Global Marzipan Market Survey: 86% of Stakeholders Cite Supply Chain Fluctuations and Climate Disruptions

Food |

2026-06-08 18:13:08

As organizations race to support AI training clusters, hyperscale interconnects, and next‑generation metro and access architectures, coherent optical modules have moved from niche long‑haul equipment to a core element of enterprise and carrier network planning. PW Consulting’s latest Coherent Optical Module Market report — with a 2025 base year and a 2026–2032 forecast horizon — quantifies that shift and translates it into executable strategy for 2026 procurement, product and capital decisions. The headline: the market is on a sustained double‑digit trajectory (13.52% CAGR), expanding from an estimated USD 6.25 billion in 2025 to more than USD 15.18 billion by 2032. This trend is reshaping sourcing priorities, engineering roadmaps and partnership models across the ecosystem.

Coherent Optical Module Market

Timing and scale: Buyers and vendors face tightening windows to capture architecture advantages. With continued acceleration in demand, 2026 will be a pivotal year to lock in vendor roadmaps, validate power and density economics, and secure supply‑chain capacity.

Coherent Optical Module Market

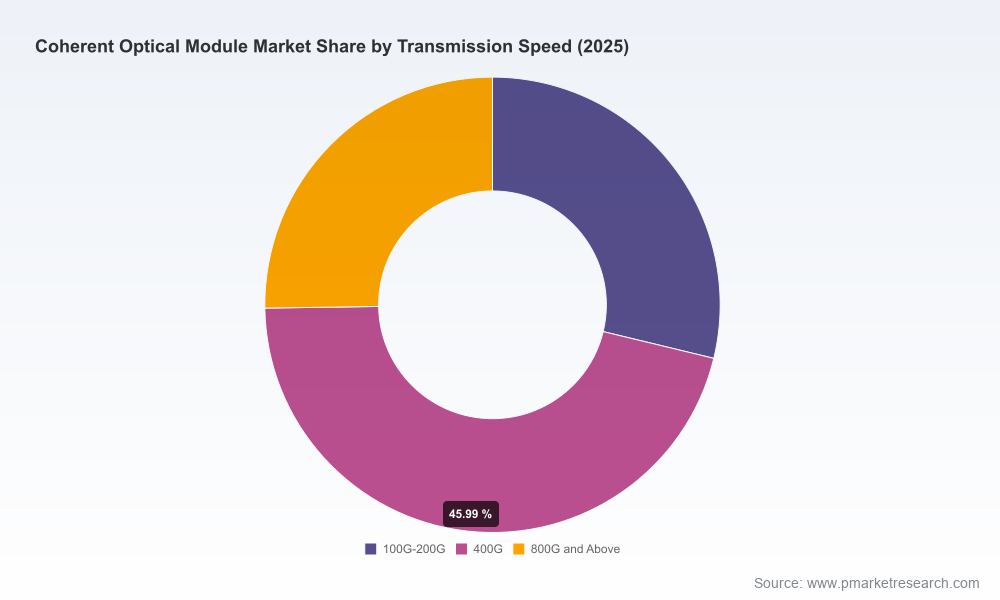

Concentration and competitive dynamics: Market concentration is material — the top three suppliers account for a majority share, and the top five consolidate substantially more. That asymmetry amplifies supplier negotiation dynamics and the strategic value of diversified sourcing and second‑source qualification programs.

Coherent Optical Module Market

TCO and energy as differentiators: Energy and operating costs are now central procurement criteria. The 2026 energy context — including rapid electricity demand growth driven by AI deployments and state/regional pricing reforms — means that module power efficiency, vendor power roadmaps, and site‑level capacity planning will determine long‑term competitiveness.

Our report is designed as a decision support toolkit for executives, architects and procurement officers. Rather than broad academic assertions, it delivers pragmatic outputs you can operationalize immediately:

Market sizing and high‑granularity forecasts: A transparent topline model validated against historical performance and forward indicators, showing the market trajectory across the 2026–2032 horizon and scenario variants that stress power, silicon availability, and adoption rates for pluggable coherent form factors.

Commercial playbooks: Vendor selection frameworks that weight not only price but roadmap alignment (e.g., 400G/800G/1.6T and beyond), thermal and power characteristics, module lifecycle, and supply resilience. These playbooks include negotiation levers tied to volume tiers, NPI timing and co‑development pathways.

Technology evaluation matrices: Comparative analysis of DSP architectures, photonic integration approaches (CPO vs. discrete photonic builds), and pluggable vs. CFP2‑DCO tradeoffs for latency, reach and operational flexibility. The matrices are scored against enterprise and carrier KPIs so product teams and network architects can prioritize features that materially affect TCO.

TCO and power modeling templates: Integrated TCO models that incorporate acquisition, power, cooling, and site impact costs — calibrated with contemporary industry inputs on high‑density AI rack energy consumption and regional pricing dynamics — to quantify lifetime costs across alternatives.

Supply‑chain risk maps and mitigation playbooks: Mapped component failure points (DSP supply, photonics fabs, packaging capacity), lead‑time scenarios, and tactical mitigations such as dual‑sourcing, inventory buffering, and contract structures that transfer risk.

