Fan Convectors Market 2026: Strategic Directions and Decision Frameworks — PW Consulting Preview

As organizations prepare capital allocations and product roadmaps for 2026, the fan convectors market presents a distinct combination of steady expansion, technology-driven displacement, and concentrated competitive dynamics. PW Consulting’s forthcoming Fan Convectors Market report synthesizes five years of historical performance (2020–2025) with a forward-looking 2026–2032 forecast period to deliver the actionable intelligence senior executives need to prioritize investments, de-risk supply chains, and accelerate product-to-market decisions.

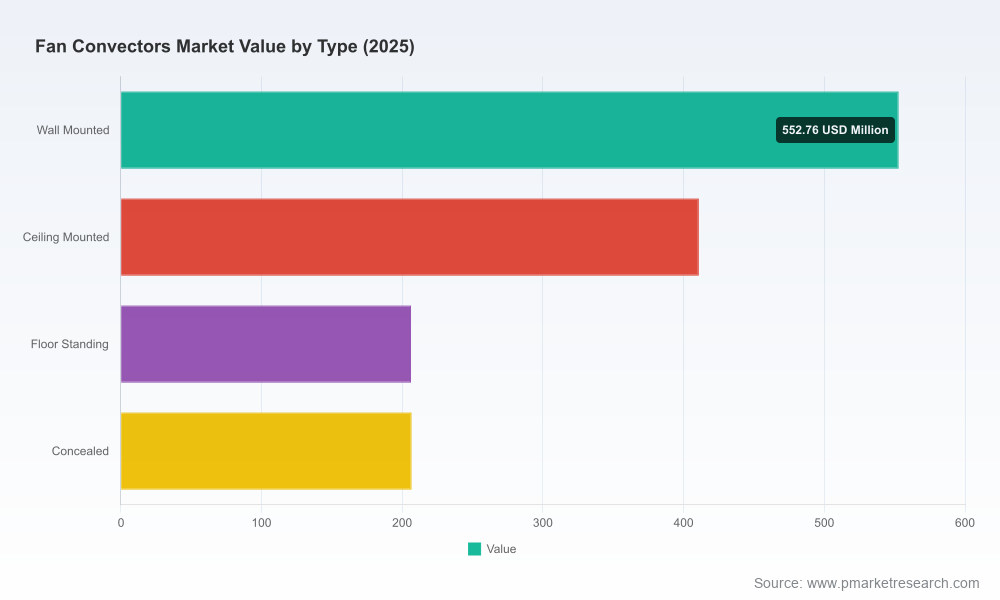

Fan Convectors Market

Macro view: growth, resilience, and what it means for 2026 planning

The global fan convectors market has demonstrated resilient growth through the recent cycle, climbing from just over USD 1.02 billion in 2020 to approximately USD 1.38 billion in 2025. PW Consulting’s base-case forecast anticipates a compound annual growth rate (CAGR) of 5.85% over the 2026–2032 horizon, with the total market reaching roughly USD 2.05 billion by 2032 under current assumptions.

Fan Convectors Market

- Implication for capital planning: a mid-single-digit CAGR signals predictable topline expansion but also intensifies the need for targeted differentiation — scale alone will not guarantee margin expansion.

- Implication for product strategy: stable growth combined with regulatory and end-use transitions (notably low-temperature heat sources) demands product portfolios that emphasize compatibility, efficiency, and low acoustic signatures.

- Implication for investors and M&A: market concentration metrics indicate meaningful room for consolidation — scale-enhancing deals that add complementary technology or channel access will remain compelling.

Market dynamics shaping 2026 decisions

Three structural trends define the near-term strategic landscape and will be key decision drivers for 2026:

Fan Convectors Market

- Low-temperature systems and heat-pump integration: Product design is converging around compatibility with low supply temperatures. Recent vendor announcements underscore an industry pivot to fan convectors that activate and perform reliably with system temperatures in the low-30s °C — a critical enabler for heat pump retrofits and new-build low-energy schemes.

- Space-constrained and retrofit-friendly architectures: Slimline and tile-integrated units (sub-100mm profiles in some offerings) are winning specification slots in residential and commercial refurbishments where floor/ceiling real estate is constrained.

- Efficiency, acoustics, and serviceability: Customers increasingly treat fan convectors not as commodity heat sources but as integrated system components where fan noise, partial-load efficiency, and maintainability materially affect lifecycle cost and occupant satisfaction.

Competitive landscape — positioning, capabilities, and strategic choices

The Fan Convectors Market exhibits moderate concentration — the top-three and top-five players control a material share of demand — creating both pressure and opportunity for mid-tier players. Our competitive assessment focuses on capability clusters rather than a transactional leaderboard, highlighting how incumbents and challengers are constructing durable advantages.

- Product-led incumbents focusing on low-temp performance: Several established manufacturers have accelerated development of fan convectors that are optimized for low-temperature water and quiet operation. These product updates reflect a strategic bet: capture the early retrofit and heat-pump-adoption wave by ensuring functional compatibility and contractor-friendly installation profiles.

