle defense, line-extension evidence generation and novel formulations that preserve share as generics enter. Strategic alliances with diagnostics or hospital networks could blunt volume erosion by reinforcing branded value.

- Bristol-Myers Squibb / Pfizer — The joint program behind a leading oral agent positions them to capitalize on secondary-prevention indications. Their scale in global commercialization will be an advantage in defending reimbursement positioning, but they face exposure to exclusivity expiration and must accelerate pediatric and label-extension evidence where feasible.

- Boehringer Ingelheim — A direct thrombin inhibitor in the treatment pathway creates opportunities for differentiated messaging around safety profiles and reversal strategies. Tactical investments in outcomes research could translate to formulary preference in select systems.

- Daiichi Sankyo — As a specialty-originator of a factor Xa option, the company’s strategic focus can include post-acute care transitions and partnerships with anticoagulation management services to secure long-term patient flows.

- Genentech (Roche Group) — With an established thrombolytic agent restricted to high-acuity presentations, continued guideline alignment and payer negotiation are critical; off-label economics remain limited, reinforcing the need to target narrow, high-value use cases and maintain hospital-liaison programs.

- Inari Medical — Clinical validation is the core growth lever. Recent trial data demonstrating superiority of a mechanical thrombectomy approach in an intermediate–high risk cohort materially improves the device value proposition. The company is well positioned to capture procedure share if it can translate trial endpoints into real-world workflow efficiencies and managed-care reimbursement acceptance.

- Penumbra, Inc. — Product evolution and incremental device performance gains lower procedural friction. Continued investment in operator training and ecosystem partnerships (catheter labs, interventional networks) will determine how rapidly aspiration-based systems substitute for conservative management in borderline cases.

- Boston Scientific — A focus on combination therapy platforms (ultrasound-facilitated thrombolysis) requires a dual narrative: clinical superiority in selected patients plus operational simplicity for hospitals. Demonstrating reduced LOS and ICU utilization will be essential to justify adoption.

Market dynamics and near-term catalysts

Several non-linear drivers will shape market outcomes in 2026:

- Intellectual property transitions: Approaching expiry timelines for marquee oral agents will accelerate generic competition and compress price realization for incumbents unless offset by new indications or authorized brands.

- Device evidence and diffusion: Randomized and pragmatic trial results favoring interventional strategies will change care algorithms for intermediate-risk cohorts and create addressable volumes for thrombectomy systems and adjunctive technologies.

- Reimbursement clarity: Recent procedural coding updates and payor signaling are making certain PE interventions economically sustainable for hospitals — but reimbursement thresholds and utilization management will be decisive.

- Supply-chain fragility: Raw-material disruptions for anticoagulant APIs introduce margin pressure and could force prioritization of product lines or opportunistic sourcing strategies.

- Guideline and HTA alignment: Restrictive guidance for systemic thrombolysis in non-massive PE limits market expansion for thrombolytics outside narrow indications, elevating the importance of device-based alternatives.

Actionable strategic recommendations for 2026

Based on the market sizing, concentration dynamics and competitive intelligence captured in our report, PW Consulting recommends five priority actions for executive teams planning 2026 strategies:

- Reallocate near-term R&D and commercial spend toward indications and technologies that are least exposed to imminent generic competition — particularly devices and combination treatment pathways supported by new evidence.

- Execute early payer engagement and health-economic pilots in high-volume systems to secure coverage policies for interventional therapies; focus pilots on demonstrable reductions in length-of-stay, complication rates and downstream costs.

- Design lifecycle defense programs for at-risk oral agents emphasizing differentiated outcomes, adherence solutions and branded-service bundles that raise switching costs for prescribers and patients.

- Pursue bolt-on acquisitions or partnerships to fill capability gaps (e.g., device access, catheter-lab training, neurovascular expertise) rather than broad platform bets — smaller, targeted transactions offer faster integration and clearer ROI.

- Implement supply-chain resilience plans that include alternate sourcing, strategic inventory, and contract terms to mitigate API volatility — ensure manufacturing and procurement levers are stress-tested against shortage scenarios.

How PW Consulting accelerates your 2026 playbook

Our PE therapeutics report is purpose-built to turn market intelligence into executable strategy. For companies seeking immediate support, PW Consulting offers: bespoke valuation models tied to your portfolio, commercialization roadmaps for device–drug combos, payer negotiation playbooks and M&A diligence on target assets. The report’s appendices contain granular datasets, Excel-based scenario tools and a proprietary competitive-intelligence matrix — access to these gated materials is provided with subscription.

Next steps

This brief outlines the strategic implications we anticipate in 2026; however, the full value to decision-makers lies in the report’s detailed segmentation, unit economics and scenario-model outputs that we intentionally reserve for subscribers. Organizations preparing budgets, R&D priorities or M&A pipelines for next year should consider an expedited review of the full report and an advisory engagement to translate insights into a prioritized action plan.

For detailed analysis of this topic, please visit the official page:Pulmonary Embolism Therapeutics Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com