Europe Water Purifier Market Size, Share, and Growth Opportunities

Other |

2026-05-19 05:10:31

PW Consulting’s latest market intelligence, the Commercial and Industrial Reverse Osmosis (RO) Water Treatment Equipment Market report (base year 2025, forecast 2026–2032), synthesizes five years of historical performance with forward-looking scenarios to equip executives, investors, and operations leaders with the insights required to make confident 2026 choices. The market has expanded materially over the 2020–2025 period and, with a forecast compound annual growth rate (CAGR) of 7.85% through 2032, is set to continue scaling toward the upper end of the industry’s investment cycle by 2032. This preview highlights the strategic takeaways and operational implications without revealing the granular segmentation that subscribers will find in the full study.

Commercial And Industrial Ro Water Treatment Equipment Market

Align capex with realistic market trajectories: With a clearly defined historical base and a conservative-to-constructive forecast path, the report enables CFOs and planning teams to stage capital deployment, financing, and depreciation schedules to match likely adoption curves across industrial end markets.

Commercial And Industrial Ro Water Treatment Equipment Market

Prioritize technology and O&M investments: Energy and recovery technologies are decisive levers for system competitiveness. The report quantifies where energy and membrane-recovery improvements will materially alter lifecycle costs and payback timelines for industrial operators.

Commercial And Industrial Ro Water Treatment Equipment Market

Define M&A and partnership targets with precision: Our competitive concentration analysis (indicative CR3 and CR5 metrics) shows a market structure that supports both bolt-on acquisitions and differentiated niche plays. The report maps the capability gaps most attractive to strategic buyers and private equity sponsors.

De-risk procurement and supply-chain decisions: The study provides procurement teams with scenario-based cost benchmarks and sensitivity analyses that highlight the trade-offs between modular, skid-mounted, and large central plants under fluctuating energy and raw-material conditions.

Robust market-sizing model: Historical series and a transparent forecast engine (2026–2032), with downloadable model templates that stakeholders can re-run under custom assumptions.

Scenario playbooks: Three demand scenarios (conservative, baseline, accelerated) that translate regulatory, energy, and technology drivers into financial and volume outcomes.

Vendor benchmarking and capability maps: Side-by-side comparative frameworks assessing engineering, modularization, service models (including rental and O&M), and high-recovery technologies.

Commercial tools for procurement: Total-cost-of-ownership (TCO) calculators, lifecycle OPEX tables, and procurement checklists to shorten vendor selection cycles.

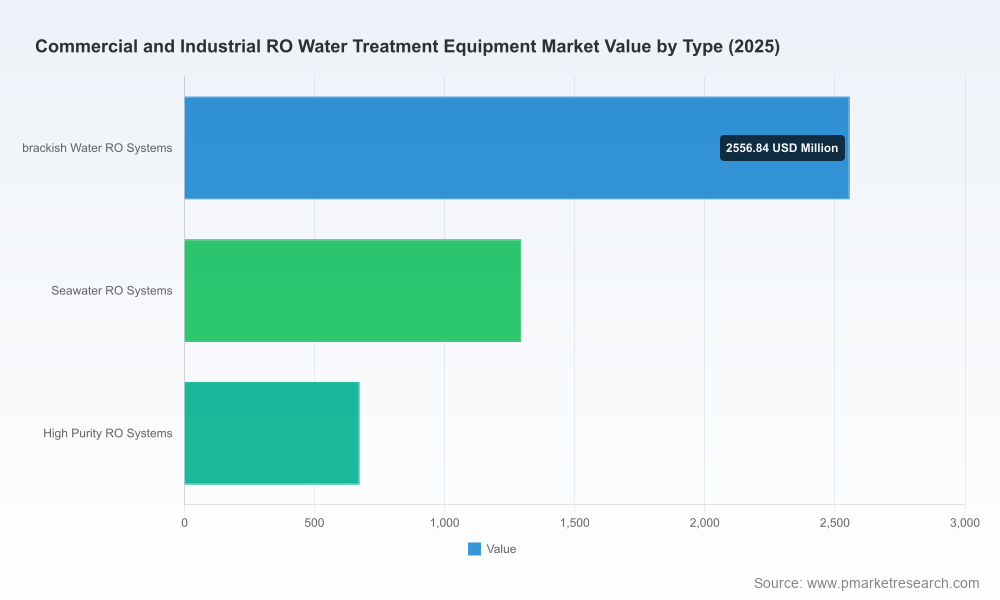

Technical deep dives: Tech briefs on brackish, seawater, and high-purity RO variants; recovery-enhancement techniques (including CCRO and staged recovery) and membrane-chemistry trends.

Regulatory and compliance matrix: Cross-jurisdictional summaries of discharge limits and water-quality thresholds that are reshaping adoption patterns among power, pharmaceutical, and food sectors.