- Slimline and integrated solutions specialists: Players offering ultra-compact units designed for ceiling tiles or shallow wall cavities are capitalizing on retrofit demand in dense urban buildings and constrained commercial fit-outs. Their technical differentiation allows premium positioning on the basis of space savings and aesthetics.

- Operationally focused commercial suppliers: Firms emphasizing commercial HVAC reliability and serviceability — including low-noise architectures and modular service access — are winning long-term facilities contracts, reinforcing recurring revenue through maintenance programs.

Company-level implications (select players)

Below we synthesize strategic takeaways from prominent participants; the intention is to clarify competitive choices rather than enumerate performance metrics.

- Smith’s Environmental Products (USA): Strong in PSU series and commercial ranges, Smith’s emphasis on quiet operation and low-temperature performance positions it well where occupant comfort and healthcare/school specifications dominate. Strategy: double down on institutional channels and ISO-classification case studies to widen specification wins.

- Myson (UK): Recent product updates explicitly tune activation and operation to lower system temperatures, closing a critical technical gap for heat pump integrations. Strategy: leverage early mover credibility into specification libraries for retrofit installers and collaborate with heat pump OEMs for co-marketing and warranty bundling.

- SPC HVAC (UK): Strength in ceiling-tile form factors and slim installations aligns with retrofit-led growth in dense commercial markets. Strategy: target partnering with fit-out contractors and MEP consultancies to secure design-stage specification inclusion.

- Jaga (Belgium): Technical leadership in slim Briza products and balanced heating/cooling performance supports premium positioning, particularly in projects pursuing low-temperature operation and occupant comfort. Strategy: monetize intellectual-property through licensing of slim-profile architectures in adjacent geographies.

- Dunham-Bush (UK/USA) & Frico (Sweden): Both emphasize robustness and rapid response models for commercial deployments — opportunities exist to upsell long-term service contracts and to integrate digital controls for performance monitoring. Strategy: develop SaaS-enabled after-sales offerings to turn installed bases into recurring revenue streams.

What PW Consulting’s report delivers to executives

Our full report is structured to support three decision-making horizons — immediate 12–18 month actions, medium-term capability builds (18–36 months), and long-term portfolio/footprint choices (36+ months). Key practical deliverables include:

- Decision frameworks for product development: clear go/no-go criteria for low-temperature compatibility, acoustic targets, and modularity thresholds that align with average payback periods for retrofit customers.

- Procurement and supplier playbooks: negotiation levers, preferred contract clauses, and inventory strategies to mitigate component shortages and lead-time risk across Tier-1 and Tier-2 suppliers.

- Commercial channel and specification maps: guidance on which distributor and contracting channels to prioritize by building type and retrofit intensity (note: the report contains granular segment maps and supplier shares behind a gated section).

- Regulatory and standards tracker: near-term compliance checkpoints relevant to Europe and North America, and the consequential product feature set required to stay compliant in 2026 tenders.

- Financial and M&A scorecards: valuation sensitivities for tuck-in versus scale acquisitions, including synergies arising from product families and service platform integrations.

Risk assessment and scenario planning

We present three core scenarios in the report — Baseline (policy and adoption trends continue), Accelerated Heat Pump Adoption (faster low-temperature system penetration), and Supply-Constrained (component lead-time shocks). For 2026 planning, the key operational levers differ:

- Under the Accelerated scenario, prioritize product compatibility, local assembly for fast-turn retrofit kits, and joint go-to-market programs with heat pump OEMs.

- Under Supply-Constrained conditions, lock strategic long-lead components under multi-year agreements and diversify manufacturing footprints to reduce single-point geographic risk.

- Under Baseline conditions, focus on margin-accretive product upgrades and targeted geographic expansion into high-specification institutional channels.

How to use this preview — next steps for 2026 decision-makers

This preview outlines why the 2026 planning cycle is a pivot point: the market’s predictable growth trajectory (mid-single-digit CAGR) plus accelerating low-temperature system adoption reshapes product requirements and supplier economics. For product teams, prioritize low-temperature activation and slimline architectures; for commercial leaders, secure specification pathways with retrofit installers and facility managers; for finance and corporate development, screen targets that add either technical capability or channel control.

For procurement and operations executives, immediate actions include stress-testing supplier continuity, defining locked-in pricing windows for critical components, and initiating pilot assemblies to validate low-temperature performance on representative job sites.

Accessing the full intelligence

PW Consulting’s full Fan Convectors Market report contains the detailed segmentation, regional and application breakdowns, proprietary demand model spreadsheets, and an exhaustive competitive appendix required to operationalize the strategies summarized here. This preview is designed to establish our analytical framework and to highlight the strategic choices facing executives in 2026 — the in-depth segment-level data and vendor share matrices are available in the full report on the PW Consulting portal.

To arrange a briefing or to license the full report and attached financial models, contact the PW Consulting Industry Research team. Our analysts can also run a tailored workshop to map your product roadmaps and procurement plans directly to the market scenarios we model.

For detailed analysis of this topic, please visit the official page:Fan Convectors Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com