PTFE Lined Dip Pipes Market: Strategic Imperatives for 2026 — PW Consulting Insight

PW Consulting today publishes its authoritative industry briefing drawn from the new Ptfe Lined Dip Pipes Market report (base year 2025). As companies plan CAPEX, procurement, and product strategies for 2026, this market — valued at approximately USD 199.1 Million in 2025 and modeled to grow at a compound annual growth rate (CAGR) of 5.2% through our 2026–2032 forecast horizon — presents both clear opportunity and mounting strategic complexity. Our analysis translates that trajectory into actionable priorities for executives, purchasers, and investors operating across chemical processing, high-purity manufacturing, wastewater treatment, and adjacent process industries.

Ptfe Lined Dip Pipes Market

Why 2026 is a Pivotal Year

Several converging forces make 2026 a decision inflection point for market players and their buyers. Regulatory tightening on hazardous fluid containment and corrosion control is elevating demand for lined solutions. Simultaneously, volatility in PTFE resin pricing (a factor that influences roughly a third to more than half of manufacturing costs depending on product type) and evolving expectations around high-purity process equipment are reshaping supplier economics and product specifications. Our market model shows steady growth from 2025 levels toward the late 2020s, but it is not linear — the path is punctuated by episodic cost shocks and regulatory-driven retrofit cycles that will determine winners and laggards.

Ptfe Lined Dip Pipes Market

What the PW Consulting Report Delivers (Practical, Decision-Ready Content)

- Executive Playbooks: Tailored strategies for OEMs, aftermarket service providers, and industrial end-users that translate market signals into 12–24 month action plans.

- Market Sizing & Scenarios: A transparent market model with base, upside, and downside scenarios for 2026–2032 that quantify the impact of PTFE price swings, regulation updates, and adoption rates of lined vs. solid solutions.

- Supply Chain & Cost Heatmaps: Granular supplier mapping, lead-time analysis, and a stress-tested cost model highlighting where raw material exposure creates strategic vulnerability (including supplier concentration and logistics choke points).

- Commercial & Pricing Playbooks: Segmented go-to-market approaches, margin levers, and practical negotiation tactics for buyers seeking to lock favorable terms amid resin volatility.

- Technology & Product Roadmaps: Comparative assessments of lining methods, adhesion technologies, and high-purity manufacturing adaptations — with guidance on R&D prioritization and test protocols.

- M&A & Partnership Criteria: A checklist to evaluate acquisition targets and alliance partners, balancing technical capability, manufacturing scale, geographic coverage, and aftermarket service potential.

- Regulatory Impact Matrix: A scenario tool that translates specific regulatory changes into CAPEX, compliance, and retrofit costs for plant operators.

- Competitive Intelligence Dossiers: Profiled strategies and capabilities for market incumbents and regional challengers, plus recent development trackers and implications for supply-demand dynamics.

Note: the report contains the full segmentation tables and regional/application-level forecasts behind these summaries. This briefing intentionally highlights strategic conclusions while steering technical readers to the full dataset for granular splits and exact figures.

Ptfe Lined Dip Pipes Market

Market Dynamics: Drivers, Constraints, and Near-Term Catalysts

- Regulatory Tailwinds: Newly enhanced environmental and process-safety requirements are driving retrofit and new-build demand for corrosion-proof piping. Where compliance windows are tight, procurement cycles compress — benefiting suppliers with short lead times and modular solutions.

- Raw Material Volatility: PTFE resin pricing is a principal driver of manufacturer margins. Our sector analysis finds that raw resin exposure can represent roughly 35–45% of manufacturing costs for solid products and 45–55% for lined assemblies, creating divergent profit sensitivity across product types.

- Premiumization & High-Purity Demand: Semiconductor, specialty pharmaceutical, and certain chemical segments are demanding tighter specifications, favoring manufacturers that can certify low-extractable, high-purity fluoropolymer systems.

- Procurement Sophistication: Buyers increasingly use total-cost-of-ownership frameworks that account for longevity, maintenance downtime, and regulatory risk — changing the purchase calculus beyond unit price.

Competitive Landscape: Who Matters and Why

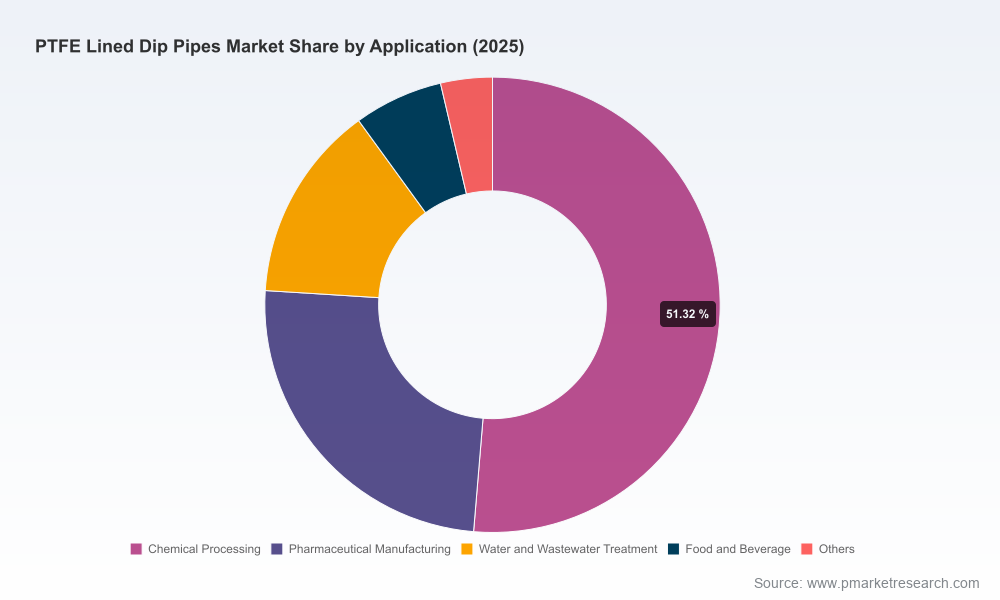

The market displays moderate concentration (CR3 ≈ 38.5%, CR5 ≈ 51.2%), indicating a mix of established specialists and regional/segment-focused challengers. Key vendor archetypes and strategic positions include:

- Established Specialty Engineering Firms: Companies such as Corrosion Resistant Products (CRP) and Edlon (GMM Pfaudler) leverage deep materials engineering expertise and a history servicing agitated, corrosive-reactor applications. Their strengths are proprietary lining techniques, engineered stress calculations for agitated service, and recognized certification pathways into regulated sectors.

- Integrated Fabricators with Branded Systems: US-based Micromold Products offers standardized FLUOR-O-FLO® lined and jacketed solutions targeted at larger nozzles and custom corrosion-resistant assemblies. These vendors scale through standardized SKUs that reduce lead times for certain buyer segments.

- Product-Focused Innovators: Andronaco Industries markets purpose-built Ethylarmor® PTFE lined components optimized for high-stress injection and sparging applications — an example of product-led differentiation in performance-critical service.

- Regional Manufactures & Cost Players: Several India-based suppliers and other regional fabricators deliver competitive cost structures and fast local support for chemicals, pharma, and petrochemical customers where price and proximity dominate procurement decisions.

Recent market moves — for example, expanded distribution partnerships, product-guide releases for semiconductor tank applications, and supplier feature updates focused on adhesion improvements — signal vendor responses to high-purity demand and resin supply-chain pressures. Buyers and investors should treat these as leading indicators of where product premiums and aftermarket opportunities will appear.

Implications for 2026 Strategy — Prioritized Actions

- Procurement & Risk Management (Top Priority for Buyers): Implement a hedging and multi-source procurement strategy for PTFE resin. Where possible, negotiate index-linked contracts, priority allocation clauses, or joint-stock inventory arrangements with strategic suppliers to smooth pricing and availability shocks.

- Product & Service Differentiation (Top Priority for Suppliers): Invest selectively in adhesion technologies and high-purity manufacturing controls. Suppliers that can demonstrate reduced extractables and validated lining adhesion under agitation will command premium pricing and faster approval cycles in regulated end-markets.

- Aftermarket & Service Monetization: Build recurring revenue through certified service packages (inspection, relining, spare-part subscription). Our modeling shows aftermarket services materially improve lifetime margins and reduce customer churn.

- M&A & Partnership Playbook: Target acquisitions that fill capability gaps (e.g., high-purity certification, adhesion R&D, or regional manufacturing footprints) rather than volume alone. Partnerships that accelerate access to semiconductor or pharmaceutical qualification pathways can be more accretive than scale acquisitions in some cases.

- Operational Resilience: Redesign manufacturing footprints to mitigate logistics bottlenecks and single-supplier dependencies. Consider regional inventory hubs and modular production cells to shorten lead times for retrofit projects.

- Commercial Strategy: Shift to value-based pricing where possible, using total-cost-of-ownership analyses to justify premium offers. Create standardized packages for rapid retrofit projects to win time-sensitive procurements.

Risks to Monitor

- Supply Shocks: Disruption in fluoropolymer feedstocks or logistics can compress supply and force margin erosion for unhedged players.

- Regulatory Uncertainty: While regulation generally supports demand, differing regional compliance timelines can produce project clustering and off-cycle volatility.

- Technology Substitution: Emerging lining chemistries or application-specific composites could shift premium pockets away from conventional PTFE-lined designs if adoption accelerates without incumbent response.

How Executives Should Use This Report

Consider the PW Consulting Ptfe Lined Dip Pipes Market report a tactical guide and strategic compass. Use it to: (1) stress-test your 2026 procurement and R&D plans against credible price and regulatory scenarios; (2) prioritize short-cycle investments in high-return product certifications and aftermarket services; and (3) identify targets and partners that accelerate entry into premium, high-purity segments.

We have deliberately presented the report’s strategic conclusions here while reserving the detailed regional and application-level splits, product-level volumes, and line-item scenario outputs for the full dataset. These underlying tables and sensitivity analytics are essential for transaction diligence, procurement renegotiation, and precise revenue forecasting.

Conclusion

The PTFE lined dip pipes market is maturing into a more sophisticated industrial niche where regulatory pressure, material-cost volatility, and high-purity demand create both risk and premium opportunity. With the market at roughly USD 199.1 Million in 2025 and forecast expansion at a 5.2% CAGR through the next planning horizon, companies that combine procurement resilience, technical differentiation, and aftermarket monetization will capture disproportionate value. PW Consulting’s full report equips decision-makers with the scenarios, models, and playbooks needed to act decisively in 2026 — whether the objective is defend, expand, or consolidate market positions.

For access to the full report, detailed segmentation tables, and proprietary scenario models, consult the PW Consulting market release and download the complete dataset.

For detailed analysis of this topic, please visit the official page:Ptfe Lined Dip Pipes Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com