The Role of Shift Transitions in High-Risk Work Environments

Other |

2026-04-01 09:43:58

PW Consulting today publishes a high-level briefing drawn from our forthcoming Car Blind Spot Surveillance Lens Market report (base year 2025). This executive release distills the report’s strategic takeaways for executives planning capital allocation, product roadmaps, procurement strategies, and partnerships in 2026. It outlines market trajectory, competitive pressure points, supply-chain dynamics, and regulatory inflection points — while reserving the granular segment tables and proprietary vendor share models for the full report to preserve the research value for subscribing clients.

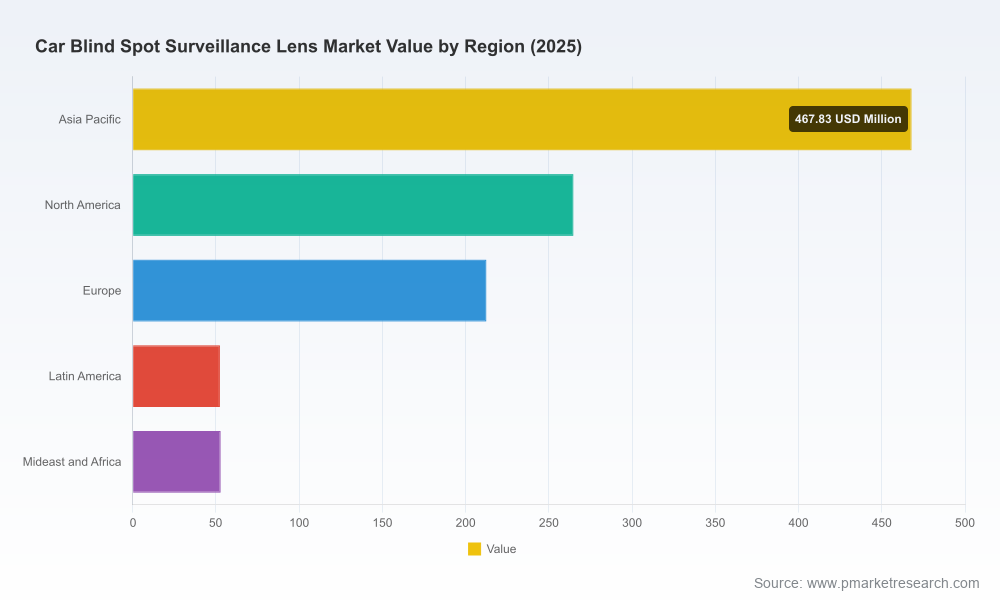

Car Blind Spot Surveillance Lens Market

The blind spot surveillance lens market is moving from niche safety add-on to a core component of mainstream ADAS packages. After a sustained expansion through 2020–2025, the market reached a meaningful scale by 2025 and, under our base-case scenario, is forecast to grow at a compound annual growth rate (CAGR) of approximately 7.85% across the 2026–2032 forecast window. That trajectory reflects accelerating ADAS feature content, higher-resolution camera adoption, and regulatory mandates that increasingly embed blind-spot information systems into vehicle compliance roadmaps.

Car Blind Spot Surveillance Lens Market

Scale and momentum: The market achieved substantial revenue scale by 2025 and is projected to nearly double over the coming forecast horizon under current assumptions. This growth is both demand-led (OEM ADAS content increases, fleet electrification trends that favor camera-based visibility solutions) and supply-side enabled (higher-yield optical manufacturing and new production lines for high-resolution lenses).

Car Blind Spot Surveillance Lens Market

Value shift toward higher performance optics: As camera sensors migrate to higher megapixel counts and OEM requirements for low-light and wide-FOV performance intensify, average selling prices and engineering complexity per lens are rising. This favors suppliers with precision manufacturing, assembly capabilities, and systems-level integration experience.

Consolidation and concentration: Market concentration metrics indicate a moderate-to-high level of vendor concentration, with the top tier of suppliers capturing a meaningful share of market value. This creates opportunities for mid-sized players to target niche product differentiation and for larger players to pursue scale-driven margin advantages.

For C-suite and line leaders, our research translates macro projections into actionable choices you must make in 2026:

Product roadmap prioritization — decide whether to accelerate investment in high-resolution optical programs or to capitalize on cost-optimized plastic lens architectures depending on your channel and customer commitments.

Manufacturing location and capacity planning — use demand timing in the report’s forecasts to phase production line expansions so CAPEX aligns with expected OEM program ramps.

M&A and partnership scouting — the analysis pinpoints capability gaps (e.g., hybrid lens coatings, thermal shock performance, or IP around wide-FOV geometries) that are likely acquisition targets for Tier-1 suppliers and optics houses seeking to close systems-integration gaps.

Supply-chain risk management — raw material trends and supplier footprint mapping enable procurement teams to hedge exposure to critical polymers and specialized glass substrates.

The full PW Consulting report provides the following practitioner-focused deliverables (selected):

Market sizing and validated forecast models (historical 2020–2025 baseline and 2026–2032 projections) with scenario sensitivity and upside/downside assumptions.

Supply-chain map and bill-of-materials analysis identifying single-source risks and common points of failure across optics, coatings, and camera module assembly.

Commercial diligence tools: supplier scorecards, negotiation playbooks, and producer cost-driver matrices to support sourcing and make-vs-buy choices.

Technology deep-dive chapters on glass vs. plastic vs. hybrid lens architectures, coating chemistries, thermal performance, and test methodologies aligned to ADAS requirements.