Case studies and implementation roadmaps: Real-world examples that translate strategy into CAPEX phasing, commissioning timelines, and common pitfalls in retrofits vs. greenfield builds.

The market exhibits a moderate level of concentration: the top three and top five players collectively occupy meaningful shares, which underscores both the advantages of scale and the room for specialty players to capture differentiated niches. Manufacturers and integrators will need a two-track approach: defend core product lines through engineering excellence and pursue adjacencies via modular, service-led offers.

MARLO Inc. (Racine, WI) — Strength: custom skid-mounted systems and high-purity MRO series capable of very high rejection rates for boiler feed and process water. Strategic implication: MARLO’s focus on customized, skid-mounted solutions positions it well for industrial customers seeking compact, turnkey deployments.

Pure Aqua, Inc. (Irvine, CA) — Strength: wide capacity range from small commercial to large industrial desalination, and a global footprint for pre-engineered and custom systems. Strategic implication: Pure Aqua’s product breadth supports cross-border project execution and rapid scaling for EPC partners.

AMPAC USA (Baldwin Park, CA) — Strength: in-house designs for harsh environments and desalination expertise for oil & gas and pharmaceutical customers. Strategic implication: AMPAC’s engineering depth is an asset in markets where environmental robustness is a procurement differentiator.

Ecolab / Nalco Water (Naperville, IL) — Strength: integrated chemistry and monitoring solutions (3D TRASAR), with commercial options such as rental and managed services. Strategic implication: Combining chemical and digital monitoring with system provision creates stickier long-term service revenues.

Puretec Industrial Water (California) — Strength: emphasis on high-recovery technologies (e.g., CCRO) and customized system builds. Strategic implication: High-recovery systems will be increasingly attractive where feedwater or disposal constraints raise OPEX risks.

Watts Water Technologies (North Andover, MA) — Strength: modular, scalable commercial RO portfolio with recent launches expanding flow capabilities up to 240 GPM. Strategic implication: Product launches in late 2025 and early 2026 reflect a push toward larger, modular commercial systems that shorten installation time and simplify spec’ing for MEP engineers.

Culligan (Rosemont, IL) — Strength: recognized brand for commercial RO and small-industrial purification systems with efficient purification offerings for business customers. Strategic implication: Strong channel and brand equity drive adoption among small-to-mid commercial customers, where speed-to-service matters.

Regulatory pressure is a primary adoption accelerator. Stricter discharge limits and higher water-quality expectations in power generation, oil & gas, pharmaceuticals, and food processing increase the technical requirements for RO systems and tilt procurement toward higher-spec, monitorable solutions.

Energy intensity remains a dominant operational variable. Industry references put seawater RO energy share at roughly 35–45% of operating costs, and treated-water unit costs can vary materially with plant configuration and energy price regimes. For buyers and owners, this elevates membrane efficiency and energy-recovery devices to critical selection criteria.

Capital and scale dynamics: The market supports both low-cost commercial units for business customers and large-scale desalination projects. Buyers face choices about modularization versus large centralized capacity; modular skid approaches accelerate deployment and lower implementation risk, while economy-of-scale still benefits very large plants.

Service models will differentiate winners: rental, managed O&M, and digital-monitoring contracts are reducing upfront barriers to adoption while creating recurring revenue for suppliers.

OEMs and system integrators — Prioritize energy-efficiency and high-recovery modules in new product roadmaps, and build bundled O&M or rental options that convert CAPEX into predictable revenue streams.

Industrial end-users — Run a TCO re-evaluation for existing RO assets that integrates energy-price sensitivity and regulatory tightening; consider retrofits that enable higher recovery before committing to full replacement.

Investors and M&A teams — Target companies with modular capabilities, digital monitoring suites, or chemistry-integration (scale/softening/coagulation) that enhance margins through services; the market concentration profile favors bolt-on acquisitions that add capability rather than share alone.

Procurement and project teams — Use scenario-driven procurement (baseline plus two stress scenarios) to select vendors that demonstrate resilient supply-chain and service footprints under variable energy and raw-material cost environments.

Policy and sustainability officers — Engage early with regulators on discharge and reuse standards; pilot high-recovery configurations where water scarcity or discharge constraints create operational risk.

Our full Commercial and Industrial RO Water Treatment Equipment Market report provides the granular segmentation, regional and application-level demand matrices, vendor scorecards, and downloadable model files omitted from this preview. That level of granularity is intentionally withheld here to prompt targeted engagement: subscribers receive the underlying data tables, sensitivity scenarios, and executable procurement templates that translate the strategic themes above into executable plans for 2026.

If your 2026 planning cycle depends on defensible market sizing, a clear view of competitive moves, or an executable technology roadmap, PW Consulting’s full report and advisory services deliver the models, benchmarks, and playbooks required to act with conviction. Visit our website or contact our commercial team to access the full study and arrange a tailored strategy session.

For detailed analysis of this topic, please visit the official page:Commercial And Industrial Ro Water Treatment Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com