Modular CNG Fueling Systems: Strategic Imperatives for 2026 — PW Consulting Market Brief

As governments, fleets and energy companies accelerate decarbonization pathways, modular compressed natural gas (CNG) fueling systems are moving from niche deployments into mainstream commercial planning. PW Consulting’s new Modular CNG Fueling System Market report synthesizes five years of market history and a seven-year forecast to deliver the actionable intelligence senior executives need to make high-stakes 2026 investments.

Modular Cng Fueling System Market

Snapshot: Why 2026 Is a Pivot Year

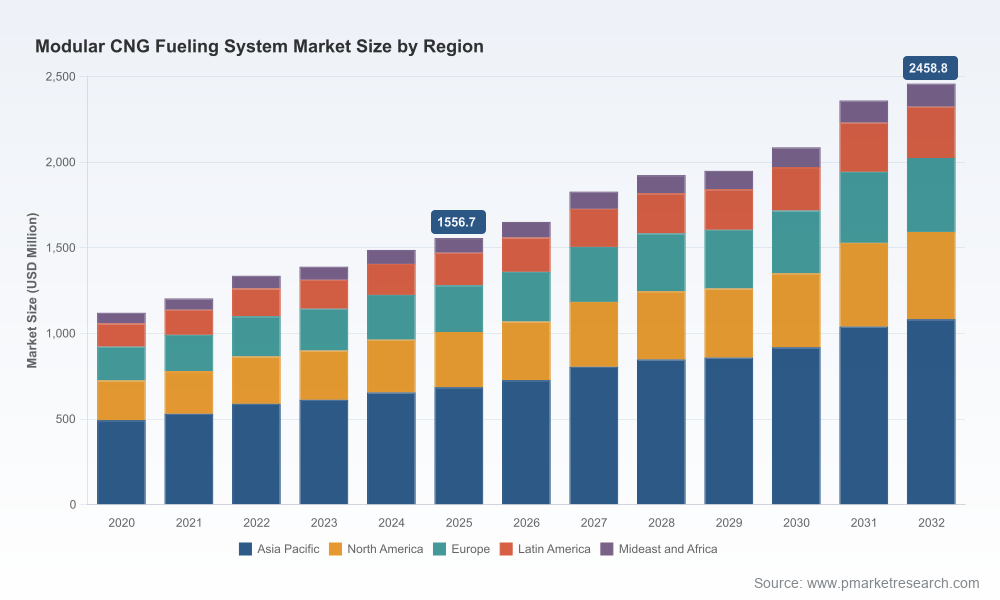

Our analysis shows the global modular CNG fueling system market expanded from around USD 1.12 billion (Million USD) in 2020 to approximately USD 1.56 billion in 2025. Forecast modelling—based on technology adoption curves, policy scenarios and supplier capacity—projects a continued compound annual growth rate (CAGR) of roughly 6.75% through 2032, with the market approaching the mid-USD 2.4 billion range by the end of the forecast period. Market concentration is moderate: the top three suppliers account for a meaningful share, and the top five for a clear majority, indicating both the presence of established players and room for specialist entrants.

Modular Cng Fueling System Market

That trajectory, combined with intensifying regulatory incentives and recent commercial rollouts, makes 2026 the year to convert strategy into committed capital plans rather than exploratory pilots.

Modular Cng Fueling System Market

What This Report Delivers — Practical, Decision-Ready Content

- Scenario-driven market sizing and demand curves calibrated to 2020–2025 history and updated to include 2026 policy developments.

- Forward-looking investment case models (CAPEX/OPEX) with customizable inputs for fuel price, utilization rates and RNG penetration.

- Site-selection frameworks and a geospatial decision matrix for fleet depots, public travel centers and remote virtual-pipeline solutions.

- Vendor scorecards and procurement templates that translate technical specifications into commercial comparators (TCO, uptime, warranty and service KPIs).

- Regulatory impact assessments, including sensitivity analyses under alternate incentive scenarios and carbon-credit regimes.

- Implementation playbooks covering permitting, safety compliance, construction sequencing and operations-readiness checklists.

Note: This brief highlights strategic findings. The full report contains detailed segmentation, regional and station-type slices, and downloadable tools for in-house modelling. Core segmentation tables are reserved for the full report to ensure subscribers receive the complete dataset and raw model files.

Market Dynamics and 2026 Decision Drivers

- Policy acceleration creates near-term economics: Proposed and enacted fiscal incentives—such as the recent 45Z Clean Fuel Production credit rulemaking (proposed Feb 3, 2026) and congressional proposals for RNG incentives—shift project IRRs materially for fleet-anchored CNG projects. The 45Z proposed structure includes a base credit and an elevated credit tied to prevailing wage and apprenticeship compliance; the final contours will be a decisive variable in project-level underwriting.

