Does Radio Frequency Treatment Really Tighten Skin?

Health |

2026-07-08 06:10:10

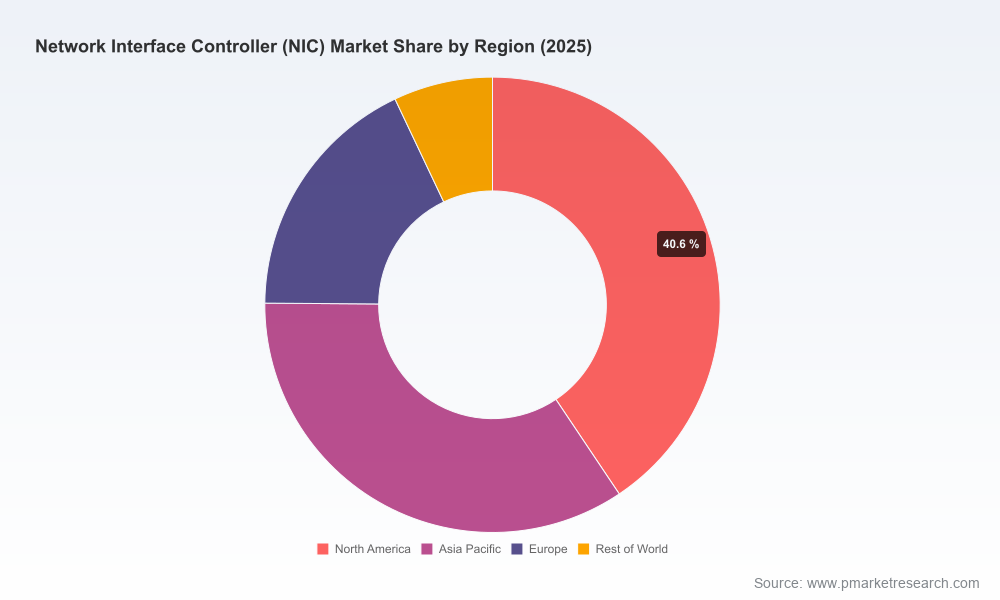

The NIC market is at an inflection point. After steady expansion through the early 2020s, our market model shows global NIC revenue accelerating from roughly USD 3,250 Million in 2020 to USD 6,800 Million in 2025, with a compounded annual growth rate (CAGR) near 16.5% across the 2026–2032 forecast window. By 2032 the market is projected to exceed USD 19,800 Million. These headline figures understate the structural change underway: the migration from commodity Ethernet controllers to programmable SmartNICs and DPUs, the rise of hyperscale and AI-driven networking demands, and new regulatory and infrastructure dynamics that will shape vendor economics and procurement choices through 2026 and beyond.

Network Interface Controller Nic Market

Actionable horizon for capital planning — The pace of NIC innovation (400GbE+, PCIe Gen5/6, CXL-enabled DPUs) means procurement windows are narrowing. IT leaders and infrastructure investors must reconcile multi-year server refresh cycles with rapidly shifting performance per watt and programmability trade-offs. Our report converts forecast growth and technology adoption scenarios into pragmatic CAPEX and lifecycle models to support 2026 budget cycles.

Network Interface Controller Nic Market

Vendor risk and opportunity mapping — Market concentration is meaningful: the top three players capture a majority share and the top five account for a sizable plurality. This concentration accelerates platform-level lock-in and drives differentiated roadmaps for offload, security, and software ecosystems. The report frames vendor choices not just as hardware purchases but as strategic platform bets.

Network Interface Controller Nic Market

Supply-chain and TCO sensitivity — Network spending is now tightly coupled with data center power and fiber infrastructure decisions. Rising energy and cabling demands increase the cost of ownership and force a re-evaluation of deployment density, multi-site redundancy, and colocated compute strategies. The study provides TCO scenarios that incorporate these operational drivers so procurement teams can stress-test vendor proposals.

Regulatory and infrastructure tailwinds — Recent policy moves to accelerate network modernization, combined with large-scale investments in fiber and power infrastructure, change the timetable for service providers and enterprises to adopt advanced NIC architectures. Our analysis translates these developments into strategic timing recommendations for technology transitions.

Comprehensive market model — A reproducible revenue model spanning historical performance and 2026–2032 forecasts, with scenario-based sensitivity for adoption rates of SmartNICs, DPUs, and high-speed Ethernet tiers.

Practical procurement tools — Vendor scorecards, a standardized RFP template for NIC/DPU procurement, and a TCO calculator calibrated to regionally differentiated operating costs and power profiles.

Competitive intelligence dossier — Consolidated profiles for the leading suppliers, recent product launches, roadmap signals and a vendor capability matrix that maps silicon, hardware platforms, offload features, and software integrations.

