High-Efficiency Soldering Technologies: Core Material Drivers Reshaping Global Microelectronics Infrastructure

Other |

2026-06-30 08:05:55

As infrastructure resilience and work‑zone safety climb national policy agendas, the global road crash attenuator market is entering a phase of sustained expansion. Our latest PW Consulting Road Crash Attenuator Market report synthesizes a six‑year historical view (2020–2025) with a forward forecast (2026–2032) to deliver strategic intelligence that matters for 2026 capital allocation, product road‑mapping, procurement, and M&A. The market expanded from approximately USD 485.2 Million in 2020 to USD 645.5 Million in 2025, and under base assumptions is projected to reach roughly USD 977.0 Million by 2032 — reflecting a compound annual growth rate (CAGR) of about 6.09% over the forecast horizon. This briefing highlights the strategic implications of that trajectory while deliberately reserving detailed segment tables and regional line items for subscribers who access the full report.

Road Crash Attenuator Market

Momentum drivers: sustained investment in highway safety programs, stricter deployment requirements for temporary work zones, and ongoing replacement/retrofit cycles for legacy attenuators are underpinning market growth.

Road Crash Attenuator Market

Commercial cadence: the market’s steady year‑on‑year rise during 2020–2025 demonstrates resilience despite commodity volatility and episodic infrastructure project slowdowns; growth through 2032 reflects a mix of steady replacement demand and selective acceleration from large road modernization programs.

Road Crash Attenuator Market

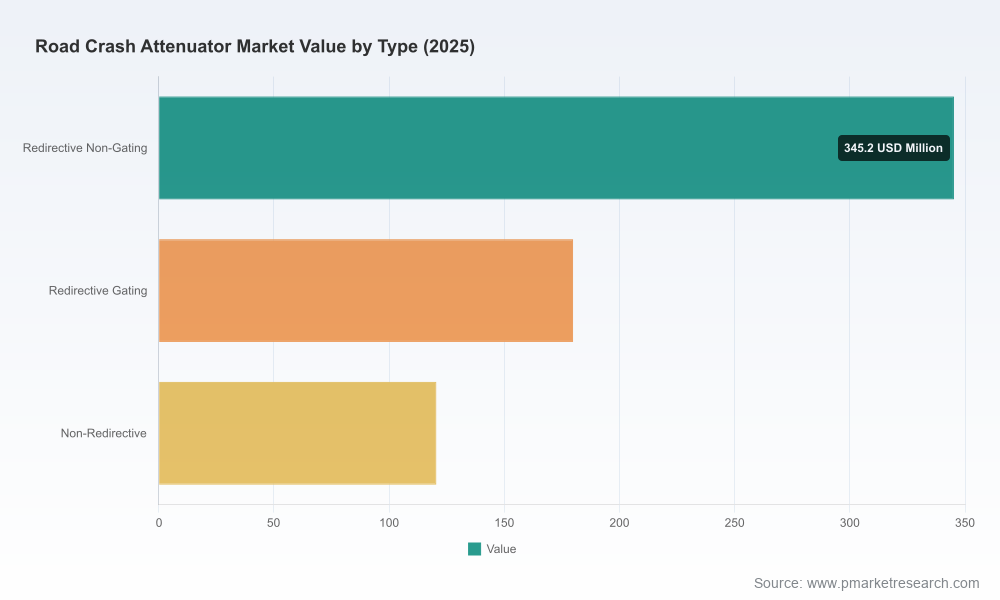

Concentration dynamics: the competitive field is moderately concentrated — the three largest firms account for a meaningful share of market revenue and the top five push total concentration notably higher. This creates clear advantages for scale players in distribution, testing capacity, and regulatory engagement, while leaving tactical opportunities for focused specialists and low‑cost innovators.

Procurement windows are time‑sensitive. Agencies and large contractors should treat 2026 as a planning inflection point: multi‑year contracts and framework agreements negotiated this year will lock in volumes against an environment of elevated steel costs and supply chain tightening. Our report provides a procurement playbook and scenario models to stress‑test contract terms.

Product strategy must reconcile compliance with differentiation. Regulatory test regimes (AASHTO MASH / legacy NCHRP 350 in the U.S.; EN 1317 and ASI classifications in Europe) remain non‑negotiable gatekeepers. Winning in 2026 requires marrying certified safety performance with faster installation, lower lifecycle cost, and serviceability — not just marginal improvements in crash performance.

Supply‑chain risk is actionable. Key structural inputs (notably hot‑rolled coil steel) are trading at materially higher price bands in early 2026 than in prior cycles. Manufacturers that adopt modular designs, selective material substitution, hedging strategies, or localized sourcing will protect margins and shorten lead times.