- Carbon market arbitrage: Jurisdictions with stringent low-carbon fuel standards (for example, bio-CNG treated as deeply negative in certain programs) create standalone revenue streams for RNG-enabled fueling sites. These credits can accelerate payback and justify higher up-front modular investments focused on RNG compatibility.

- Fuel price environment: Natural gas price levels and volatility materially affect operating economics for CNG vs. alternative powertrains. Recent spot pricing has eased some supply-cost concerns, but project stress-testing against higher-price scenarios remains essential.

- Modularity as an operational lever: The modular model (containerized compressors, skid-mounted storage, modular dispensers) reduces initial capex, shortens construction timelines and enables staged capacity deployment—especially important for fleets managing phased conversions or uncertain duty cycles.

Competitive Landscape — How to Read Supplier Positioning in 2026

The supplier field balances global engineering incumbents, regional specialists and service-led integrators. Key archetypes and strategic implications for procurers:

- Turnkey global systems providers — firms with end-to-end capability (compression, storage, dispensing, controls) and global support footprints often command premium pricing but reduce integration risk. These vendors are compelling for high-utilization public or multi-site commercial networks where uptime and standardized maintenance are priorities.

- Compression and equipment specialists — companies focused on compressor and module technology bring deep engineering for high-duty or biogas-ready applications. They are preferred where technical differentiation—efficiency, footprint or biogas compatibility—is a procurement priority.

- Local integrators and virtual-pipeline innovators — these players enable fast rollouts in underserved geographies via virtual pipeline delivery or modular skid packages. They are the pragmatic choice for remote, captive-fleet or temporary installations where speed-to-service and deployment flexibility outweigh scale economies.

- Service-differentiated players — operators that bundle fueling-as-a-service, performance guarantees, or RNG sourcing agreements can convert cost-averse customers by shifting capex to opex and by de-risking utilization assumptions.

Recent commercial events illustrate these archetypes in action: large-scale fueling network openings and commissioning projects across North America and Latin America have been driven by both major fuel retailers and fleet service providers. Orders for on-site power and modular compression units show demand for integrated system solutions that go beyond standalone compressors.

Strategic Recommendations for Executives Planning 2026 Commitments

- Make policy-led sensitivity the default: Underwrite projects against multiple policy outcomes—conservative (no 45Z uplift), moderate (partial credit), and aggressive (full prevailing-wage uplift). This avoids over-committing on marginal green-premium assumptions.

- Prioritize modularity for staged deployments: Use modular systems to de-risk scale-up. Pilot with containerized fast-fill units or mother-daughter configurations where possible, and reserve larger fixed investments for proven high-utilization corridors.

- Design for RNG compatibility now: The value stack for bio-CNG (from low or negative carbon intensity credits) is already material in regulated markets. Spec compressors, materials and controls for biogas to avoid retrofitting costs.

- Embed service and availability guarantees: Negotiate uptime SLAs and outcome-based contracts to move risk to vendors and align incentives on reliability—critical where CNG uptime intersects with fleet operations and revenue protection.

- Use supplier scorecards in procurement: Apply a weighted scoring matrix that balances lifecycle cost, service network, modular lead time, RNG-readiness and compliance track record rather than awarding purely on upfront price.

Procurement and Implementation Playbook Highlights

- Standardized RFP templates for modular CNG projects, including mandatory biogas-ready clauses and commissioning benchmarks.

- Site-permitting checklist aligned to common safety standards and regional regulatory touchpoints to compress approval timelines.

- Financial model templates that integrate fuel-price hedges, carbon credit revenue streams and incentive cliffs.

- Operational handoff and competency-transfer modules to ensure in-house maintenance teams are prepared post-warranty.

How PW Consulting’s Report Supports 2026 Decisions

For executives who must decide in 2026, the report functions as both a market map and a transaction toolkit. It combines empirical market growth data, competitor benchmarking and practical contracting instruments so you can:

- Quantify addressable opportunity and set realistic deployment targets;

- Build finance-ready business cases that reflect upside from incentives and downside from policy shifts;

- Shortlist vendors based on fit-for-purpose criteria that matter to procurement and operations; and

- Accelerate execution by using pre-built templates for RFPs, site selection and commissioning.

Call to Action

PW Consulting’s Modular CNG Fueling System Market report offers the complete dataset, regional and station-type segmentation, downloadable models and vendor scorecards needed to move from strategy to signed contracts in 2026. To access the full analysis, raw model files and vendor benchmarking, visit the report page and download the executive data pack.

For a tailored briefing or procurement-support engagement, our senior consulting team is available to run a 90-minute workshop that applies the report’s models to your portfolio and produces a prioritized roll-out plan aligned to your balance-sheet and regulatory exposure.

PW Consulting — converting market insight into executable advantage for the modular CNG fueling transition.

For detailed analysis of this topic, please visit the official page:Modular Cng Fueling System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com