Risk and resilience playbook — Supply-chain heatmaps, supplier concentration analysis, and mitigation actions (dual-sourcing strategies, long-lead component hedges, and contract clauses) to protect rollout schedules.

Deployment and architecture guidance — Best-practice configurations for data center, edge/telco, and enterprise use cases; migration pathways from standard NICs to SmartNIC/DPU-enabled fabrics without compromising service SLAs.

M&A and partnership framework — Criteria for bolt-on acquisitions, white-space partnership models, and licensing approaches to accelerate in-house NIC capabilities or secure preferential sourcing.

Intel Corporation — Continuing investment in high-speed Ethernet controllers with a push into programmable adapters and next-generation platforms targeted at industrial TSN and edge telco deployments. Strategic buyers should monitor Intel’s platform timing and ecosystem support for accelerated adoption in server fleets.

Broadcom Inc. — Strong in high-throughput NICs and offload features optimized for cloud-native hypervisors and network virtualization. Broadcom’s product families emphasize integration with existing data center switch and silicon portfolios; procurement teams must evaluate software and firmware roadmaps along with hardware specs.

NVIDIA Corporation — The expansion of DPUs and BlueField-series SmartNICs is repositioning NVIDIA from an accelerator vendor to a platform provider for AI-centric data centers. Their DPUs provide deep offload, security services, and cryptographic acceleration making them compelling where workload isolation and programmable infrastructure are priorities.

Marvell Technology Group — Focused on integration of high-throughput DPUs and ecosystem features such as CXL support and Universal RDMA. Marvell’s positioning is attractive to cloud operators seeking tight hardware-software co-design for latency-sensitive services.

Cisco, Juniper, Fujitsu — These incumbents continue to bundle NICs with broader switching, SDN, and server offerings. For enterprises pursuing integrated vendor stacks, their NIC roadmaps and cross-product interoperability are critical evaluation points.

Realtek, TP-Link, NETGEAR and other volume players — Competitive at the low-cost edge and SMB tiers; buying teams should differentiate commodity NIC purchases from strategic SmartNIC investments and apply different governance to each buy stream.

Specialist and niche suppliers (Chelsio, Silicom, Abaco, Lantronix, Molex, LR-LINK) — Offer differentiated form factors (ruggedized, bypass NICs, TOE/iWARP-enabled cards) and are important sources for constrained or specialized deployments like defense, industrial, or telco edge.

Major vendors have accelerated launches of 100/200/400GbE-capable NICs and DPUs, with several firms announcing product availability and production roadmaps in late 2025 and early 2026. These launches materially alter upgrade timing for hyperscalers and service providers.

Large-scale investments in fiber and data center infrastructure, plus rising electricity pressures, are increasing the operational cost sensitivity of high-throughput NIC deployments. Energy and cabling considerations are now first-order inputs to network modernization budgets.

Regulatory shifts that ease certain transition and permitting burdens have shortened deployment lead times in some jurisdictions, accelerating the commercial runway for next-generation IP-based networking in 2026.

Establish a two-track procurement strategy: commoditized NICs follow a cost-and-supply optimization playbook; SmartNIC/DPU purchases require a platform evaluation (software ecosystem, offload roadmaps, security posture) and longer-term lifecycle management.

Embed power and fiber TCO into NIC selection. Require vendors to provide power/performance curves and port-level energy metrics as binding elements of RFP responses.

Pursue vendor diversification for strategic workloads. Where possible, avoid single-source lock-in for DPU-enabled infrastructure and include interoperability and escape clauses in contracts.

Invest in in-house integration skills and open APIs. The shift to programmable network interfaces makes software-defined orchestration and observability essential capabilities for internal teams or trusted partners.

Update governance for security and cryptography. As vendors add hardware-accelerated crypto and post-quantum features, align procurement and security roadmaps to exploit these capabilities safely.

Download the full dataset to access the granular regional and application breakdowns, vendor share tables, and the scenario model used to produce the forecasts. These granular datasets are intentionally held in the full report to support controlled distribution and to preserve commercial value for subscribers.

Use the included Excel model to run bespoke scenarios (e.g., accelerated AI adoption, constrained component supply, or aggressive energy-cost inflation) and generate procurement-ready outputs for board and budgeting cycles.

Leverage our vendor scorecards and RFP templates to operationalize the report’s insights into immediate sourcing actions and pilot projects for 2026.

PW Consulting’s NIC Market Report is designed as both an industry primer and a practical toolkit for decision-makers who must align technology choices with finance, operations, and regulatory realities in 2026. For access to the full datasets, granular segmentation, and step-by-step procurement instruments, visit the report page and request the subscriber package or contact our advisory team for a tailored briefing.

For detailed analysis of this topic, please visit the official page:Network Interface Controller Nic Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com