Aftermarket and service become revenue engines. With higher unit costs and longer useful lives from modern systems, field service, rapid repair kits, and rental fleets for TMAs (truck‑mounted attenuators) are fast‑growing profitable adjacencies in 2026 — particularly for firms that can combine parts logistics with rapid deployment capability.

Practical market sizing (2020–2032) and probabilistic forecasts, with sensitivity scenarios tuned to commodity price paths and regulatory shocks.

Decision frameworks: procurement scorecards, total cost of ownership (TCO) models, and specification checklists designed for DOTs, contractors, and fleet operators.

Competitive intelligence: annotated profiles and capability maps of the leading global suppliers, alongside product feature matrices and testing credentials.

Go‑to‑market playbooks: channel strategies for OEMs targeting rental fleets, direct DOT supply, or international exports; pricing playbooks that reflect concentration dynamics and regional procurement practices.

M&A and partnership dashboards: targets filtered by capability gaps (e.g., modular repair kits, rapid‑deploy TMAs, certification testing labs), with valuation heuristics and integration risk scores.

Implementation tools: ready‑to‑use tender language, sample service‑level agreements for rental TMAs, and retrofit prioritization matrices for asset owners.

The market is composed of established engineering brands and a handful of specialized players that together shape product innovation, testing standards, and channel relationships. A short, non‑exhaustive summary of notable incumbents covered in the report:

Lindsay Corporation — recognized for a diversified crash cushion and TMA portfolio including rapid‑repair TAU systems and ABSORB water‑filled products; recent product introductions in late 2025 and early 2026 strengthen its work‑zone offering and emphasize faster deploy/stow mechanics.

TrafFix Devices — maintains a strong reputation in MASH‑tested redirective non‑gating systems and TMAs with compact deployment footprints; recent generations emphasize short deployment length with full‑width protection for TMAs.

Hill & Smith (Hill & Smith Inc.) — bringing advanced dynamics to attenuator design through speed‑dependent, self‑restoring cushions that aim to optimize deceleration profiles across vehicle classes.

Valtir (formerly Trinity Highway) and Energy Absorption Systems — a combined heritage in modular systems, quadguard families and compact TMAs, with product variants aimed at both permanent and temporary use cases.

Saferoad — a European leader with CE‑marked, EN 1317‑compliant systems and high‑speed certified performance, an important supplier for markets requiring ASI A performance up to higher operating speeds.

Our full competitive chapter maps product credentials to procurement needs, highlights recent launches (including Lindsay’s Road Runner TMA platform line‑extension and TAU‑M Wide launch), and evaluates each player against certification status, service footprint, and aftermarket capability.

Regulatory certainty vs. divergence: While U.S. federal eligibility rests on MASH/NCHRP protocols, European approvals rely on EN norms and ASI ratings. Manufacturers that maintain multi‑regime test dossiers accelerate global market access; those that don’t risk being constrained to regional niches.

Commodity volatility: Early‑2026 hot‑rolled coil price bands materially affect steel‑frame attenuator economics. Our report provides stress scenarios showing margin erosion thresholds and procurement contract clauses to share or cap price exposure.

Service and rental economics: Rental TMAs and modular repair ecosystems reduce upfront procurement outlays for agencies but require robust logistics and rapid repair capability from suppliers to be viable at scale.

Capital allocation tradeoffs: For OEMs, 2026 capital should be prioritized across compliance testing capacity, modular product lines, and digital service platforms (inventory / rapid dispatch) rather than purely incremental performance gains.

For manufacturers: prioritize certification pipelines (MASH / EN 1317), develop modular repair kits, and pilot aluminum/advanced‑composite framing where lifecycle analysis supports cost parity versus steel.

For agencies and contractors: renegotiate framework agreements with built‑in commodity clauses, expand rental‑fleet contracts to smooth capex, and require SLA‑backed response times for TMA deployments.

For investors and acquirers: focus on targets that strengthen service/aftermarket, possess proven testing corridors, or offer rapid‑deploy TMAs; avoid pure commodity producers unless they have durable channel lock‑ins.

This briefing demonstrates the type of strategic insight PW Consulting provides, but deliberately omits the granular segmentation tables, regional and application splits, and downloadable models that underpin procurement and valuation work. To access the full dataset, interactive dashboards, vendor scorecards, and the procurement playbook referenced here, please visit the report landing page or contact PW Consulting’s Road Safety practice. The full report includes itemized segment forecasts, regional demand mapping, supplier revenue pools, and model files you can adapt directly into 2026 budgets and RFPs.

PW Consulting — Strategic clarity for safer roads. If you would like a tailored briefing (30–60 minutes) that applies these findings to your portfolio, procurement pipeline, or product roadmap, our industry team is available to run bespoke scenario workshops and decision‑grade deliverables.

For detailed analysis of this topic, please visit the official page:Road Crash Attenuator Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com