Regulatory and standards tracker detailing near-term mandates (including EU-level safety rules and UNECE compliance topics) and their likely timing impact on OEM programs.

Go-to-market playbooks for aftermarket suppliers and system integrators, and M&A opportunity mapping for private equity and strategic buyers.

Note: while this briefing highlights the report’s structure and its strategic utility, the complete granular segmentation (regional, application, and lens-type breakdowns) and vendor-specific market share tables are reserved for the full report to preserve the research’s actionable value.

The competitive dynamics are shaped by a mix of specialized optics manufacturers, automotive Tier-1 system integrators, and aftermarket suppliers. The market is neither highly fragmented nor tightly monopolized; the top three to five players command a meaningful portion of value, creating a two-speed competitive environment where scale and OEM relationships matter.

Wintop Optics (China) — Specializes in automotive camera lenses for BSM/BSIS applications, with design capabilities emphasizing wide field-of-view and high-resolution optics. Their focus on side-view surveillance positions them well for OEM programs that value bespoke optical design and integration support. (https://www.wintoplens.com/)

Tesoo Optical (China) — Known for ruggedized lens solutions with high ingress protection and wide operating temperature ranges, making them attractive for heavy-duty and commercial-vehicle segments where environmental endurance is mandatory. (https://www.tesoooptical.com/)

Sunny Automotive Optech (China) — A high-volume supplier with established OEM contracts, recently expanding capacity for higher-resolution ADAS optics. Their scale advantage supports aggressive pricing and reliable delivery for large platform programs. (https://www.sunny-automotive.com/)

Robert Bosch GmbH (Germany) — Integrates lens and camera solutions as part of broader ADAS system offerings. Their systems-level competence and OEM relationships place them at the intersection of sensor hardware and control software requirements. (https://www.bosch-mobility.com/)

Continental AG (Germany) — Another Tier-1 with sensor-to-software capabilities; competence in blind-spot monitoring systems makes them a natural route-to-market for integrated lens modules. (https://www.continental.com/)

Rostra (USA) — Focused on aftermarket dual-camera solutions and low-profile CMOS cameras, representing the commercial opportunity outside of OEM channels. (https://www.rostra.com/)

EverFocus Electronics (Taiwan) — Supplies dual-lens smart cameras for commercial vehicles, aligning products to EU BSIS standards and commercial fleet safety requirements. (https://www.everfocus.com/)

Recent industry moves underscore changing competitive priorities: large optics firms expanding production lines for 8MP+ optics and consumer-electronics scale investments that migrate into automotive-grade manufacturing. These shifts lower time-to-market for high-resolution lens solutions but intensify pressure on mid-tier suppliers to differentiate by performance or cost-efficiency.

Two supply-side themes are critical for 2026 planning:

Polycarbonate and optical plastics: Lightweight optical plastics remain a dominant material choice for many ADAS camera lenses due to impact resistance and cost advantages. The market for lens-grade polycarbonate is itself large and growing, creating both volume opportunity and price volatility. Procurement teams should plan hedging strategies and alternate supplier lists to mitigate price and availability shocks.

Glass vs. plastic trade-offs: Glass lenses deliver superior optical performance for high-resolution sensors but come with higher cost and manufacturing complexity. Hybrid approaches and improved plastics are narrowing these gaps; your chosen material strategy should align to expected sensor resolution, thermal requirements, and cost targets.

Policy and standards are accelerating baseline demand for blind-spot surveillance technologies. Notable drivers include:

Regional safety mandates that increasingly require advanced obstacle-detection and blind-spot information systems for new vehicles.

International standards governing pedestrian and vehicle detection performance for commercial vehicles, which raise the technical bar for sensor and lens validation.

These regulatory milestones convert latent safety interest into enforced specification sheets — shortening OEM negotiation cycles for required hardware and increasing urgency for compliant suppliers.

Prioritize supplier qualification for high-resolution lens production now: secure capacity windows and tech transfer timelines aligned with your next-generation camera module programs.

Hedge raw-material exposure by qualifying dual-sourced polycarbonate and specialized coatings to protect against price and supply swings.

Accelerate systems-level partnerships between optics specialists and Tier-1 ADAS integrators to offer verified module-level solutions rather than lens-only components.

Use regulatory compliance deadlines to justify incremental investment in thermal and environmental testing labs, reducing downstream program delays.

Consider selective bolt-on acquisitions to acquire IP around wide-FOV optics, anti-glare coatings, or compact lens geometries if internal R&D timelines are prohibitive.

PW Consulting’s full report is designed to be a decision-ready toolkit: financial-grade demand models, supplier diligence workbooks, and negotiation playbooks that procurement, product, and corporate development teams can deploy immediately. For companies prioritizing next-generation ADAS content, the report reduces timing risk and improves CAPEX allocation accuracy for 2026 program cycles.

To preserve the actionable advantage of the research, this press release omits the granular regional, application-level, and lens-type numeric breakdowns included in the paid report. Organizations seeking the complete dataset, proprietary vendor share tables, and customizable forecast modules are invited to access the full report and accompanying analyst briefings on our website.

Corporate subscribers and prospective clients can request the full Car Blind Spot Surveillance Lens Market report and a tailored briefing to extract the specific implications for their business. PW Consulting analyst teams are available to run bespoke scenario modeling and procurement readiness assessments to support 2026 program decisions.

For detailed analysis of this topic, please visit the official page:Car Blind Spot Surveillance Lens Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com