Market entry and product launch guides: For module vendors and component suppliers, go‑to‑market plans tailored to hyperscalers, carriers and enterprise segments, including channel strategies, co‑engineering partnerships, and targeted performance benchmarks that accelerate trials and qualification cycles.

The coherent optics ecosystem is a mix of vertically integrated incumbents, DSP and silicon leaders, and aggressive challengers from Asia. Our report scores and profiles the key players on technology breadth, vertical integration, go‑to‑market strength and NPI cadence.

Coherent Corp. — A leader in high‑capacity coherent transceivers, advancing to 1.6T and demonstrating technologies for even higher aggregate module densities at industry shows. Their vertical integration across photonics elements and systems-level demonstrations position them strongly for AI DCI and large carrier deployments.

Lumentum — Strong in high‑bandwidth modulators and component supply for 400G and 800G pluggables. Their component play makes them a strategic supplier for vendors seeking to reduce time‑to‑market for new form factors.

Fujitsu Optical Components — Focused on high‑performance DWDM and metro‑optimized coherent pluggables, with demonstrable power‑per‑bit reductions in recent launches — an important lever for sites where energy pricing is a gating factor.

Marvell Technology — Advancing DSP performance and integration with COLORZ solutions and next‑generation process nodes. Their DSP roadmap is critical to enabling newer pluggable density points and security features relevant for enterprise DCI.

Acacia (Cisco), Infinera (Nokia), Ciena — Each brings systems and coherent‑engine expertise that blurs the line between component and network vendor, offering packaged solutions attractive to carriers and some hyperscalers seeking end‑to‑end accountability.

Chinese and regional players (Huawei, Accelink, InnoLight) — Playing a growing role in certain markets and form factors, particularly around 400G/800G pluggables. Their presence increases competitive tension and offers alternate sourcing vectors for buyers focused on cost and scale.

Recent industry developments underscore the pace of innovation: demonstrations of 1.6T and multi‑terabit module concepts, announcements of 2nm DSP roadmaps, and product launches that emphasize both higher line rates and aggressive power reduction per bit. These events are signals — not certainties — and our vendor risk‑adjusted adoption timelines help you align trials and deployments to realistic production readiness.

Energy and site economics: U.S. data centers contributed disproportionately to electricity demand growth in 2025, and state‑level reforms (for example, targeted pricing mechanisms introduced in 2025) mean buyers must embed energy cost risk into procurement and site selection. For high‑density AI racks, power and cooling are material line items — understanding power efficiency at the module level is now as important as raw capacity.

Infrastructure and capex pressure: The per‑rack cost of powering dense compute has significant variability; enterprises should use our provided range scenarios to stress test site economics and to compare co‑location vs. on‑prem alternatives when negotiating long‑term contracts.

Regulatory environment: New regional policies and spectrum rulings are changing the interplay between satellite, microwave and fiber networks; carriers and enterprise network planners must track regulatory shifts that affect link planning and backhaul economics.

Technology cadence and standards: The rapid move to pluggable coherent at higher line rates and the emergence of new multi‑technology packaging standards will affect module interoperability and vendor lock‑in. Our report outlines migration pathways that minimize retrofit cost while preserving upgrade headroom.

Recast procurement around power efficiency and lifecycle cost, not just price per port. Require vendor TCO models that include energy, cooling and site impact; make multi‑year purchase agreements contingent on demonstrable efficiency roadmaps and milestone‑driven price adjustments.

Establish staged qualification and dual‑source strategies. Pilot next‑gen modules with two technology partners to avoid single‑vendor dependency. Use shorter qualification cycles and production milestones tied to supply chain transparency to secure capacity.

Invest in modular site architecture and upgrade paths. Design systems to support pluggable coherent upgrades without forklift replacements; prioritize vendor roadmaps compatible with evolving DSP and photonic packaging standards.

The report is structured for pragmatic use by executive teams, procurement, network engineering and product groups. It contains reproducible models, vendor scorecards, procurement templates, scenario analyses and actionable recommendations tailored to hyperscalers, carriers, and enterprise/campus buyers. Importantly, the dataset and annexes enable you to run your own sensitivity tests against energy price trajectories, vendor supply scenarios, and adoption speeds for emerging form factors.

This release intentionally previews the analytical framework, vendor assessments and strategic prescriptions while reserving the full segmented datasets, granular regional and application splits, and line‑by‑line vendor market share worksheets for the full report. Those elements are core to detailed vendor strategy and negotiation playbooks and are provided in the complete offering.

2026 will separate leaders who treat coherent optics as a strategic platform from those who view it as a commodity. With a projected market expansion from a multi‑billion dollar base in 2025 to more than USD 15 billion by 2032 at a sustained double‑digit CAGR, the choices made this year about vendor relationships, power and TCO assumptions, and upgrade pathways will materially affect cost curves and competitive positioning for the rest of the decade. PW Consulting’s Coherent Optical Module Market report gives teams the models, comparative intelligence and procurement playbooks to make those choices with confidence.

For access to the complete dataset, segmentation detail and vendor scorecards that underpin our recommendations, please visit the PW Consulting report page or contact our advisory team to arrange a briefing and customized scenario modeling session.

For detailed analysis of this topic, please visit the official page:Coherent Optical Module Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com